Saltwater Boat Insurance: What Northwest Boaters Should Know

Saltwater boat insurance isn’t optional if you keep your vessel in the Pacific Northwest-it’s a necessity. The Puget Sound and coastal waters present real hazards that standard policies simply don’t cover.

We at H&K Insurance Agency work with Northwest boaters every day who discover gaps in their coverage too late. This guide walks you through what you actually need to protect your boat and your finances.

What Your Saltwater Boat Policy Actually Covers

Hull and Structural Damage Protection

Hull and structural damage coverage protects your boat against physical harm from collisions, groundings, storms, and saltwater corrosion-but the details matter far more than the basic description. In Washington, where 237,493 vessels are registered, most policies offer either Agreed Value or Actual Cash Value. Agreed Value is your stronger choice for saltwater boats because it locks in your boat’s worth before a total loss occurs, eliminating depreciation disputes when saltwater damage becomes catastrophic.

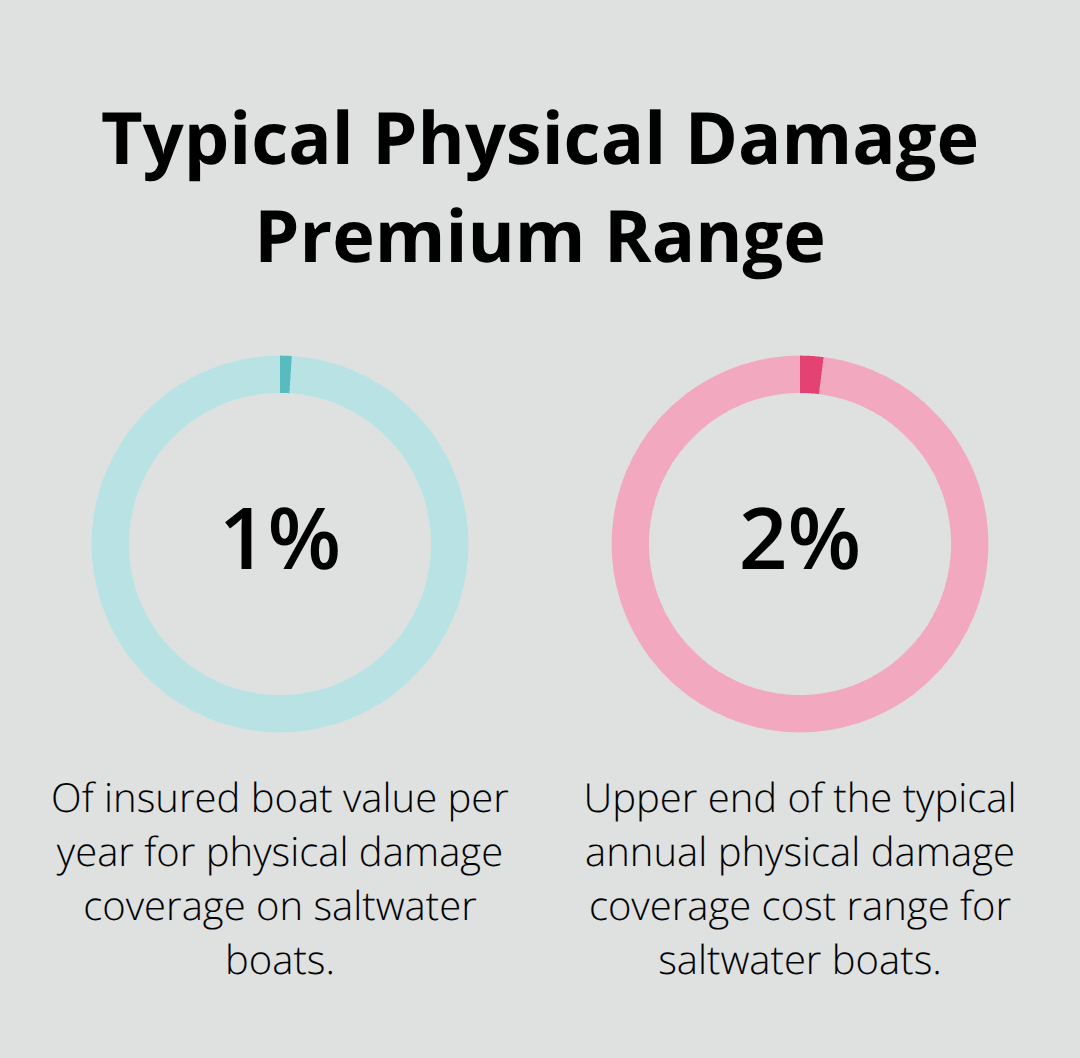

Physical damage coverage typically costs between 1% and 2% of your insured boat value annually, so a $40,000 saltwater cruiser runs roughly $400 to $800 per year. Pay close attention to deductibles for striking submerged objects-these often sit separate from your standard deductible and can range from $250 to $1,500. Saltwater-specific endorsements matter here: zinc anodes cost only $40 to $100 each but protect aluminum tubes from corrosion, and anti-corrosion coatings provide additional defense in Puget Sound’s harsh marine environment.

Liability Protection Shields Your Finances

Liability coverage, technically called Protection and Indemnity in marine insurance, covers injuries to other people and damage to their property caused by your boat. The U.S. Coast Guard reports roughly 100 recreational boating accidents annually in Washington, and a single serious injury claim can exceed $500,000 in medical costs alone. We recommend a minimum of $300,000 per occurrence, though many serious Northwest boaters carry $500,000 to $1 million in liability limits.

Cross-border boating adds complexity-if you cruise into Canadian waters, you need at least CAD 100,000 in liability coverage to enter. Environmental liability deserves special attention in Washington because the state’s Department of Ecology can levy fines up to $10,000 per day for fuel spills, making pollution and fuel spill endorsements genuinely valuable rather than optional extras.

Medical Payments and Uninsured Boater Protection

Medical payments coverage pays no-fault benefits for injuries to you, passengers, or guests aboard your boat, typically ranging from $1,000 to $10,000 per person. This coverage activates regardless of who caused the accident, making it invaluable for family boating on Puget Sound. Uninsured boater coverage protects you financially when an at-fault operator lacks insurance or carries insufficient limits-a realistic scenario given that Washington state doesn’t mandate boat insurance.

Choose uninsured boater limits that match your potential out-of-pocket exposure; if you carry $500,000 in liability, your uninsured boater limit should align with that threshold. Towing and emergency assistance endorsements cost relatively little but prevent catastrophic expenses-towing around Puget Sound averages $250 per hour, and multi-hour salvage operations regularly exceed $2,000. These endorsements transform what could become a financial disaster into a manageable claim, which is why selecting the right combination of coverages sets the foundation for your next decision: assessing your specific boat and how you actually use it.

Why Northwest Saltwater Conditions Demand Specialized Coverage

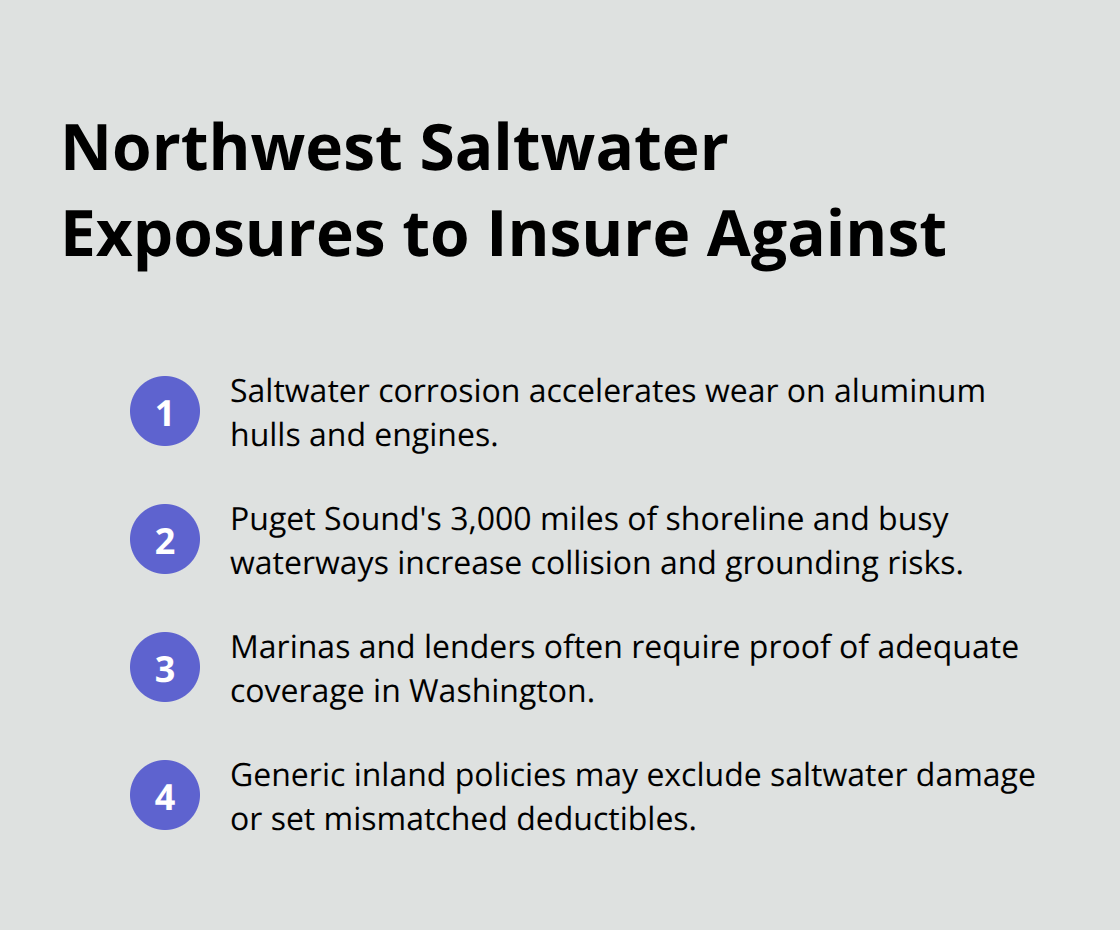

Puget Sound’s 3,000 miles of shoreline and major waterways create conditions that demand coverage tailored specifically to saltwater environments. Generic boat policies written for inland lakes miss critical exposures that Northwest boaters face daily. Saltwater corrosion attacks aluminum hulls and engines at a pace that freshwater operators never encounter. With more than 227,000 vessels registered in Washington, marinas and lenders increasingly require proof of adequate coverage before they allow your boat to stay in their slips or finance your purchase.

Standard policies often carry exclusions for saltwater damage or impose deductibles that don’t reflect the true cost of repairs in marine conditions.

Agreed Value Protects Against Saltwater Depreciation

Agreed Value coverage becomes non-negotiable for saltwater boats because saltwater damage can total a vessel that still has years of life left in freshwater use. A $50,000 cruiser experiencing gel coat failure, engine corrosion, and rigging damage from salt spray loses value under Actual Cash Value, but Agreed Value protects you from that financial hit. You lock in your boat’s worth before a total loss occurs, which eliminates depreciation disputes when saltwater damage becomes catastrophic.

Environmental Liability and Spill Coverage

Environmental liability matters more in Washington than most states because the Department of Ecology enforces strict spill regulations. Fuel spill coverage isn’t optional when one bilge pump failure or docking accident can trigger regulatory action. Your policy must include pollution and fuel spill endorsements as genuine protections rather than optional extras.

Security and Theft Prevention in Coastal Areas

Theft and vandalism in coastal marinas demand specific security endorsements that inland policies rarely consider necessary. Coastal theft rings target electronics, outboards, and gear at higher rates than inland lakes, making GPS trackers and alarm systems more than conveniences. You need coverage that accounts for the specific hazards your boat actually faces in saltwater conditions rather than fitting into a one-size template designed for calmer waters.

Seasonal Storage and Winter Coverage Flexibility

Winter weather patterns in the Pacific Northwest create seasonal storage challenges that affect your coverage timeline and costs. The boating season spans roughly eight to nine months, meaning your policy needs flexibility for lay-up periods when your boat sits in dry storage or covered slips. Some insurers adjust premiums during winter suspensions if you formally notify them that your boat won’t operate. Puget Sound’s combination of strong currents, busy shipping lanes, and unpredictable weather makes November through March genuinely dangerous for recreational boating. Towing and emergency assistance endorsements become essential when Puget Sound conditions strand you miles from help, with salvage costs regularly exceeding $2,000 for multi-hour operations. These endorsements transform what could become a financial disaster into a manageable claim. Understanding these specific saltwater exposures sets the stage for selecting the right policy-which means comparing what different providers actually offer and how their coverage options align with your boat and your plans for Puget Sound.

Picking the Right Policy for Your Saltwater Boat

Establish Your Boat’s True Market Value

Start with your boat’s actual market value, not what you paid for it five years ago. A free boat valuation tool analyzes comparable sales and current listings to establish low, medium, and high market values based on 2026 data, which typically falls within 5-10% of actual selling prices. Once you know your boat’s real value, you can decide whether Agreed Value or Actual Cash Value makes sense for your situation. Agreed Value locks in your boat’s worth before a total loss, eliminating depreciation disputes when saltwater damage strikes. For a $50,000 cruiser, this difference matters enormously because saltwater damage depreciates vessels faster than freshwater exposure ever would.

Match Coverage to Your Actual Usage Patterns

Document exactly how you use your boat because usage patterns directly affect your premium and what coverage you actually need. If you cruise Canadian waters regularly, your policy must cover cross-border navigation and meet CAD 100,000 liability minimums. If you fish offshore versus day cruise in Puget Sound, your exposure differs dramatically. Boaters who navigate coastal waters 100 nautical miles offshore need extended navigation endorsements that inland operators never consider. Your storage method also shapes your premium significantly-wet slip moorage in a busy marina carries different theft and weather risks than home storage on a trailer. Once you understand your boat and how you actually operate it, gather your Hull Identification Number, engine specifications, purchase price, and planned cruising area before requesting quotes from multiple providers.

Compare Coverage Details, Not Just Premiums

Comparing quotes requires reading past the premium number to examine what each insurer actually covers. A $600 annual policy might exclude saltwater corrosion while a $750 policy includes zinc anode protection and anti-corrosion endorsements that prevent expensive repairs. Verify whether towing and emergency assistance limits reach $1,500 per occurrence because Puget Sound salvage operations routinely cost $2,000 or more for multi-hour assistance. Check environmental liability limits carefully-Washington’s Department of Ecology can fine up to $10,000 per day for fuel spills, so your pollution coverage must reflect that real regulatory threat. Ask specifically about deductibles for striking submerged objects because these often sit separate from your standard collision deductible and can range from $250 to $1,500. Personal effects coverage should reach at least $10,000 if you store expensive gear aboard. Medical payments coverage between $10,000 and $25,000 per person protects family and guests adequately for Puget Sound conditions.

Stack Discounts to Reduce Your Annual Premium

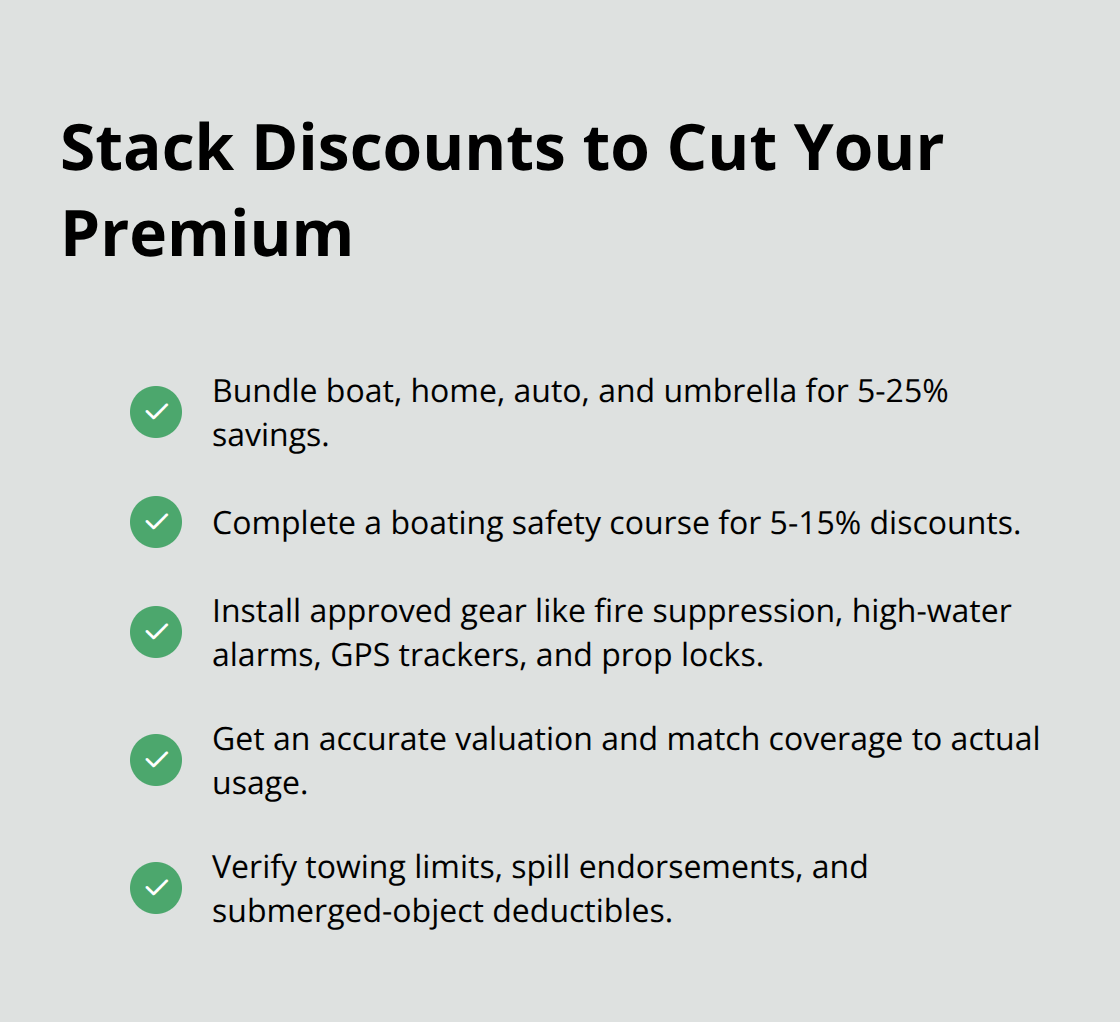

Bundling your boat insurance with homeowners, auto, and umbrella policies typically saves 5-25% across your entire coverage package, making this your most direct premium reduction opportunity. A boating safety course completion yields additional 5-15% discounts with most carriers. Installing approved safety gear like fire suppression systems, high-water alarms, GPS trackers, and prop locks qualifies you for further discounts that accumulate quickly.

These practical steps-securing accurate valuation, matching coverage to your actual usage, and stacking available discounts-transform boat insurance from an expense into legitimate financial protection that reflects your real exposure on Puget Sound waters. As an independent agency representing multiple top carriers, H&K Insurance Agency compares rates and customizes packages so you get the right protection at competitive prices without overpaying for coverage you don’t need.

Final Thoughts

Saltwater boat insurance protects your vessel and finances against the specific hazards of Puget Sound and Washington’s coastal waters. Agreed Value protection, environmental liability endorsements, and towing assistance address real threats like saltwater corrosion, regulatory fines up to $10,000 per day, and salvage costs exceeding $2,000. Standard inland policies leave you exposed to exposures that Northwest boaters face daily.

Gather your boat’s Hull Identification Number, engine specifications, and planned cruising area, then request quotes from multiple providers who understand Northwest conditions. Compare what each policy actually covers rather than focusing solely on the premium, and verify that environmental liability, towing limits, and deductibles for submerged objects align with your real exposure. Stack available discounts through boating safety courses and bundling to reduce your annual cost by 5-25%.

Contact H&K Insurance Agency to discuss your saltwater boat insurance needs with agents who know Puget Sound conditions firsthand. We represent multiple top carriers and customize packages so you get the right protection at competitive prices without overpaying for coverage you don’t need.