Bremerton Auto Insurance Rates: What Drivers Pay in Puget Sound

Bremerton auto insurance rates have climbed steadily over the past few years, leaving many drivers wondering if they’re paying too much. The Puget Sound region faces unique pricing pressures that don’t always apply elsewhere in Washington State.

We at H&K Insurance Agency help local drivers understand what drives these costs and how to cut through the noise. This guide breaks down the real numbers, explains why your rate might be higher than your neighbor’s, and shows you concrete ways to save.

What You’ll Actually Pay for Car Insurance in Bremerton

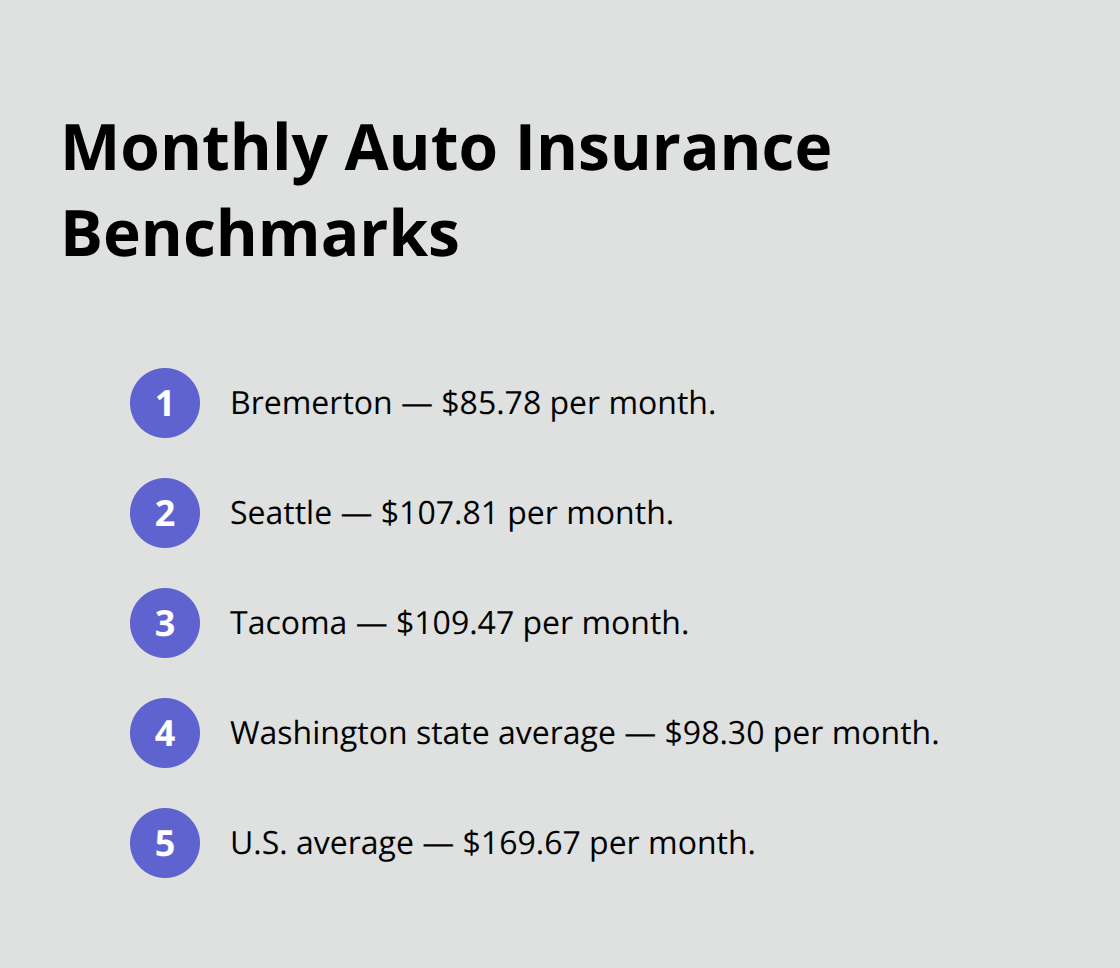

The average driver in Bremerton pays about $85.78 per month for car insurance, according to SmartFinancial data. That breaks down to roughly $1,029 annually for most coverage types. If you compare this to Seattle or Tacoma, you’re already ahead-those cities average $107.81 and $109.47 monthly respectively. Washington state as a whole sits at $98.30 per month, which means Bremerton drivers enjoy rates about 12% below the state average. The national average hovers around $169.67 monthly, so living in the Puget Sound region gives you a genuine pricing advantage even though costs have climbed in recent years.

The Real Cost Breakdown by Coverage Type

Full coverage in Bremerton runs approximately $80 per month, while liability-only policies average $40 monthly. These numbers matter because they show you’re not locked into expensive coverage. If you drive an older paid-off vehicle, dropping to liability-only could cut your costs in half. The catch is that Washington requires minimum liability coverage of 25/50/10, so you cannot go below that threshold legally. Within Bremerton’s ZIP codes, you’ll see variation-98310 and 98337 run cheaper at around $80 for full coverage, while 98314 climbs to $140 monthly for full coverage due to higher theft and claim frequency in that neighborhood. This ZIP code spread matters more than most drivers realize; a five-minute drive could mean a $60 monthly difference.

Age Creates the Biggest Rate Difference

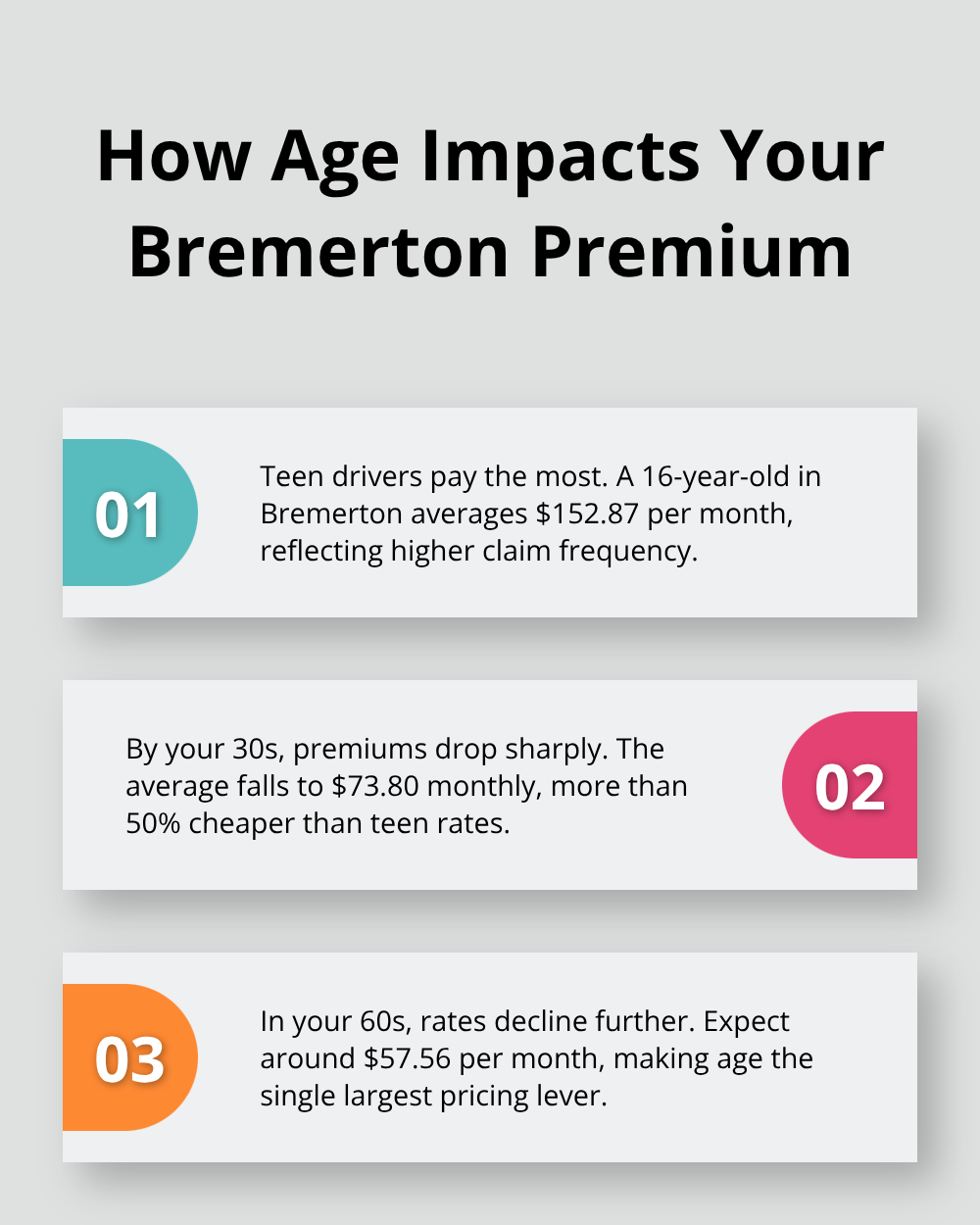

Your age determines more of your premium than most other factors combined. A teenager in Bremerton pays roughly $152.87 monthly on average, while someone in their 30s pays $73.80-that’s more than 50% cheaper. Someone in their 60s drops to $57.56 monthly, making age the single largest rate lever available.

The jump from teenage years to your 20s saves you about $33 per month, and the drop from your 20s to your 30s saves another $46 monthly. These age-based differences reflect actual claim data that insurers track across millions of drivers.

Vehicle Type and Safety Features Shape Your Cost

Your vehicle type ranks second in importance after age. A 2014 Honda CR-V quotes around $49.38 monthly while a 2022 Kia Forte reaches $113.70 for the same driver-newer cars with advanced safety features sometimes cost less to insure than older models because repair technology and safety ratings matter more than age alone. Insurers reward vehicles equipped with collision avoidance systems, automatic braking, and lane-keeping assistance. The make and model you choose affects both repair costs and claim frequency, which insurers factor into your rate.

Driving History and Parking Location Impact Rates

Your driving history and claims record create permanent rate impacts. One at-fault accident can raise your premium by 15-40% depending on your insurer, and that increase typically lasts three to five years. Where you park your vehicle matters too; securing garage storage versus street parking can reduce your premium by signaling lower theft risk to insurers. These factors work together to explain why two drivers in the same ZIP code pay different rates. Understanding what moves your rate up or down helps you identify which changes actually save money versus which ones don’t.

Why Your Rate Differs From Your Neighbor’s

Age Dominates Pricing More Than Any Other Factor

Age creates the largest rate swing in Bremerton insurance pricing, and the numbers prove it decisively. A 16-year-old driver pays $152.87 monthly while a 30-year-old pays $73.80 for the same coverage-that’s a $79 monthly gap or roughly $948 annually. Move into your 50s and the rate drops further to $57.85 monthly. Insurers base these differences on decades of claims data showing that younger drivers file more claims and cause more accidents. The experience gap matters enormously. A driver in their 20s still pays $119.60 monthly on average, nearly double what a 40-year-old pays at $76.90. These aren’t estimates or projections; SmartFinancial data from the Puget Sound region confirms this pattern consistently.

If you’re a young driver, this reality stings, but understanding it helps you identify legitimate discounts. Some insurers like PEMCO offer teen rates around $121.70 monthly, which beats the regional average by roughly $31 per month. USAA comes in around $130.16 for the same age group. Shopping specifically for companies that price teens competitively saves real money monthly.

Vehicle Selection Creates the Second-Largest Rate Swing

Vehicle selection matters far more than most drivers realize. A 2014 Honda CR-V costs roughly $49.38 monthly to insure while a 2022 Kia Forte reaches $113.70 for an identical driver profile-that’s a $64 monthly difference driven entirely by the vehicle itself. Safety features matter more than model year; the newer Kia actually costs less than some older models because its collision avoidance and automatic braking systems reduce claim frequency and repair complexity. A 2005 GMC Sierra runs about $54.23 monthly while a 2016 BMW 428 climbs to $121.32, illustrating how luxury vehicles and repair costs directly translate to higher premiums.

Driving Record and Claims History Create Permanent Impacts

Your driving record and claims history create permanent rate impacts that dwarf temporary factors. One at-fault accident typically raises your premium 15-40% depending on your insurer and can stick with you for three to five years. Multiple claims or violations trigger rate increases that compound over time, making the cost of poor decisions genuinely expensive. Where you park your vehicle also shifts your rate; garage storage signals lower theft risk compared to street parking in the same ZIP code.

What You Can Control Right Now

These three elements-age, vehicle type, and driving history-explain most rate variation you see across Bremerton drivers. Some factors you cannot change immediately, but vehicle selection and parking location offer concrete ways to reduce your premium right now. Understanding which levers actually move your rate helps you make smarter decisions about coverage and protection. The next section shows you specific strategies that work, starting with how bundling policies and leveraging safety features can cut your costs significantly.

How to Cut Your Bremerton Auto Insurance Costs

Bundle Home and Auto Policies for Immediate Savings

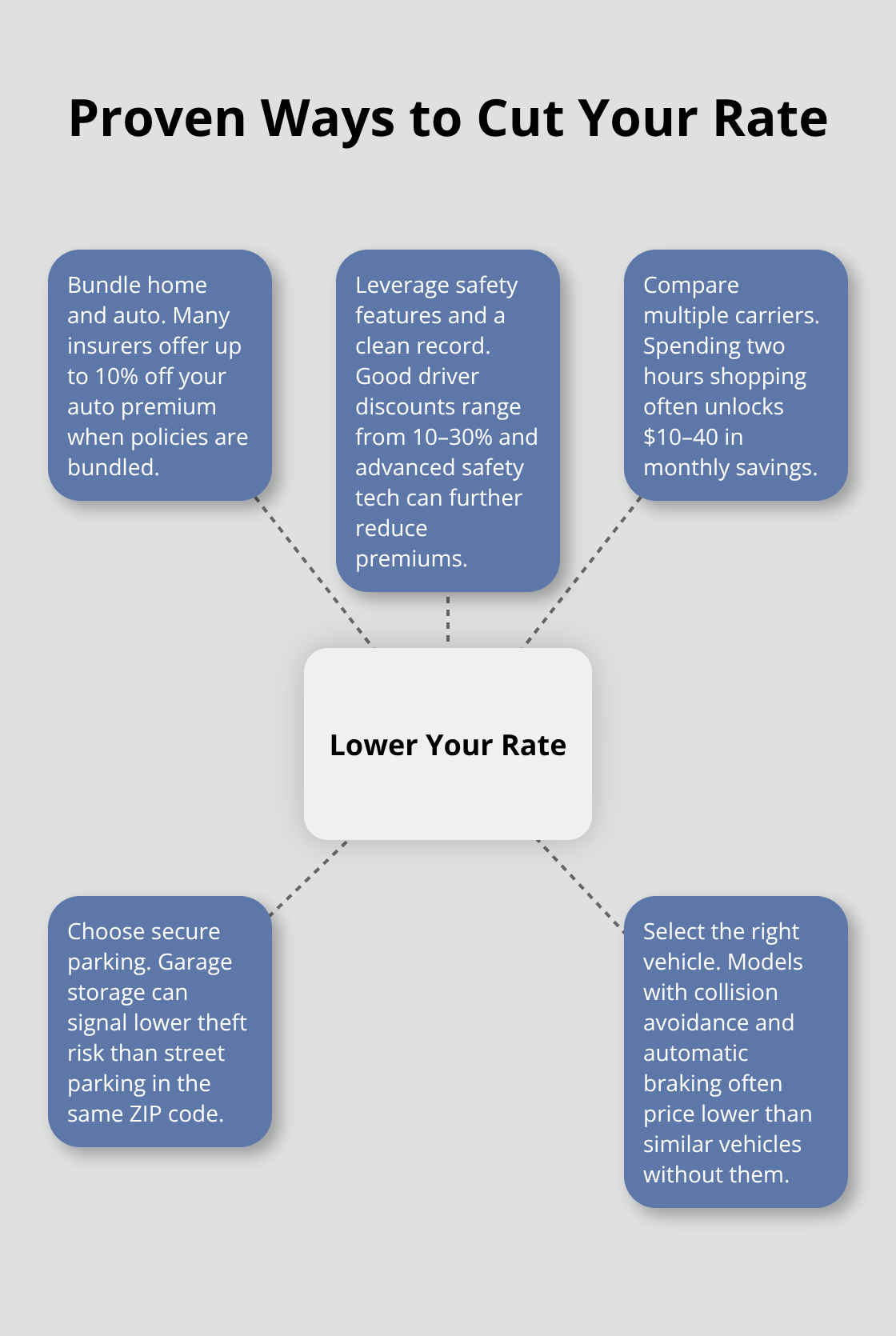

Combining your home and auto policies produces the fastest savings available to Bremerton drivers. Most insurers discount bundled policies by up to 10%, which translates directly to your bottom line. If you pay $85.78 monthly for auto insurance in Bremerton, adding a bundled home policy discount could save $8-21 monthly on your auto premium alone, plus additional savings on your home coverage. The math matters here: a 15% bundle discount on an $85.78 auto premium equals roughly $12.87 monthly or $154 annually. Many drivers miss this opportunity because they quote auto insurance separately from home insurance, never comparing what bundling actually costs. Shopping bundles requires getting quotes from the same insurer on both policies simultaneously-quoting them separately defeats the purpose and hides your actual savings. Start with listing your current home and auto carriers; if they differ, that gap represents money left on the table.

Leverage Safety Features and Driving Records

Vehicle safety features and your driving record unlock legitimate discounts that compound when combined. Insurers like USAA and PEMCO offer good driver discounts ranging from 10-30% for drivers with clean records over three to five years. If your vehicle has collision avoidance systems, automatic emergency braking, or lane-keeping assistance, mention these specifically when quoting-many insurers discount these features automatically, but some require you to flag them. The 2022 Kia Forte example from earlier illustrates this perfectly: advanced safety technology reduced that vehicle’s premium to $113.70 despite being newer than older alternatives. Shopping multiple carriers reveals how differently they value these discounts.

Compare Rates Across Multiple Carriers

Direct General quotes around $46.02 monthly in the Bremerton area while Chubb reaches $116.00 for comparable coverage-that $70 monthly gap exists because carriers weight age, vehicle type, and safety features differently. Spending two hours gathering quotes from multiple carriers typically yields $10-40 monthly savings compared to your current rate. USAA consistently ranks among Bremerton’s most competitive options at $73.00 monthly average, while Infinity Special leads at $51.98 monthly for select driver profiles. The carriers that quote lowest for your specific age, vehicle, and driving record may surprise you; regional pricing varies enormously. Requesting quotes from at least three carriers before renewing your policy separates drivers who pay fair rates from those overpaying by hundreds annually.

Final Thoughts

Bremerton auto insurance rates reflect three primary factors: your age, your vehicle type, and your driving history. Age creates the largest rate swing, with teenage drivers paying roughly double what drivers in their 30s pay monthly. Vehicle selection ranks second, where safety features and repair costs matter more than model year alone. Your driving record and claims history create permanent impacts that persist for years.

The real opportunity lies in what you can control right now. Bundling your home and auto policies saves 10% or more on your auto premium. Comparing rates across multiple carriers typically reveals $10-40 monthly savings you’re currently missing. Leveraging safety features and maintaining a clean driving record unlocks discounts that compound together.

Contact H&K Insurance Agency to discuss your current coverage and explore how much you could save on Bremerton auto insurance rates. Our local team will compare your options across multiple carriers and show you exactly where your rate stands against regional averages. Whether you’re a young driver, a parent insuring a teenager, or someone looking to cut costs on an existing policy, we’ll find the right protection at competitive prices.