Landlord Tenant Disruption Coverage: Planning For Renters, Repairs, And Relocations

A single repair can turn your rental income into a financial headache. When tenants need to relocate due to fire, water damage, or other covered events, you’re left covering temporary housing costs while your property sits vacant.

Landlord tenant disruption coverage protects you from these income gaps. At H&K Insurance Agency, we help Puget Sound landlords understand how this coverage works and why it matters for their bottom line.

What Landlord Tenant Disruption Coverage Actually Pays For

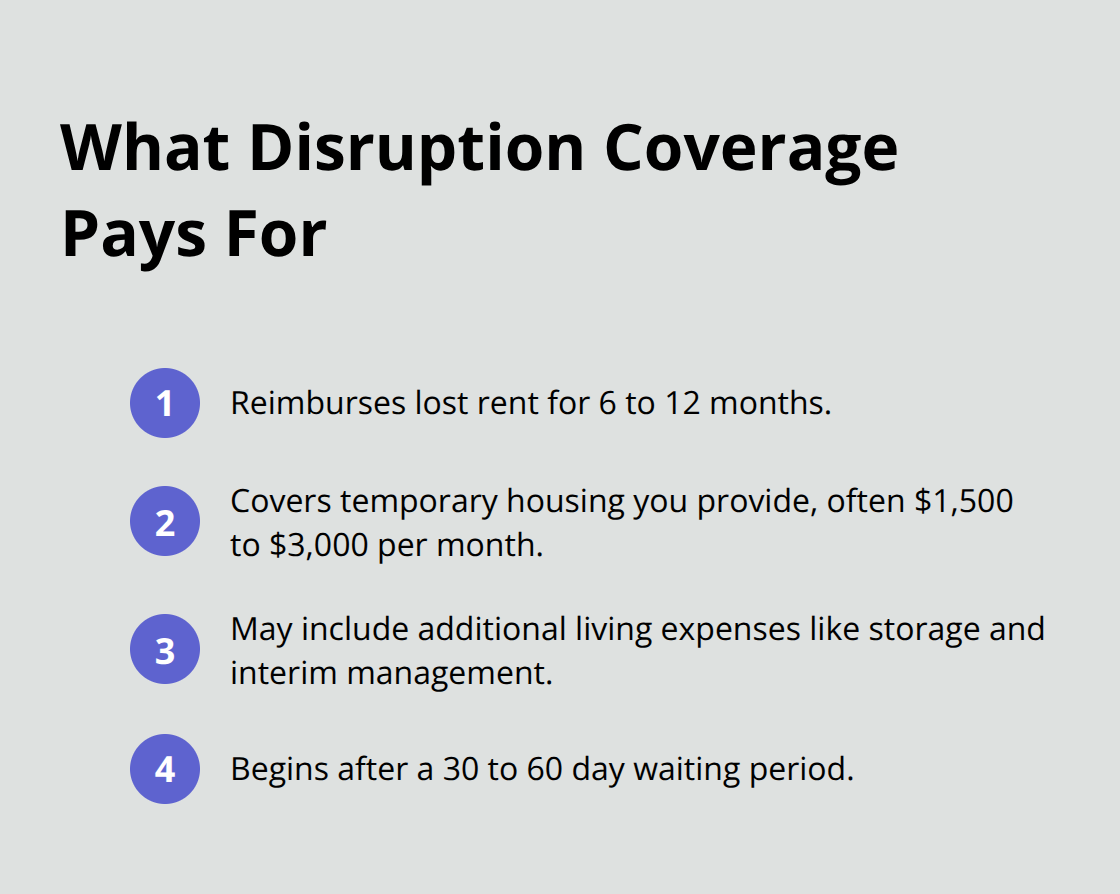

Landlord tenant disruption coverage fills a specific gap that standard landlord policies ignore: the financial damage that occurs when tenants cannot occupy your property. When a fire, water damage, or other covered event forces tenants out, your rental income stops immediately, but your expenses continue. You still owe the mortgage, property taxes, utilities, and maintenance costs. Disruption coverage reimburses the rent you would have collected during the repair period, typically covering 6 to 12 months of lost income depending on your policy. Some carriers also cover the temporary housing costs you provide to displaced tenants, which can range from $1,500 to $3,000 per month in the Puget Sound region depending on unit size and local market rates. Additional living expenses tied to covered events-such as storage fees for tenant belongings or interim property management costs-may also fall under your policy, though this varies significantly between carriers.

The waiting period before payouts begin typically runs 30 to 60 days, which means you absorb the initial financial hit before coverage kicks in.

How Fire Damage Creates Income Loss

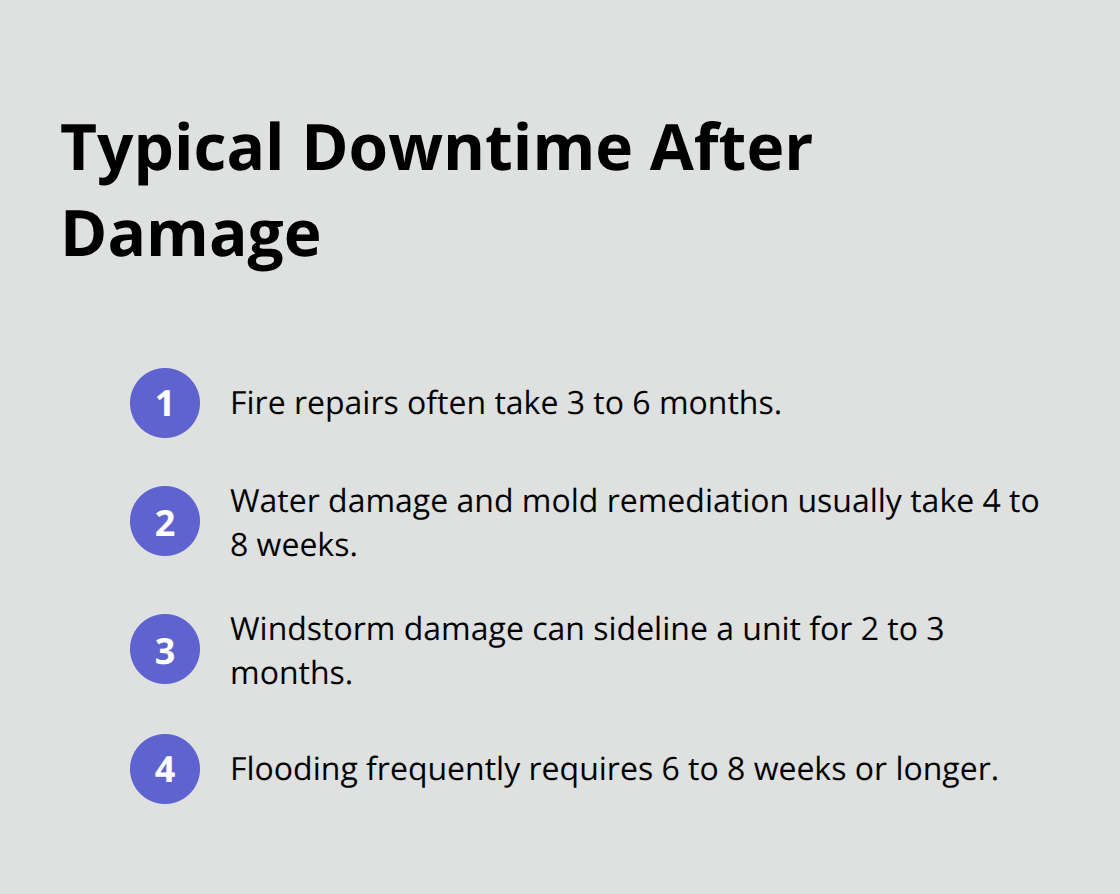

Fire damage represents one of the costliest disruption scenarios. A residential fire can take 3 to 6 months to fully remediate, including structural repairs, system restoration, and code compliance inspections. During that entire window, your tenant lives elsewhere and you collect zero rent. If your property generates $2,000 monthly, that translates to $6,000 to $12,000 in lost income before repairs finish. Water damage and mold remediation often extend 4 to 8 weeks, creating similar income gaps. Natural disasters in the Puget Sound area-though less frequent than in other regions-can displace tenants for months. Without disruption coverage, you absorb all those lost months out of pocket.

What You Pay When Tenants Relocate

When you relocate tenants due to property damage, you typically cover their temporary housing costs. While relocation assistance requirements vary by jurisdiction and circumstance, they illustrate the real costs you face when tenants must move. Disruption coverage absorbs these temporary housing expenses, preventing them from compounding your lost rental income. Some policies also reimburse reasonable storage costs if tenants need to store belongings during repairs, which can add $200 to $400 monthly per unit in the Puget Sound area.

Coverage Limits and Waiting Periods Matter

The structure of your disruption policy directly affects how much financial protection you actually receive. Most policies impose a waiting period of 30 to 60 days before payouts begin, which means you cover the initial repair costs and lost rent yourself. Coverage limits typically cap at 6 to 12 months of rent, so properties with extended repair timelines may face gaps in protection. Some carriers exclude certain events-like damage from tenant negligence or lack of maintenance-so you need to understand exactly what your policy covers. The cost of this coverage varies based on your property’s location, age, and claims history, but most landlords find the premium reasonable compared to the financial exposure they face.

Understanding What Varies Between Carriers

Different insurance carriers structure disruption coverage in fundamentally different ways. One carrier might cover temporary housing at actual cost while another caps reimbursement at a fixed monthly amount. Some policies include loss of rent immediately after the waiting period ends, while others require proof that repairs are actively underway. Additional living expenses receive different treatment across the market-some carriers cover them generously, others exclude them entirely. When you compare policies, focus on the specific events covered, the length of the waiting period, the maximum monthly payout, and whether the policy covers both your lost rent and tenant relocation costs. This comparison process determines whether your coverage truly protects your income or leaves you exposed to significant losses.

The right disruption coverage transforms a potential financial crisis into a manageable situation. Understanding what different policies actually pay for positions you to make decisions that align with your property’s specific risks and your financial situation.

When Fire, Water, and Disasters Force Tenants Out

Fire Damage Stops Rent Collection Immediately

Fire damage ranks among the fastest ways to eliminate your rental income. A residential fire requires 3 to 6 months of repair work, including structural reconstruction, electrical and plumbing system restoration, and final code compliance inspections. Your tenant evacuates immediately, but the repair timeline doesn’t accelerate just because you need the rent. A $2,000 monthly rental becomes $12,000 in lost income over six months before your tenant moves back in. During this entire window, your mortgage payment arrives on schedule, property taxes remain due, and utilities continue running on an empty unit. Without disruption coverage, you write checks for expenses on a property that generates zero income.

Water Damage and Mold Create Extended Timelines

Water damage and mold remediation follow a similar but slightly faster pattern, usually taking 4 to 8 weeks depending on saturation extent and structural involvement. Mold testing and remediation can extend timelines in the Puget Sound region, where moisture problems are common. The drying phase compounds the timeline-structural materials must dry completely before contractors can assess hidden damage or begin repairs. Your tenant cannot return until the property passes inspection and remediation is complete, which means your income stays at zero throughout the entire process.

Natural Disasters Displace Tenants for Months

Natural disasters hit harder in some regions than others, but the Puget Sound area faces genuine exposure to wind damage, flooding, and occasional earthquake damage that displaces tenants for extended periods. A severe windstorm that damages your roof or causes water intrusion can knock your rental unit offline for 2 to 3 months while contractors work through backlogs. Flooding events prove particularly brutal because they trigger both immediate displacement and lengthy drying and remediation phases that can stretch 6 to 8 weeks or longer depending on water damage severity.

The Math Behind Income Loss

The financial reality of these scenarios demands more than hope. A property generating $24,000 annually in rent faces $2,000 to $12,000 in lost income during a single repair event, yet most landlords carry no coverage for this gap. Disruption coverage fills exactly this hole. When you calculate whether this coverage makes sense for your property, multiply your monthly rent by the longest reasonable repair timeline you might face, then compare that number to the annual premium cost. For most Puget Sound landlords, a $2,000 monthly rental with potential 4 to 6 month repair scenarios justifies coverage costs that typically run $300 to $600 annually.

How Coverage Timing Affects Your Protection

The waiting period of 30 to 60 days means you absorb the first month’s loss yourself, but coverage kicks in precisely when extended repairs begin compounding your financial exposure. Properties in older buildings or those prone to weather exposure face higher disruption risk and benefit most from this protection. Newer construction with modern systems experiences fewer catastrophic events, but when fire or water damage does occur, the same income loss timeline applies regardless of building age. Understanding your property’s specific vulnerabilities helps you determine whether standard coverage limits match your actual risk profile or whether you need enhanced protection.

Choosing Disruption Coverage That Matches Your Property’s Real Exposure

Assess Your Property’s Actual Risk Profile

Start with your property’s actual risk profile, not generic insurance industry standards. A 1950s wood-frame house in a flood-prone area faces fundamentally different disruption risks than a 2015 concrete-construction apartment building on higher ground. Walk your property and identify specific vulnerabilities: roof age and condition, proximity to water sources, electrical system condition, and local weather patterns in the Puget Sound region. Properties with roofs over 20 years old experience higher wind damage risk; properties within 500 feet of creeks or in low-lying areas face genuine flood exposure; older plumbing systems fail more frequently than modern PEX installations. This assessment determines which covered events matter most to your coverage decision. A property in a wildfire zone needs different protection priorities than one in an urban area where fire typically comes from structure fires rather than external events.

Insurance carriers in Washington state can provide risk assessments based on your specific address and building characteristics, helping you understand which scenarios pose the greatest financial threat to your rental income.

Calculate Your Actual Income Loss Exposure

Take your monthly rent and multiply it by the longest repair timeline realistic for your property type and condition. A $2,500 monthly rental facing a potential 5-month water damage scenario needs at least $12,500 in coverage; a $1,800 monthly rental with similar exposure requires $9,000 minimum. Add 20 percent to that number as a safety margin for extended timelines or contractor delays, which occur regularly in the Puget Sound region during peak construction seasons.

Then review what different carriers actually offer. Some carriers cap monthly payouts at $3,000 regardless of your actual rent; others reimburse the full amount you lost. A few carriers limit total payout to 6 months of rent while others extend to 12 months. These differences matter enormously. A property that generates $3,500 monthly with a 6-month coverage limit receives only $21,000 in total protection, which leaves a $10,500 gap if repairs extend beyond six months.

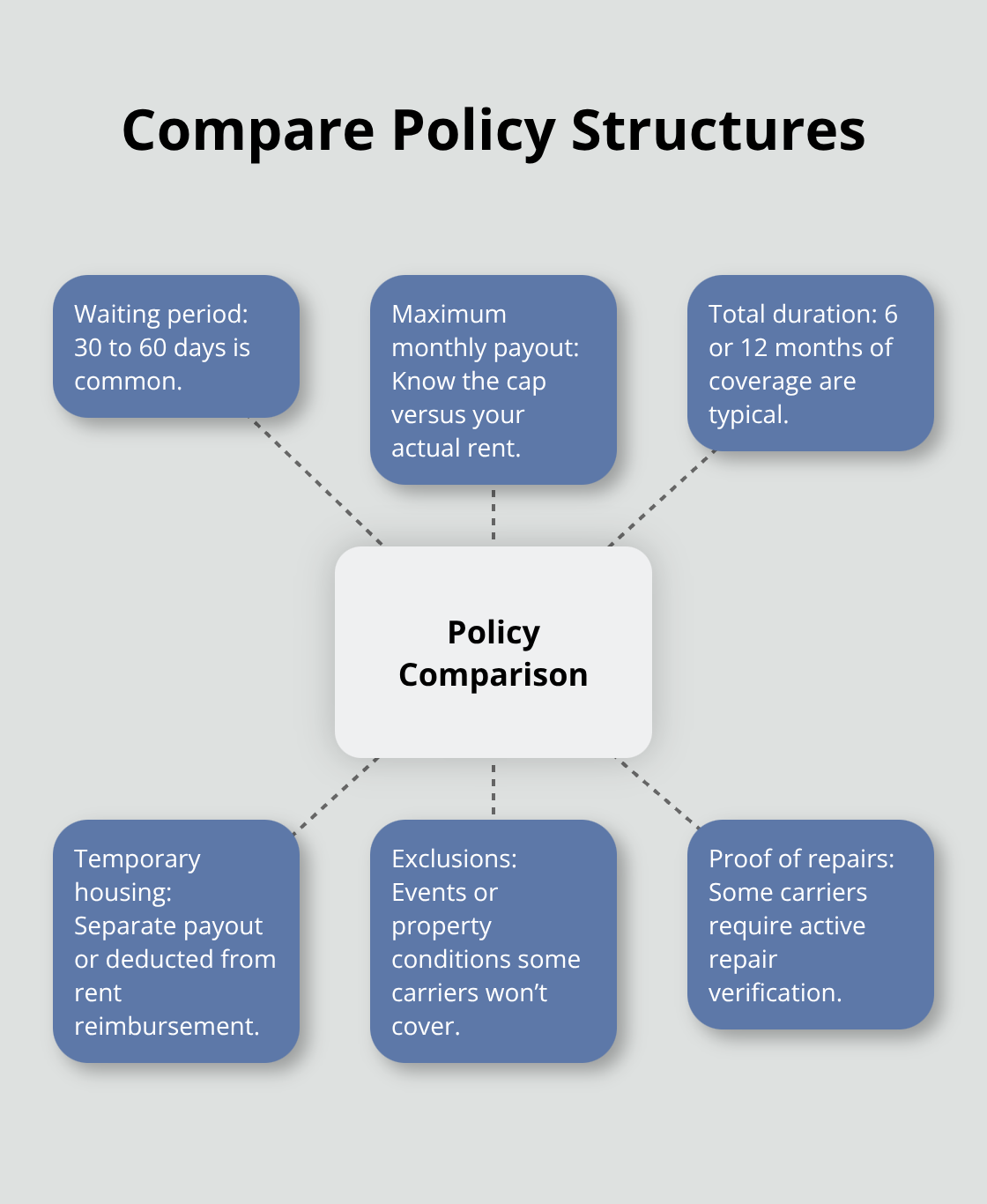

Compare Coverage Structures Across Multiple Carriers

Carriers differ significantly on whether they cover temporary housing costs as separate payouts or deduct those costs from your rent reimbursement. Request detailed policy specifications from at least three carriers and compare the actual dollar amounts each would pay during your longest realistic repair scenario. Focus on these specific elements: the waiting period length (30 to 60 days is standard), the maximum monthly payout amount, the total coverage duration (6 or 12 months), whether temporary housing costs reduce your rent reimbursement or stand as separate coverage, and any exclusions for specific events or property conditions.

A property in the Puget Sound region with water damage exposure might prioritize carriers that cover mold remediation costs and extended drying timelines. A property with older electrical systems might prioritize carriers that don’t exclude fire damage from aging infrastructure. Your specific vulnerabilities should drive which policy features matter most to your decision.

Match Coverage Limits to Your Financial Exposure

The gap between what you think you need and what you actually purchase often determines whether disruption coverage truly protects you. A $2,000 monthly rental with a potential 4-month repair scenario requires $8,000 in minimum coverage, but a 6-month scenario demands $12,000. If you purchase a policy with only $6,000 in total coverage, you face a $6,000 shortfall in the longer scenario. Insurance carriers structure policies to appeal to different landlord situations, so comparing three or more options reveals which carrier’s structure aligns with your property’s actual exposure rather than forcing you into a one-size-fits-all solution.

Final Thoughts

Landlord tenant disruption coverage protects your rental income when fire, water damage, or other covered events force tenants out and halt rent collection. The financial exposure is real: a single repair event costs you thousands in lost rent while your mortgage, taxes, and utilities continue. Most Puget Sound landlords underestimate how quickly these costs accumulate, which is why understanding your property’s specific vulnerabilities matters more than generic coverage recommendations.

Calculate your monthly rent and multiply it by the longest repair timeline realistic for your property type and location-that number represents your actual income loss exposure. Then compare what different carriers offer in terms of waiting periods, monthly payouts, and total coverage duration. A policy that caps monthly reimbursement at $2,500 when your rent is $3,000 leaves you exposed, and a policy with only six months of coverage when your property faces potential eight-month repair scenarios creates a gap you absorb yourself.

Contact H&K Insurance Agency to review your current coverage and identify whether landlord tenant disruption coverage makes sense for your rental properties. We help Puget Sound landlords compare options from multiple carriers and customize protection that matches their actual property exposure. The cost of this coverage typically runs $300 to $600 annually, which is minimal compared to the financial exposure you face without it.