Umbrella Coverage for Families: Protecting Your Loved Ones

Your home and car insurance have limits. When someone sues your family for more than those limits cover, your personal assets are at risk.

Umbrella coverage for families fills that gap, protecting your savings, home equity, and future earnings from major liability claims. We at H&K Insurance Agency help families understand how this extra layer of protection works and why it matters.

How Umbrella Insurance Actually Works

Umbrella insurance is straightforward: it’s additional liability coverage that starts paying after your home or auto policy limits are exhausted. Most policies begin at 1 million dollars in coverage, though you can purchase higher amounts depending on your situation. The key thing to understand is that umbrella insurance doesn’t replace your existing policies-it sits on top of them.

The Layering Structure That Protects Your Assets

If someone sues your family for injuries or property damage, your auto or homeowners policy pays first up to its limit, then the umbrella policy kicks in for amounts beyond that threshold. For example, if a guest is severely injured at your home and medical costs reach 650,000 dollars while your homeowners liability limit is only 500,000 dollars, the umbrella covers that remaining 150,000 dollar gap. This layering structure makes umbrella insurance remarkably affordable. According to ACE Private Risk Services data cited by Forbes, the average annual cost for a 1 million dollar umbrella policy for a typical family profile (one home, two cars, two drivers) is about 383 dollars per year. Additional coverage beyond that first million typically costs around 75 dollars per year for each additional million dollars of protection.

Why the Cost Makes Sense

That pricing makes sense when you consider what’s at stake: a serious accident or lawsuit could cost hundreds of thousands of dollars out of pocket without this protection. The real value emerges in specific scenarios where standard policies fall short. A multi-car accident with 700,000 dollars in bodily injury claims exceeds what most auto policies cover-typically capped at 300,000 to 500,000 dollars depending on your limits. The umbrella covers that excess without leaving your family financially exposed.

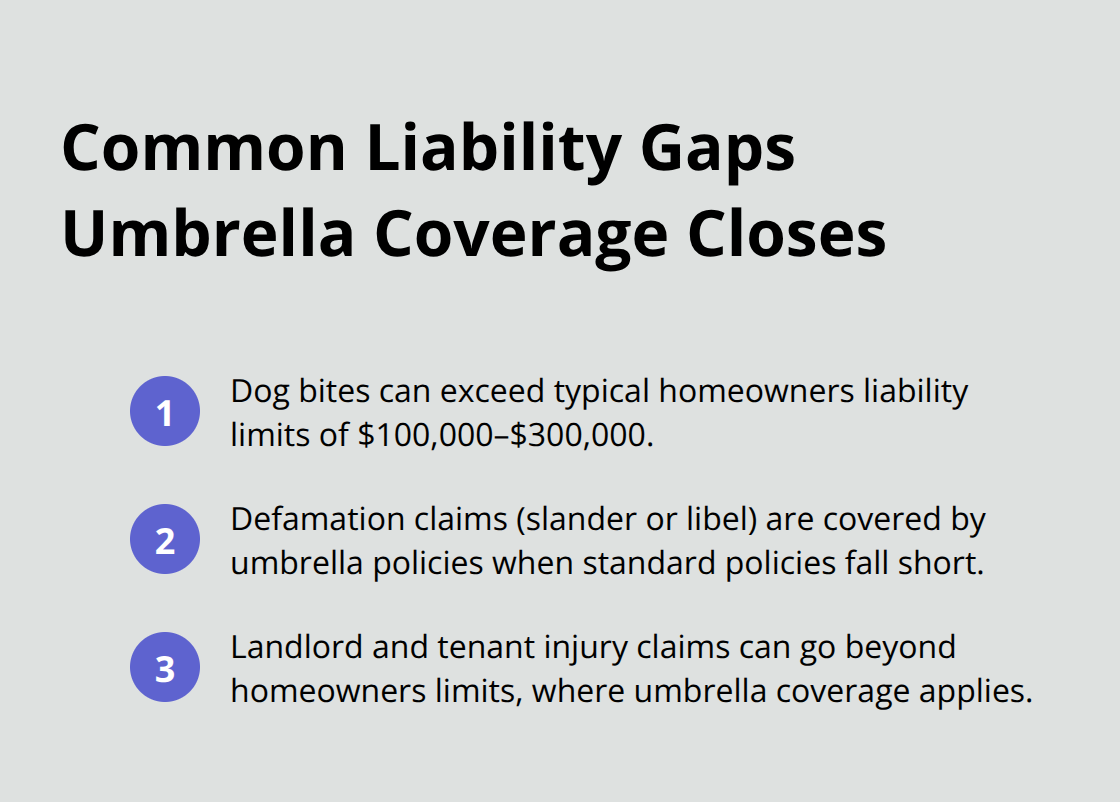

Common Liability Gaps Umbrella Coverage Closes

Dog bite liability presents another common situation where umbrella insurance matters; homeowners policies often include only 100,000 to 300,000 dollars in personal liability coverage, and a serious bite claim can easily surpass that amount. Defamation claims (slander or libel) also fall under umbrella protection and can involve substantial damages that your standard policies won’t cover. Property owners benefit significantly too: if you rent out a unit and a tenant is injured on the property, umbrella coverage protects against liability claims beyond your homeowners policy limits.

These aren’t hypothetical risks-they’re real exposures that families face, and the 383 dollar annual investment provides genuine peace of mind.

Understanding how umbrella insurance fills these gaps is essential, but the next step involves assessing your own situation to determine the right coverage amount for your family’s specific assets and lifestyle.

Why Your Family’s Liability Exposure Is Bigger Than You Think

Social Media and Modern Accidents Amplify Your Risk

Liability risks have fundamentally shifted over the past decade, and most families dramatically underestimate their exposure. Social media amplifies personal injury claims-a slip-and-fall at your home can result in medical costs that balloon into the hundreds of thousands when documented online and shared widely. Teen drivers present another substantial risk; according to the CDC, motor vehicle crashes are the leading cause of death for U.S. teens, and a serious accident involving your teenager could generate liability claims well beyond standard auto policy limits. Dog ownership creates measurable risk too: the CDC reports that roughly 4.5 million dog bites occur annually in the United States, and a single severe bite case can easily cost 500,000 dollars or more in medical expenses and damages.

Property Owners Face Steeper Exposure

These aren’t remote possibilities-they’re statistically probable events that families with assets must address directly. Property owners face even steeper exposure; if you rent out a unit or even allow extended family to live on your property, tenant injuries or visitor accidents create liability scenarios that standard homeowners policies simply cannot absorb. The financial reality is stark: a 650,000 dollar judgment against your family with only 300,000 dollars in underlying coverage leaves a 350,000 dollar gap that comes directly from your savings, home equity, and future earnings. That gap exists because most people never reassess their liability limits as their net worth grows and their family circumstances change.

Legal Defense Costs Add Up Faster Than You Expect

The cost of legal defense alone justifies umbrella coverage for any family with meaningful assets. When someone sues your family, your insurance carrier covers legal fees up to policy limits, but those costs mount rapidly-expert witnesses, depositions, and trial preparation can easily exceed 50,000 dollars before a settlement is reached. Umbrella policies cover these defense costs in addition to damages, meaning your family’s financial exposure includes both the judgment amount and the cost to defend against it.

The Math Behind Umbrella Protection

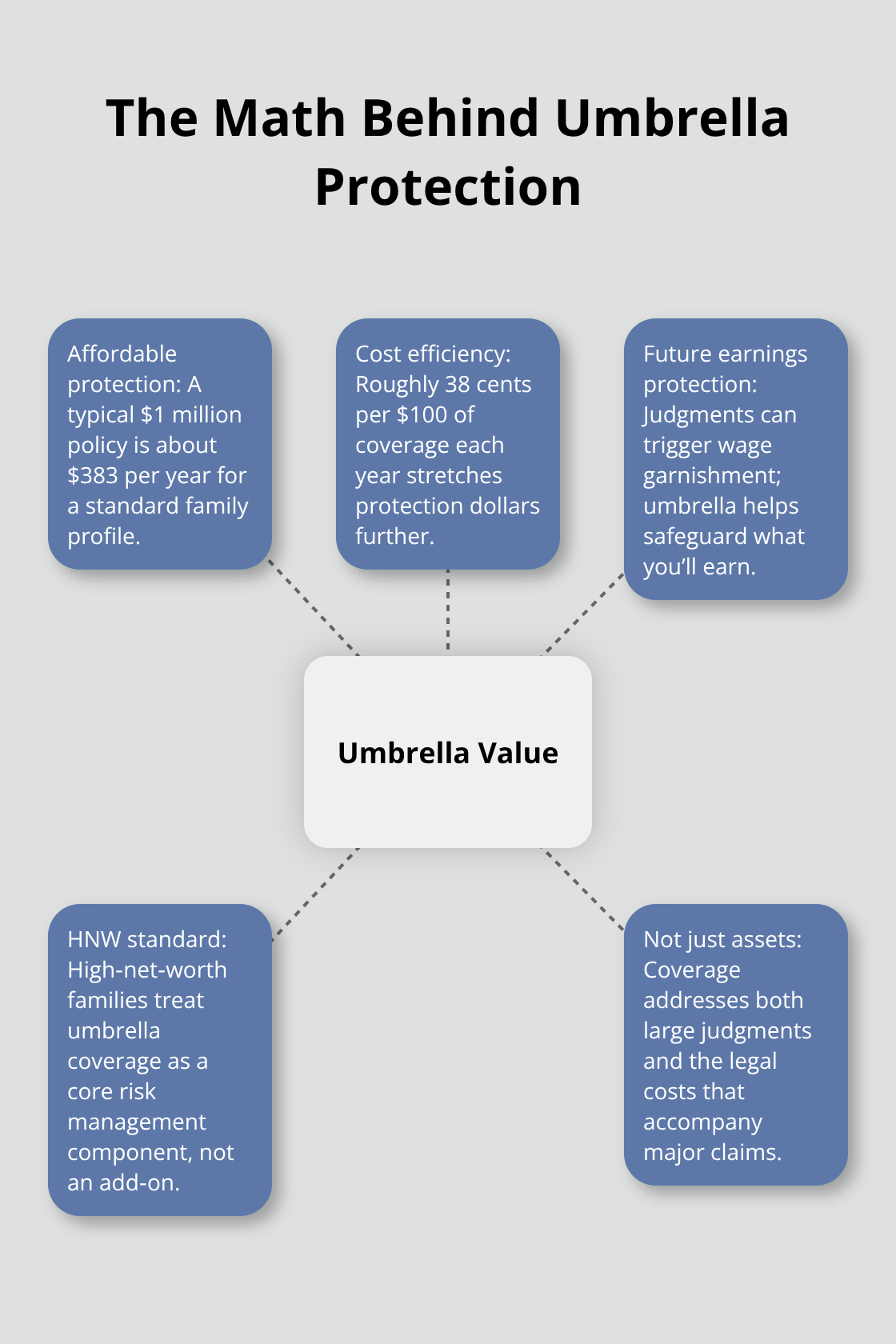

For families with a combined net worth above 500,000 dollars, umbrella insurance becomes mathematically essential rather than optional. The typical 1 million dollar policy costs around 383 dollars annually for a standard family profile, which translates to protecting 1 million dollars of assets for roughly 38 cents per hundred dollars of coverage per year. That efficiency explains why high-net-worth families treat umbrella insurance as a standard component of their risk management strategy rather than an optional add-on.

Your future earning potential also sits at risk in liability lawsuits; a judgment can lead to wage garnishment or asset seizure that impacts your financial security for decades. Umbrella coverage protects not just what you’ve already built but what you’ll earn going forward, making it particularly valuable for families in their peak earning years.

Once you understand how real these liability exposures are, the next logical step involves calculating exactly how much umbrella coverage your family actually needs.

How Much Umbrella Coverage Does Your Family Actually Need

Calculate Your Current Protection Gaps

Pull your auto and homeowners policy declarations pages right now. Most families have no idea what their actual liability limits are, which makes choosing umbrella coverage impossible. Your homeowners policy likely caps personal liability at 300,000 dollars, and your auto policy probably maxes out at 300,000 to 500,000 dollars depending on whether you selected basic or higher limits. These numbers feel substantial until you face a real claim. A single serious accident with multiple injured parties can generate damages exceeding 1 million dollars in medical costs alone, and that’s before accounting for pain and suffering damages, which often dwarf medical expenses in liability cases.

Start with a baseline calculation: add your home equity, investment accounts, retirement savings, and any rental property value. If that total exceeds 500,000 dollars, your underlying liability limits are already inadequate. The gap between your current limits and your total assets represents your unprotected exposure.

Understand Minimum Requirements and True Costs

A 1 million dollar umbrella policy costs approximately 383 dollars annually for a standard family according to ACE Private Risk Services data, but that price assumes you already meet minimum underlying coverage requirements. Most insurers require at least 300,000 dollars in homeowners liability and either 300,000/300,000 or 250,000/500,000 in auto bodily injury and property damage limits before they’ll write an umbrella policy. If your current limits fall below those thresholds, you’ll need to increase them first, which actually costs more than simply purchasing umbrella coverage from the start.

That pricing makes sense when you consider what’s at stake. A 650,000 dollar judgment against your family with only 300,000 dollars in underlying coverage leaves a 350,000 dollar gap that comes directly from your savings and home equity.

Match Coverage to Your Risk Profile

The right coverage amount depends on your specific risk profile, not generic rules. High-net-worth families, landlords, and families with teenage drivers should seriously consider 2 to 3 million dollars in umbrella protection rather than stopping at 1 million. Each additional million typically costs around 75 dollars per year, making the jump from 1 million to 2 million quite affordable when you consider what’s at stake.

Your future earning potential also sits at risk in liability lawsuits; a judgment can lead to wage garnishment that impacts your financial security for decades. Umbrella coverage protects not just what you’ve already built but what you’ll earn going forward.

Optimize Your Policy Details and Discounts

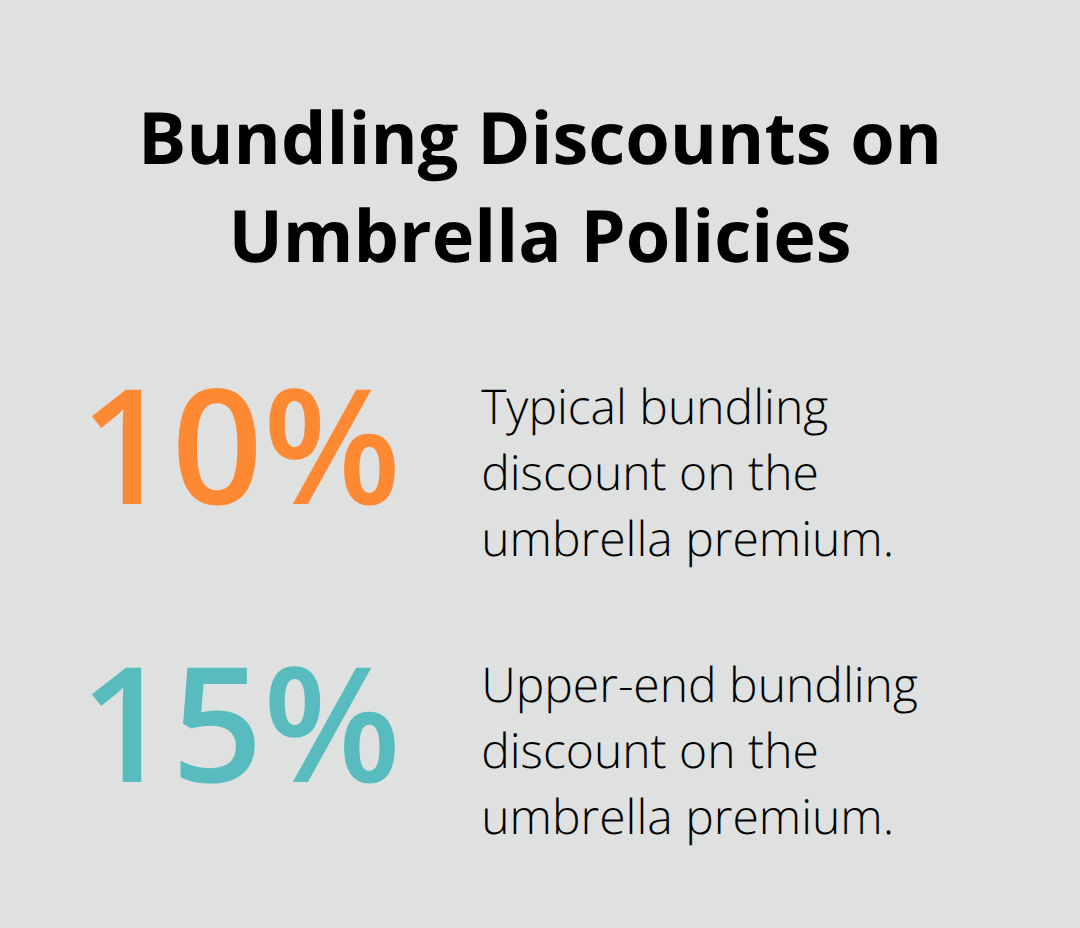

Bundling your umbrella policy with your auto and home coverage typically unlocks discounts of 10 to 15 percent on the umbrella premium itself, plus additional savings on your underlying policies. If you own rental property (even a single unit), you need umbrella coverage that explicitly includes landlord liability; standard personal umbrella policies sometimes exclude or limit coverage for rental operations.

If you have a dog, verify that your breed isn’t excluded from the policy before purchasing, as some insurers restrict coverage for certain breeds or deny claims entirely based on breed history.

The most practical approach involves scheduling a consultation where an agent reviews your specific assets, liability exposures, and family circumstances to recommend an actual number rather than guessing based on generic advice. H&K Insurance Agency represents multiple carriers across the Puget Sound region and can compare umbrella quotes from different insurers because pricing varies significantly based on your location, number of properties, driving records, and claims history.

Final Thoughts

Umbrella coverage for families isn’t a luxury-it’s a practical financial safeguard that costs less than most people spend on coffee annually. A 1 million dollar policy runs approximately 383 dollars per year for a typical family, yet it protects hundreds of thousands of dollars in assets and future earnings from a single liability claim. Without this protection, a serious accident or lawsuit forces you to liquidate savings, tap home equity, or face wage garnishment for years.

Your homeowners and auto policies have limits, and those limits fall almost certainly lower than your total assets. When a claim exceeds those limits, your family bears the financial burden directly. Umbrella insurance eliminates that gap by stepping in after your underlying policies max out, covering both damages and legal defense costs (which can reach 50,000 dollars or more before settlement).

Pull your policy declarations pages and calculate your actual liability limits versus your total assets. If that gap exists-and for most families it does-contact H&K Insurance Agency to compare umbrella quotes and find the coverage that fits your family’s specific situation and budget.