Kitsap rental property coverage: Landlord’s Guide to Protection

Owning rental property in Kitsap County comes with real financial exposure that standard homeowners policies simply don’t address. Most landlords discover this gap only after a tenant injury or property damage claim lands on their desk.

At H&K Insurance Agency, we’ve helped dozens of local property owners understand why Kitsap rental property coverage requires a completely different approach than personal home insurance. The right landlord policy protects your building, your liability, and your income-all three matter equally.

Why Your Homeowners Policy Won’t Protect Your Rental

Standard Homeowners Policies Exclude Rental Properties

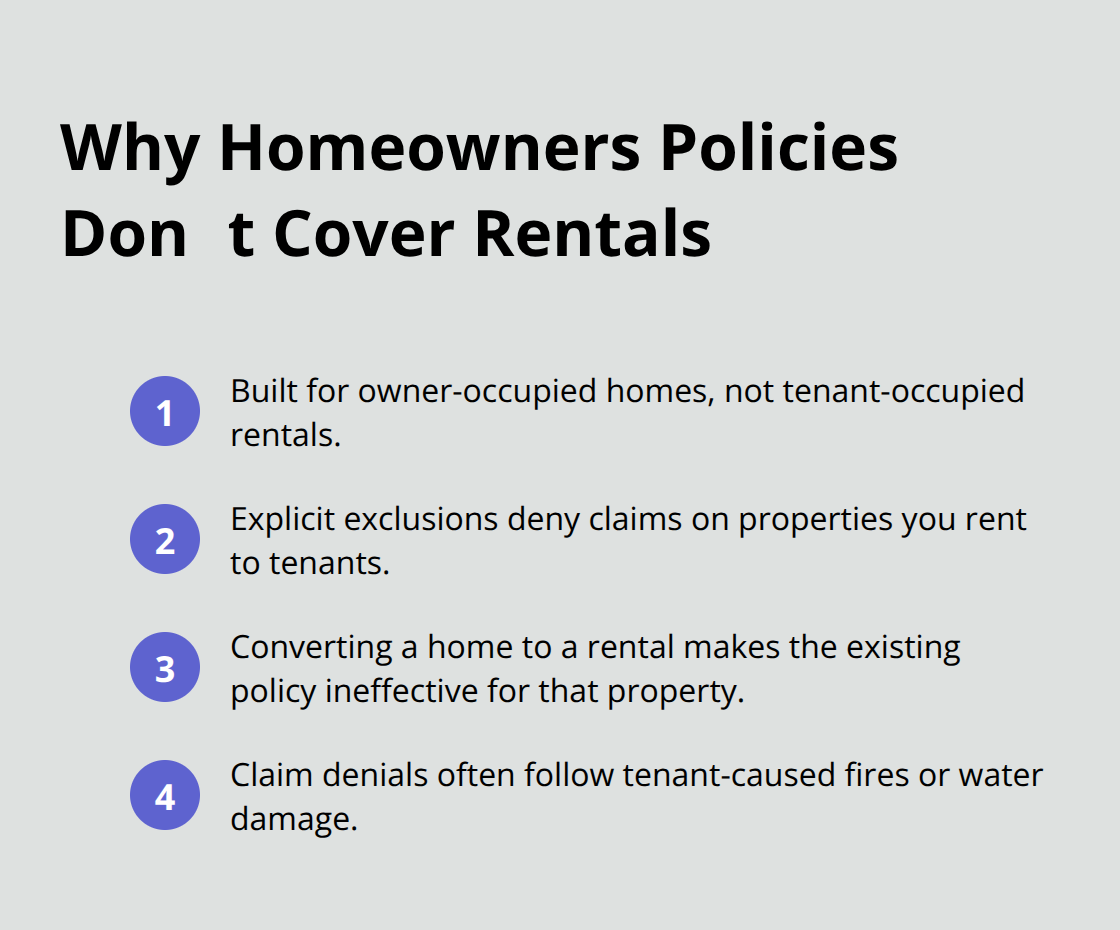

Your homeowners insurance policy explicitly excludes rental properties. This isn’t a loophole or an oversight-it’s intentional. Standard homeowners policies are designed for owner-occupied residences, and insurers won’t pay claims on properties you rent to tenants.

The moment you convert your home to a rental, your existing coverage becomes worthless for that property. Many Kitsap landlords learn this harsh truth only when they file a claim after a tenant-caused fire or water damage and watch their insurer deny it outright.

Washington State Insurance Resources confirms that landlords’ insurance covers the building and landlord liability, while standard homeowners policies simply don’t. Your policy language will state this exclusion clearly-but most landlords never read it until they need it.

Personal Liability Exposure You Can’t Ignore

Beyond the building itself, you face exposure that homeowners policies never address. If a tenant or visitor is injured on your property and sues you, your homeowners liability won’t cover it. If a tenant’s guest slips on a wet step and fractures their spine, you’re personally liable for their medical bills and any judgment against you.

Washington’s comparative negligence laws make this risk even sharper-courts assign fault based on percentage of responsibility, meaning you could be found partially liable even when you’re not the direct cause. Landlord policies in Washington should start with at least $500,000 in liability coverage per occurrence. Your personal assets sit unprotected when you carry inadequate coverage for years without realizing the gap between what you think you’re covered for and what you actually are.

Loss of Rental Income: The Hidden Financial Drain

Landlord insurance addresses what homeowners policies completely ignore: loss of rental income. If a covered event like fire or severe wind damage makes your property uninhabitable, your mortgage and property taxes don’t pause. In Seattle, a six-month vacancy during reconstruction erases more than $13,000 in gross rent. That’s money you’ll owe whether the unit generates income or not.

Proper landlord coverage includes loss of rents protection for 12 to 24 months, covering your lost revenue while repairs happen. Without this, you absorb the full financial hit yourself.

Building Coverage That Reflects Today’s Costs

The second critical gap is building coverage structured for rental properties. Homeowners policies use actual cash value, which depreciates everything. A 15-year-old roof damaged in a windstorm gets paid out at its depreciated value, not what it actually costs to replace. Landlord policies should use replacement cost value instead, paying you what it truly costs to rebuild or repair in today’s market.

Washington construction costs rose about 15 percent from 2020 to 2023, with Seattle-area rebuilding costs running $350 to $500 per square foot. Your policy needs to reflect these current prices, not yesterday’s values.

Building Ordinance Coverage Protects Against Code Upgrades

Additionally, landlord policies include building ordinance coverage, which homeowners policies exclude entirely. When you rebuild after a covered loss, Kitsap County building codes may require upgrades-updated electrical systems, improved egress windows, or seismic reinforcement. These code-upgrade costs typically represent 10 to 25 percent of the dwelling limit. Without ordinance coverage, you pay those upgrades out of pocket while your insurance pays only the pre-loss building cost.

The gaps in standard homeowners coverage create real financial exposure that landlord-specific policies address directly. Understanding these differences shapes how you protect your rental income and assets. The next step involves selecting the right coverage types and limits for your specific Kitsap property.

What Coverage You Actually Need for a Kitsap Rental

Building Coverage That Matches Today’s Reconstruction Costs

Replacement cost value for your building is non-negotiable. When you rebuild after fire or wind damage, you need dollars that match 2026 construction prices, not depreciated values. In the Seattle area, rebuilding costs run $350 to $500 per square foot, so a 1,500-square-foot rental damaged by fire could cost $525,000 to $750,000 to reconstruct. If your policy pays only actual cash value, you’ll absorb tens of thousands in out-of-pocket repair costs.

Liability Protection Against Tenant and Visitor Injuries

Liability coverage should start at $500,000 per occurrence minimum, and many Kitsap landlords should carry $1 million or more if they own multiple properties. A single lawsuit from a tenant’s guest injured on your property can exceed $300,000 in medical bills and damages. Washington’s comparative negligence system means courts assign partial fault even when you’re not the primary cause, making robust liability limits essential.

Loss of Rents and Building Ordinance Coverage

Loss of rents coverage protects your mortgage and property taxes when a covered loss makes the unit uninhabitable. A six-month vacancy during reconstruction in the Kitsap area costs roughly $6,000 to $12,000 in lost rent, depending on your unit’s market rate. You should carry loss of rents protection for 12 to 24 months of your expected monthly income.

Building ordinance coverage deserves special attention because it’s often overlooked. When Kitsap County codes require seismic upgrades, electrical system replacements, or egress window improvements after a loss, ordinance coverage pays 10 to 25 percent of your dwelling limit toward those mandated upgrades. Without it, you pay code-compliance costs separately.

Water, Flood, and Earthquake Endorsements for Puget Sound Risks

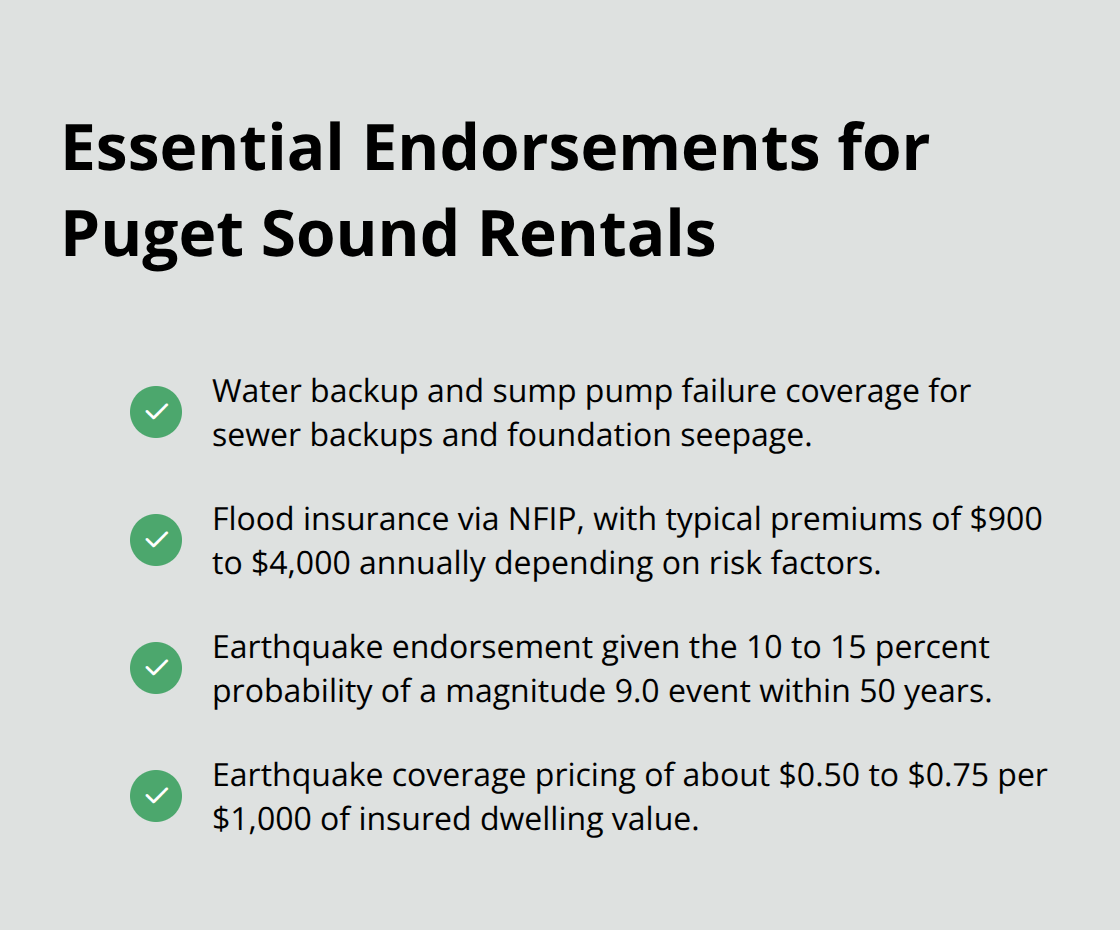

Water backup and sump pump failure endorsements are vital for Kitsap properties because standard policies exclude sewer backups and foundation seepage. A single sewer backup can cost $15,000 to $30,000 in cleanup and property damage. Flood coverage is separate from standard landlord policies entirely and requires enrollment in the National Flood Insurance Program if your property sits in a mapped floodplain. NFIP premiums typically run $900 to $4,000 annually depending on elevation and foundation type.

Earthquake endorsements also matter in the Puget Sound region given the 10 to 15 percent probability of a magnitude 9.0 Cascadia Subduction Zone event within the next 50 years. Earthquake coverage costs roughly $0.50 to $0.75 per $1,000 of insured dwelling value, making it an affordable addition.

Comparing Quotes and Maximizing Savings

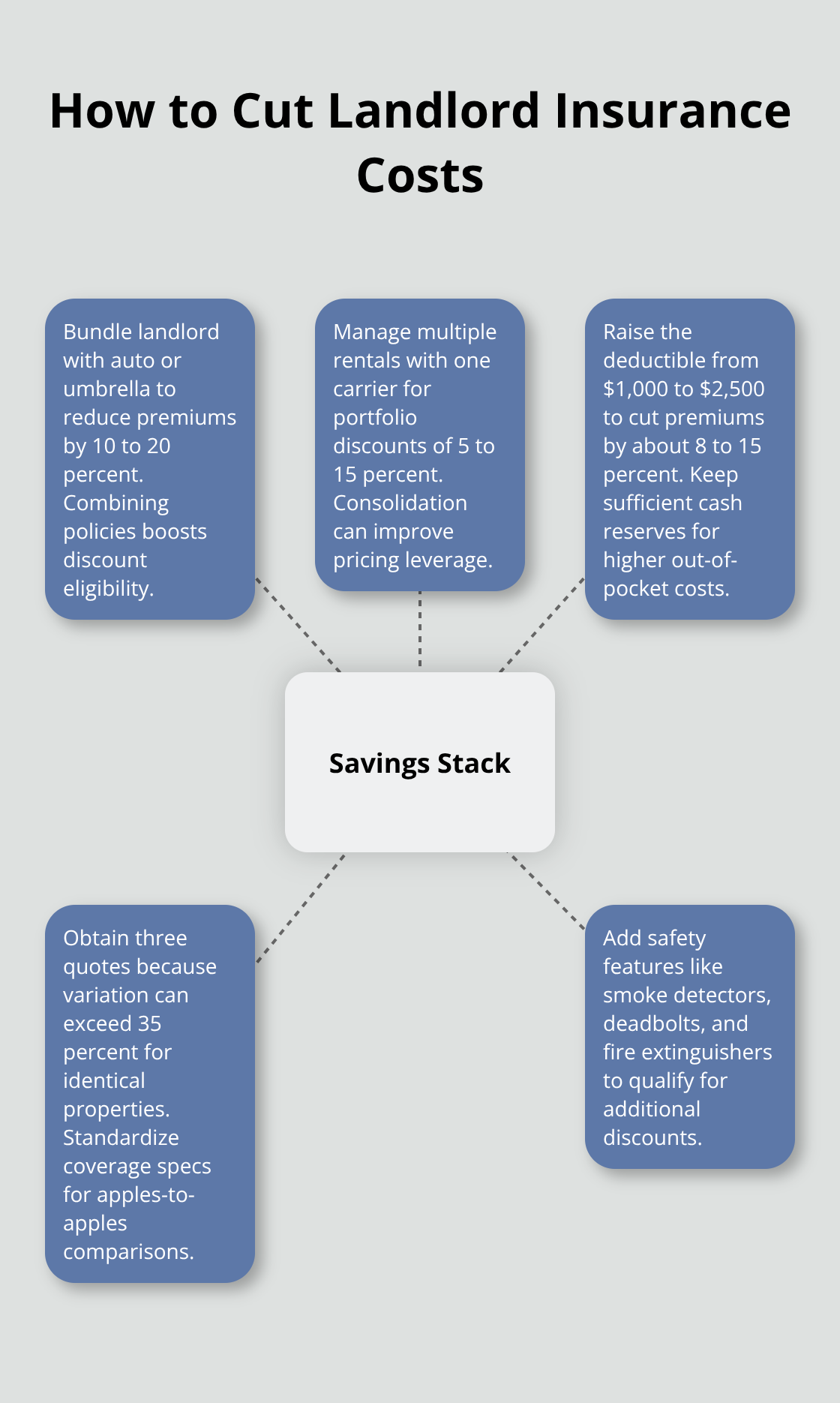

When comparing quotes from carriers, verify that each quote includes replacement cost value, not actual cash value, and confirm liability limits start at $500,000. Premium variation across carriers can exceed 35 percent for identical properties, so obtaining three quotes from different insurers is essential.

Bundling landlord coverage with your auto or umbrella policy reduces premiums by 10 to 20 percent, and managing multiple rental properties through one carrier unlocks portfolio discounts of 5 to 15 percent. Raising your deductible from $1,000 to $2,500 cuts premiums by roughly 8 to 15 percent, but only if you maintain sufficient cash reserves to cover the higher out-of-pocket expense when a claim occurs.

The right coverage combination protects your building, income, and personal assets-but only if you select limits and endorsements that match your property’s actual risks. An independent agent who represents multiple carriers can help you navigate these options and find the right balance between protection and cost.

How to Save Money While Protecting Your Kitsap Rental

Compare Quotes Across Multiple Carriers

Premium variation for identical properties exceeds 35 percent, so obtaining three separate quotes with matching property details reveals how much carriers actually differ in their risk assessment and pricing. When you compare, verify each quote includes replacement cost value rather than actual cash value, confirm liability limits start at $500,000 per occurrence, and ensure loss of rents coverage extends 12 months minimum. Many Kitsap landlords accept the first quote and leave thousands of dollars on the table annually. An independent agent representing multiple carriers can access rate differences you won’t find shopping alone and will identify which carriers offer the best claims performance and customer service in the Puget Sound region specifically.

Stack Discounts for Immediate Savings

Bundling your landlord policy with auto or umbrella coverage cuts premiums by 10 to 20 percent, and managing multiple rental properties through a single carrier unlocks portfolio discounts of 5 to 15 percent immediately. Raising your deductible from $1,000 to $2,500 reduces premiums by roughly 8 to 15 percent, but only if you maintain cash reserves large enough to absorb that higher out-of-pocket cost when a claim occurs. Many carriers offer discounts for safety features like working smoke detectors, deadbolt locks, and fire extinguishers because these reduce loss frequency. The real savings opportunity lies in stacking these discounts together rather than selecting one approach alone.

Reduce Claims Through Active Risk Management

Carriers reward landlords who reduce claims through maintenance and tenant screening. Regular property inspections and preventive maintenance lower water damage and liability claims, which insurers recognize with reduced rates. Thorough tenant screening through credit checks, criminal history, employment verification, and landlord references significantly reduces tenant-caused damage claims. Documenting property condition at move-in and move-out protects you from false damage claims and prevents disputes that lead to liability exposure. Keeping your property occupied minimizes vandalism and burglary losses during vacancies, which directly affects your premium. Some insurers offer discounts for completing landlord training courses or maintaining a detailed maintenance log because these actions prove you manage risk actively.

Match Your Property to the Right Carrier

The carriers offering the best rates aren’t always the cheapest initially but rather those whose underwriting rewards your specific risk profile. An agent with deep knowledge of Kitsap properties understands which carriers value your property type, tenant situation, and maintenance practices most favorably, allowing them to match you with the insurer most likely to offer competitive rates today and tomorrow. Independent agencies representing multiple carriers serving the Puget Sound region can tailor options to your specific situation and leverage regional expertise on local claims performance.

Final Thoughts

Protecting your Kitsap rental property requires three distinct layers of coverage that standard homeowners policies simply don’t provide. Building protection with replacement cost value allows you to rebuild at today’s construction prices without absorbing tens of thousands in out-of-pocket costs. Liability coverage starting at $500,000 shields your personal assets when a tenant or visitor suffers injury on your property, and loss of rents protection covers your mortgage and taxes during reconstruction.

The real opportunity lies in comparing quotes across multiple carriers and stacking discounts strategically. Premium variation exceeds 35 percent for identical properties, meaning your first quote could cost thousands more annually than your best option. Bundling with auto coverage, managing multiple properties through one carrier, and raising your deductible all reduce premiums significantly when combined, while active risk management through tenant screening and preventive maintenance proves to insurers that you reduce claims.

Your next step is straightforward: gather your property details and obtain three quotes from different carriers with identical coverage specifications. Verify each quote includes replacement cost value, $500,000 liability minimum, and 12 months loss of rents coverage. Contact H&K Insurance Agency to discuss your Kitsap rental property coverage needs and receive quotes that reflect competitive pricing and local expertise in the Puget Sound region.