Boat Insurance Discounts: Ways to Save on Your Watercraft

Boat insurance doesn’t have to drain your budget. We at H&K Insurance Agency know that smart choices-from safety upgrades to bundling policies-can significantly lower what you pay each year.

This guide shows you the most effective boat insurance discounts available right now. You’ll learn exactly which steps reduce your premiums and how to apply them to your coverage.

Safety Upgrades and Certifications That Lower Your Boat Insurance Costs

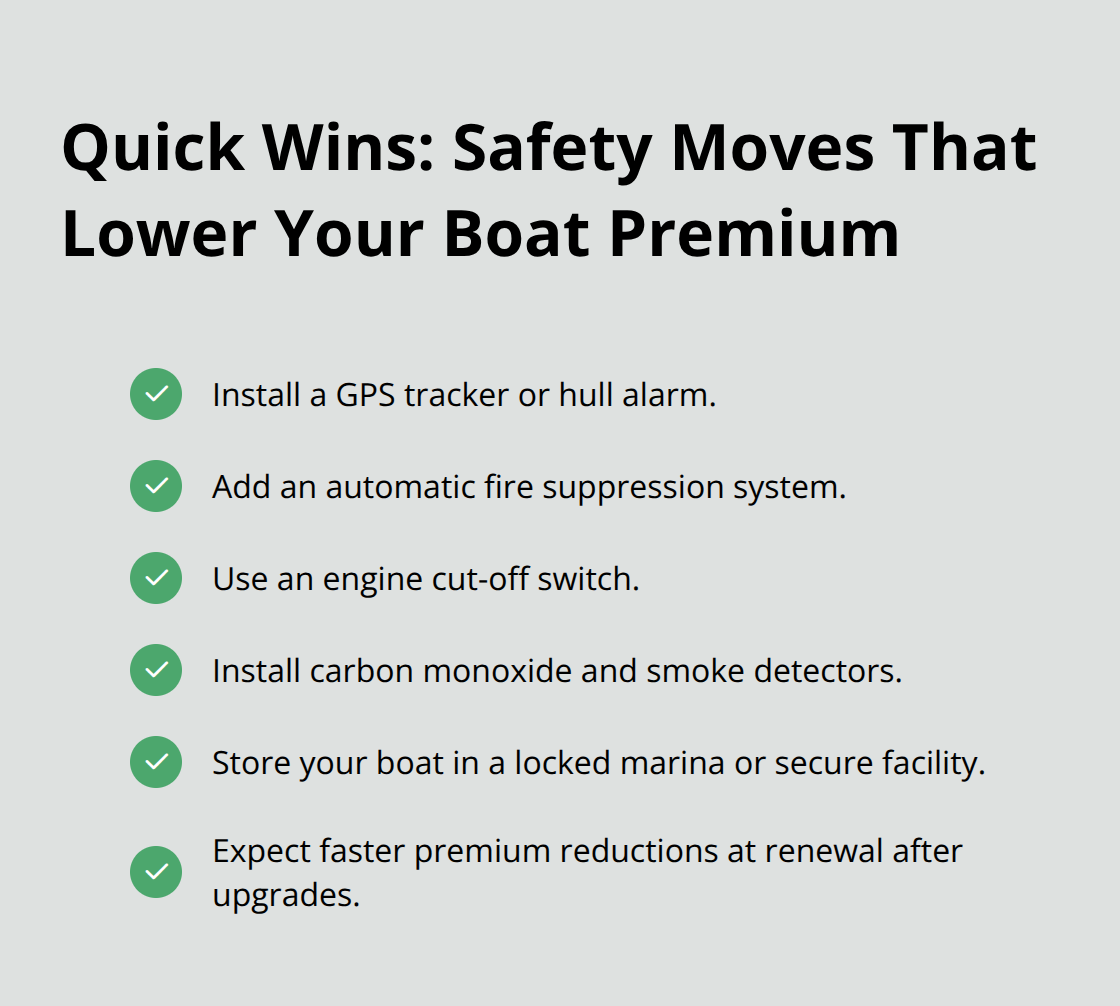

Install Approved Safety Equipment on Your Boat

Certified safety equipment cuts your premiums faster than almost any other discount available. Automatic fire suppression systems, engine cut-off switches, carbon monoxide detectors, and smoke detectors all qualify for direct reductions from most insurers. GPS trackers and hull alarms reduce theft risk in the eyes of underwriters, which translates to lower rates immediately. The investment in equipment pays for itself quickly when your premium drops at renewal.

Secure storage matters too-keeping your boat in a locked marina or facility instead of leaving it exposed cuts your rate because theft risk plummets.

Complete a Boating Safety Course for Immediate Savings

An approved boating safety course ranks among the easiest discounts to claim. The US Coast Guard Auxiliary offers courses that most insurers recognize and reward with rate reductions. The BoatUS Foundation provides a free online course that qualifies you for discounts with BoatUS and potentially other carriers. Paid options typically cost under $100, and the premium savings often recover that cost in your first year. Some insurers offer larger discounts if you complete the course before purchasing your policy rather than after you’re already covered. Insurers view safety training as a clear signal that you understand boating risks and take them seriously, which directly lowers their claims exposure.

Maintain Certifications and Document Your Training

A USCG captain’s license or OUPV license demonstrates serious commitment to safe boating, and many insurers offer discounts for licensed operators. Membership in the Power Squadron or Coast Guard Auxiliary also qualifies for premium reductions in most states. You should keep records of every course you complete and every certification you earn, because you’ll need to provide proof when you request discounts. Update your insurer whenever you add new training or equipment to your boat. Some policies include disappearing deductibles that shrink by 25% after each claim-free year, potentially reaching zero (which means your safety record compounds your savings over time). The combination of safety equipment, training, and a clean claims history creates the strongest discount profile available to boat owners, and these advantages stack when you explore bundling options with your other policies.

How Bundling Saves You More Than Single-Policy Coverage

Stack Multiple Policies for Immediate Savings

Bundling boat insurance with your auto and home policies offers the convenience of having all your insurance needs managed under one roof. When you combine boat coverage with auto or home insurance, most carriers reduce your overall premium by stacking discounts across multiple policies. The math works because insurers reward customer loyalty and reduce administrative costs when they manage multiple policies under one account.

Understand the Trade-Off Between Convenience and Coverage

A bundled policy means one bill, one renewal date, and one point of contact when you need to make changes or file a claim. However, bundling comes with a critical trade-off that most boat owners overlook: separate boat insurance provides superior coverage compared to bundled policies because specialized boat insurers understand watercraft-specific risks that general home and auto insurers do not. Boat-specific policies deliver more comprehensive coverage for damages, liability, medical payments, and uninsured boaters than bundled options typically offer. Filing a boat claim on a bundled policy could impact your other policies’ premiums or renewal status, which means separating boat coverage isolates risk to the boat and protects your auto and home policies from boat-related claims.

Maximize Discounts with Multiple Watercraft

If you own multiple boats, stacking them on a single marine policy unlocks a multi-boat discount that reduces your rate further. Loyalty discounts compound over time as you maintain a clean claims history with your carrier. Some carriers reduce your deductible by 25% after each claim-free year through disappearing deductible programs, which means your long-term savings accelerate the longer you stay claim-free.

Work with a Marine Specialist to Find Your Best Option

The key is shopping with an agent who represents multiple underwriters-not relying on online quotes alone-because a marine specialist can identify which carrier offers the best combination of coverage depth and discount stacking for your specific situation. An independent agent can show you exactly how much you’ll save by bundling versus keeping your boat policy separate, and the answer depends on your unique coverage needs and risk tolerance rather than just convenience. Whether that means bundling everything together or keeping your boat policy separate, a specialist who understands both bundling benefits and boat-specific coverage gaps will help you make the right choice. Your maintenance habits and usage patterns also affect which bundling strategy works best for your boat, which is why the next section focuses on how your daily boating decisions impact your premiums.

How Your Daily Boating Habits Shape Insurance Rates

Insurers don’t just care about what you own-they care about how you use it. Your maintenance records, annual usage patterns, and storage methods directly influence your premium because they tell underwriters exactly how much risk you represent. A boat that sits in a secure facility for eight months per year costs less to insure than one that runs 200 days annually, and a vessel with documented maintenance beats one with a questionable history every time. Boat owners save hundreds annually simply by changing how they use and store their watercraft, which means the decisions you make right now affect what you’ll pay for years to come.

Documentation Proves You Prevent Claims

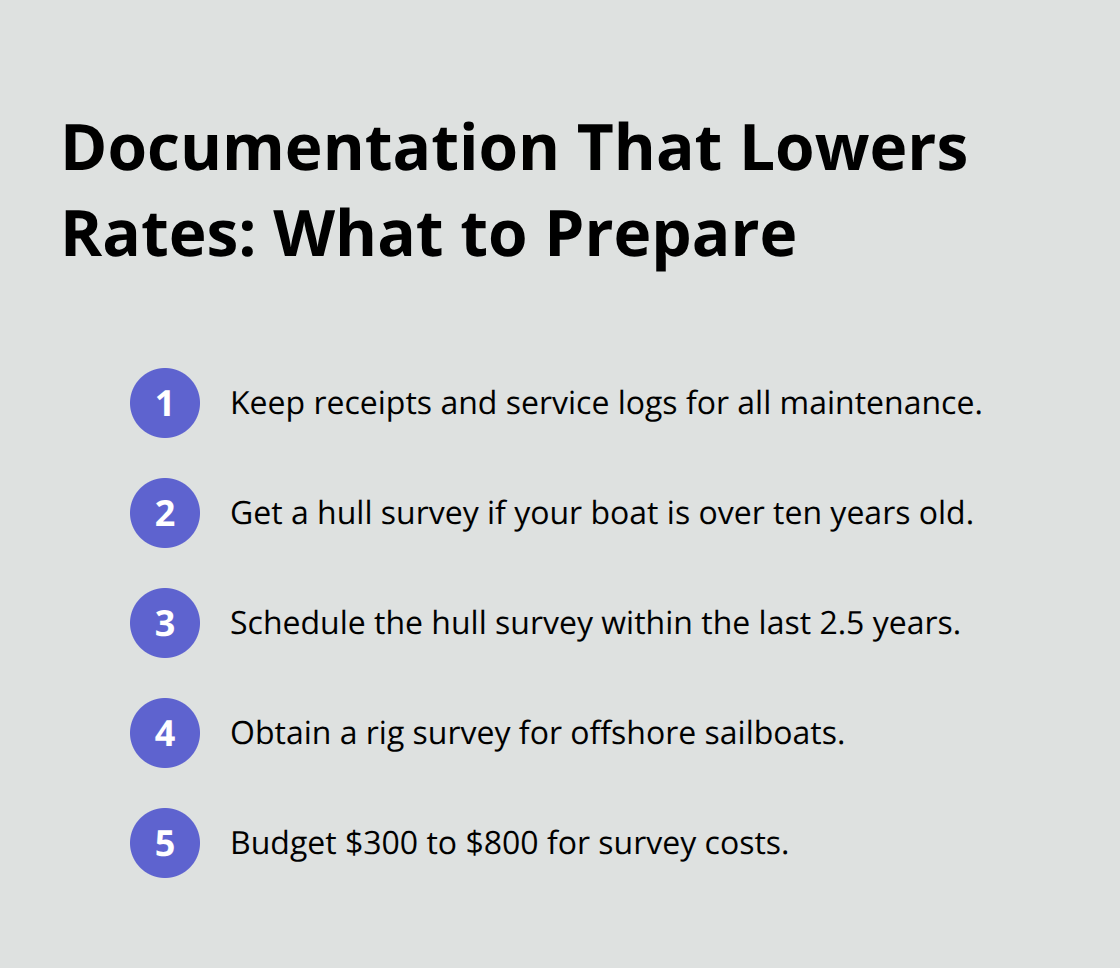

Maintenance records are your strongest argument for lower rates at renewal time. Insurers view detailed service histories as evidence that you prevent breakdowns, reduce mechanical failures, and lower claims likelihood. Keep receipts and service logs for every engine service, hull inspection, electrical system check, and seasonal maintenance task-these documents prove you’re a responsible operator when you request rate reviews. Older boats especially benefit from recent surveys; if your vessel is over ten years old, obtain a hull survey completed within the last 2.5 years because many insurers require one before they’ll quote competitive rates. For sailboats heading offshore, insurers often demand a detailed rig survey to validate your boat’s condition and seaworthiness. These surveys cost $300 to $800, but they unlock better pricing and prevent policy denials when you need coverage most.

Secure Storage Cuts Theft Risk and Premiums

Store your boat in a locked marina or secure facility rather than leaving it exposed, because theft risk drops dramatically and insurers reward this choice with immediate rate reductions. A boat sitting in an open field faces higher premiums than the same vessel locked behind a gate-insurers have actuarial data proving this distinction matters for claims frequency and theft losses. Your storage choice signals to underwriters whether you take ownership seriously, and that signal translates directly into your annual cost.

Usage Patterns Drive Pricing More Than Most Owners Realize

How often and how far you boat directly affects your annual premium. Year-round operation costs more to insure than seasonal use because constant exposure increases accident and mechanical failure risk. Some insurers offer lower rates for boats used only three to six months annually, while others charge less for vessels kept within specific geographic regions or lower-risk areas. Document your actual usage honestly when you quote policies, because underreporting mileage or operating months creates coverage gaps that leave you exposed when claims happen. If you limit your boating to weekends on calm inland waters, your rate should reflect that lower-risk profile compared to someone running offshore in rough conditions regularly. This is where working with a knowledgeable agent becomes essential-they know which carriers reward occasional use with meaningful discounts and which ones don’t differentiate based on usage patterns. Some newer policies include usage-based or telematics options where the insurer tracks how you actually operate the boat, and responsible boaters can earn discounts of 10 to 15 percent by proving their safe habits through real data rather than promises.

Final Thoughts

The boat insurance discounts covered in this guide represent real money in your pocket at renewal time. Safety equipment, boating courses, bundled policies, and responsible maintenance habits all work together to lower what you pay annually. The strongest savings come from combining multiple strategies rather than relying on a single discount, because insurers reward owners who demonstrate commitment to safety and responsible boat ownership across multiple areas.

Start by reviewing your current coverage and identifying which discounts you already claim. Check whether your safety equipment qualifies for reductions, confirm that your boating certifications appear in your policy file, and calculate whether bundling your boat with auto and home coverage actually saves money compared to a specialized marine policy. Pull together your maintenance records and storage information, because these details matter when you request rate reviews at renewal.

We at H&K Insurance Agency specialize in comparing rates across multiple carriers to find the combination of boat insurance discounts and coverage that works best for your situation. As a locally owned, independent agency serving the Puget Sound region, we represent top local and national carriers, which means we can show you exactly how much you save by bundling and which safety upgrades unlock the biggest reductions with each underwriter. Contact us today to discuss your boat insurance and discover how much you can save with the right strategy.