Landlord Insurance Guide: Get The Right Coverage For Rental Properties

Owning a rental property means protecting your investment from real financial threats. Most landlords discover they’re underinsured only after something goes wrong-a tenant causes damage, a liability claim arrives, or the property sits vacant.

We at H&K Insurance Agency created this landlord insurance guide to show you exactly what coverage matters and what gaps could cost you thousands. The right policy makes the difference between a manageable loss and a financial disaster.

What Landlord Insurance Actually Covers

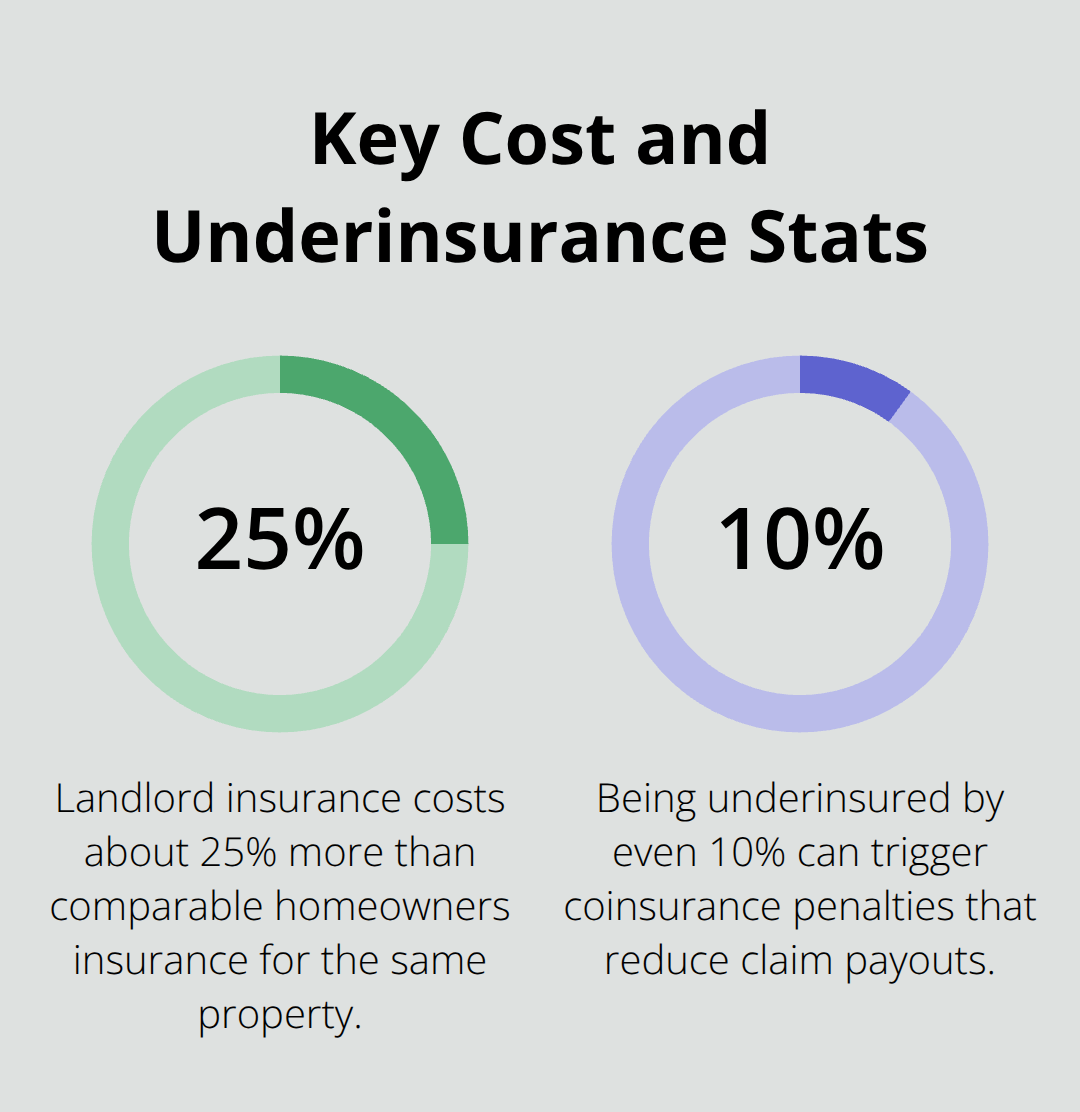

Landlord insurance protects rental income and addresses tenant-specific risks that standard policies ignore. A homeowners policy covers you when you live in the property, but the moment you rent it out, that coverage becomes inadequate or void. Insurance Information Institute data shows landlord insurance costs about 25% more than homeowners insurance for the same property, reflecting the higher liability and income-loss exposure that comes with tenants.

The dwelling coverage protects your building structure, permanent fixtures, and other structures on the property, but it deliberately excludes your tenants’ personal belongings-that’s their responsibility through renters insurance. Liability coverage is where landlord insurance truly separates itself from homeowners policies. If a tenant or visitor gets injured on your rental property and sues you, liability coverage handles medical expenses, legal fees, and damages up to your policy limit. This matters because rental properties statistically see more foot traffic and longer-term occupancy, creating higher injury risk than owner-occupied homes.

Loss of Rents: Your Income Protection Layer

Loss of rents coverage replaces your lost rental income when a covered loss makes the property uninhabitable-a fire, major water damage, or other disaster. This coverage typically lasts up to 12 months depending on your policy tier. Without this protection, you pay your mortgage while collecting zero rent, a financial trap that forces many landlords into emergency decisions.

Why Your Lender Requires It

If you have a mortgage on the rental property, your lender mandates landlord insurance as a condition of the loan. Lenders protect their collateral, and they won’t accept the liability exposure of a property covered only by a homeowners policy. Even if your property is paid off, skipping landlord insurance exposes you to catastrophic repair costs that homeowners insurance won’t cover. A significant structural loss-roof replacement averaging $8,000 to $15,000, foundation repairs, or major electrical work-falls squarely on you without proper coverage.

Rebuild Cost Versus Purchase Price

Most landlords make a critical mistake by insuring their property at the purchase price rather than rebuild cost. Rebuild cost is what it actually takes to reconstruct the building from the ground up, and it’s often higher than what you paid. If your property cost $300,000 but would cost $380,000 to rebuild today with current labor and materials, insuring it at $300,000 leaves you severely underinsured. Insurance Information Institute guidance emphasizes getting a professional rebuild cost estimate before shopping for quotes. Without matching your dwelling coverage to actual rebuild value, you face coinsurance penalties that can reduce your payout significantly when you file a claim.

What Comes Next in Your Coverage Strategy

Understanding what landlord insurance covers is only half the battle. The next step involves identifying which specific coverage types matter most for your rental property and recognizing the gaps that could leave you exposed.

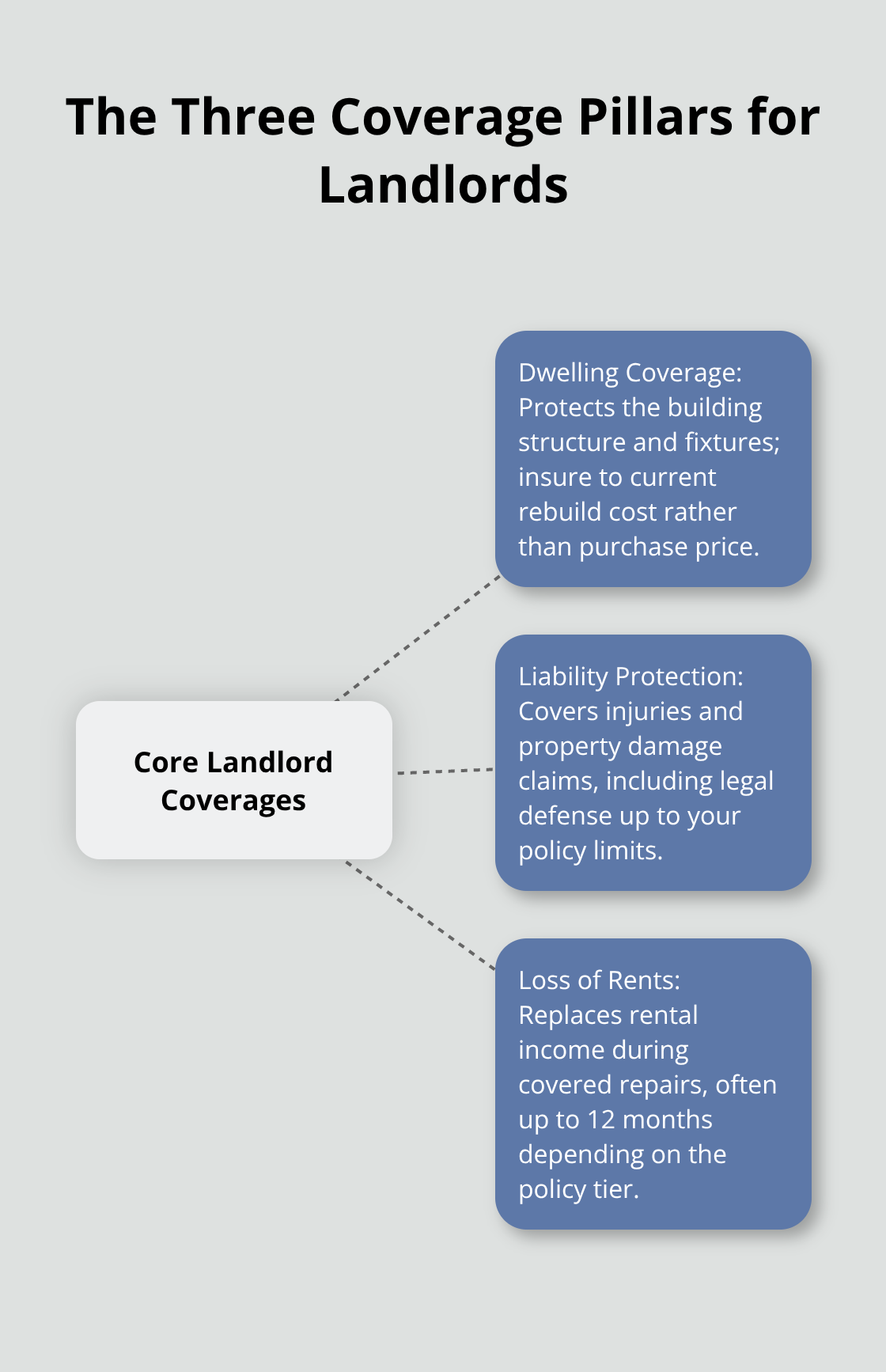

The Three Coverage Pillars Every Landlord Needs

Dwelling coverage, liability protection, and loss of rents form the foundation of any functional landlord policy. Each pillar serves a distinct purpose, and understanding how they work prevents costly mistakes when claims arrive.

Dwelling Coverage: Protecting Your Building Structure

Dwelling coverage protects the structure itself-walls, roof, permanent fixtures, and other buildings on the property. The coverage amount matters far more than most landlords realize. Many landlords insure based on purchase price rather than rebuild cost, creating a dangerous gap when claims occur. A $350,000 purchase price doesn’t mean $350,000 in rebuild value; current labor and material costs in the Puget Sound region often push rebuild expenses 15 to 25 percent higher than historical purchase prices.

If you’re underinsured by even 10 percent, coinsurance penalties can slash your payout by thousands. Get a professional rebuild estimate before requesting quotes-this single step prevents most major underinsurance problems. The Insurance Information Institute reports that many landlords make this mistake, leaving themselves exposed to significant financial loss.

Liability Coverage: Your Legal Protection

Liability coverage protects you when someone gets injured on your rental property or you cause property damage to others. If a tenant’s guest slips on your stairs and sues for $50,000 in medical costs plus lost wages, your liability coverage handles the claim up to your policy limit, plus legal defense fees. Rental properties see higher injury frequency than owner-occupied homes because tenants and their guests spend more time on the property and face longer-term exposure to hazards.

A $300,000 liability limit works for single-family homes; multi-unit properties should carry $500,000 to $1,000,000. The specific amount depends on your net worth and the injury risk profile of your property. Older homes with stairs, pools, or high foot traffic warrant higher limits to match your actual exposure.

Loss of Rents: Income Protection During Repairs

Loss of rents coverage replaces your monthly rental income when a covered loss makes the property uninhabitable-typically for up to 12 months depending on your policy tier. This coverage prevents the scenario where you pay the mortgage while collecting zero rent, a situation that forces many landlords to accept inadequate repair work just to get tenants back in place.

If your property generates $2,000 monthly rent and sits damaged for six months, loss of rents covers the $12,000 income gap while repairs happen. Without this protection, you absorb that $12,000 loss yourself while your lender still demands the mortgage payment.

Aligning Coverage with Your Actual Property Value

Standard policies don’t automatically adjust as rents increase or rebuild costs climb. Review your dwelling coverage annually and request updated rebuild estimates every three to five years, especially in high-appreciation markets. Liability limits should match your net worth and the injury risk profile of your specific property.

Loss of rents caps vary by insurer; some policies limit it to 12 months of fair rental value while others offer longer periods. Compare the actual dollar amounts in quotes rather than just the policy names. The difference between a $300,000 dwelling limit and a $350,000 limit might be $100 annually, but that $50,000 coverage gap could cost you tens of thousands in an actual loss.

When shopping for quotes, request identical coverage amounts across carriers so you’re comparing actual price differences, not coverage gaps disguised as savings. This approach reveals which insurers truly offer competitive rates for your specific property and risk profile. The gaps in your coverage often surface only during the claims process-the time to fix misalignment is before something happens.

What Your Landlord Policy Won’t Cover

Most landlords assume their policy covers everything that happens on the property, then face denial letters when they file claims. Standard landlord policies explicitly exclude tenant-caused damage, which creates a massive blind spot for property owners. If a tenant punches a hole in the drywall, damages flooring, or causes water damage through negligence, your landlord insurance won’t pay for repairs. Your only recourse is the security deposit, which rarely covers the actual cost of damage.

A single incident of tenant-caused structural damage can cost $5,000 to $20,000, depending on the property and the type of damage.

Tenant Damage: The Coverage Gap That Costs Thousands

Many landlords absorb tenant-caused losses because pursuing tenants in small claims court consumes time and rarely recovers the full amount. The Insurance Information Institute notes that tenant-related claims represent a significant portion of landlord losses, yet standard policies treat them as the tenant’s financial responsibility rather than the landlord’s insurance problem. This gap forces you to choose between accepting losses or maintaining expensive security deposits that barely cover real damage costs. Consider that renters insurance places responsibility on tenants to protect their own belongings and interests.

Vacant Properties and Water Damage Exposure

Vacant properties introduce a different exposure that standard landlord policies handle poorly. If your rental sits empty for more than 30 days, your dwelling coverage may not apply to water damage, theft, or vandalism. Insurers treat vacant properties as higher risk because no one monitors them daily, and damage can spread unchecked for weeks. A frozen pipe in a vacant property during winter can cause $15,000 to $40,000 in water damage before discovery, and your standard landlord policy may deny the claim because the property was unoccupied.

Natural Disasters: Flood and Earthquake Exclusions

Natural disasters create the third major gap that catches landlords off guard. Standard landlord policies exclude flood damage entirely, leaving you exposed if your property sits in a flood-prone area or near drainage patterns that concentrate water during heavy rain. The Puget Sound region experiences increasing rainfall intensity, and several neighborhoods in Bremerton and surrounding areas face elevated flood risk. Earthquake damage is also excluded from standard policies, despite Washington State’s documented seismic activity. A major earthquake could damage your structure, but your landlord policy won’t cover reconstruction costs.

Adding Protection for Catastrophic Risks

You need separate flood and earthquake endorsements to close these gaps, and they cost extra because they represent genuine catastrophic risk. Request specific quotes that include flood and earthquake coverage, then compare the actual dollar increases rather than assuming they’re prohibitively expensive. Many landlords pay $200 to $400 annually for these endorsements and consider it essential protection given the region’s exposure to both hazards. Umbrella liability insurance can also extend your protection beyond standard policy limits when catastrophic events occur.

Final Thoughts

Matching your specific property to the right coverage amounts and carriers determines whether landlord insurance protects you or leaves you exposed. Start with a professional rebuild cost estimate rather than your purchase price, since this single step prevents coinsurance penalties that slash payouts when claims happen. Calculate your monthly rental income and request loss of rents coverage that reflects at least six to twelve months of that income, then set liability limits that align with your net worth and property risk profile.

Request quotes from multiple carriers using identical coverage amounts so you reveal genuine price differences instead of gaps disguised as savings. The Insurance Information Institute reports that landlord insurance costs vary significantly by location and property features, making apples-to-apples comparisons essential to avoid overpaying. Pay close attention to what each quote excludes, particularly flood and earthquake coverage, since these gaps expose you to catastrophic losses in the Puget Sound region.

We at H&K Insurance Agency represent multiple top carriers and compare rates to customize packages that match your actual coverage requirements. Contact us to discuss your rental property needs and receive quotes tailored to your specific situation, or visit our landlord insurance guide to learn more about protecting your investment.