Boat Insurance Claims Process: Step-by-Step to Fast Settlements

Boat damage happens fast, but your insurance claim doesn’t have to move slowly. We at H&K Insurance Agency know that understanding the boat insurance claims process makes all the difference between a quick settlement and months of frustration.

This guide walks you through each step, from reviewing your policy to receiving your payout. You’ll learn exactly what insurers need and how to provide it efficiently.

Know Your Coverage Before You File

Your boat insurance policy isn’t one-size-fits-all, and most boat owners fail to understand what they actually own until damage strikes. We see this repeatedly: policyholders uncover gaps in coverage weeks after filing a claim, which delays settlements and leaves them vulnerable. Start now, not after an incident. Open your policy documents and identify the two main sections that matter most. Physical damage coverage protects your hull, engines, sails, and onboard equipment from specific perils like wind, collision, theft, and fire. Liability coverage handles your legal responsibility if you damage someone else’s property or injure someone. The difference between these two sections determines what gets paid and what doesn’t.

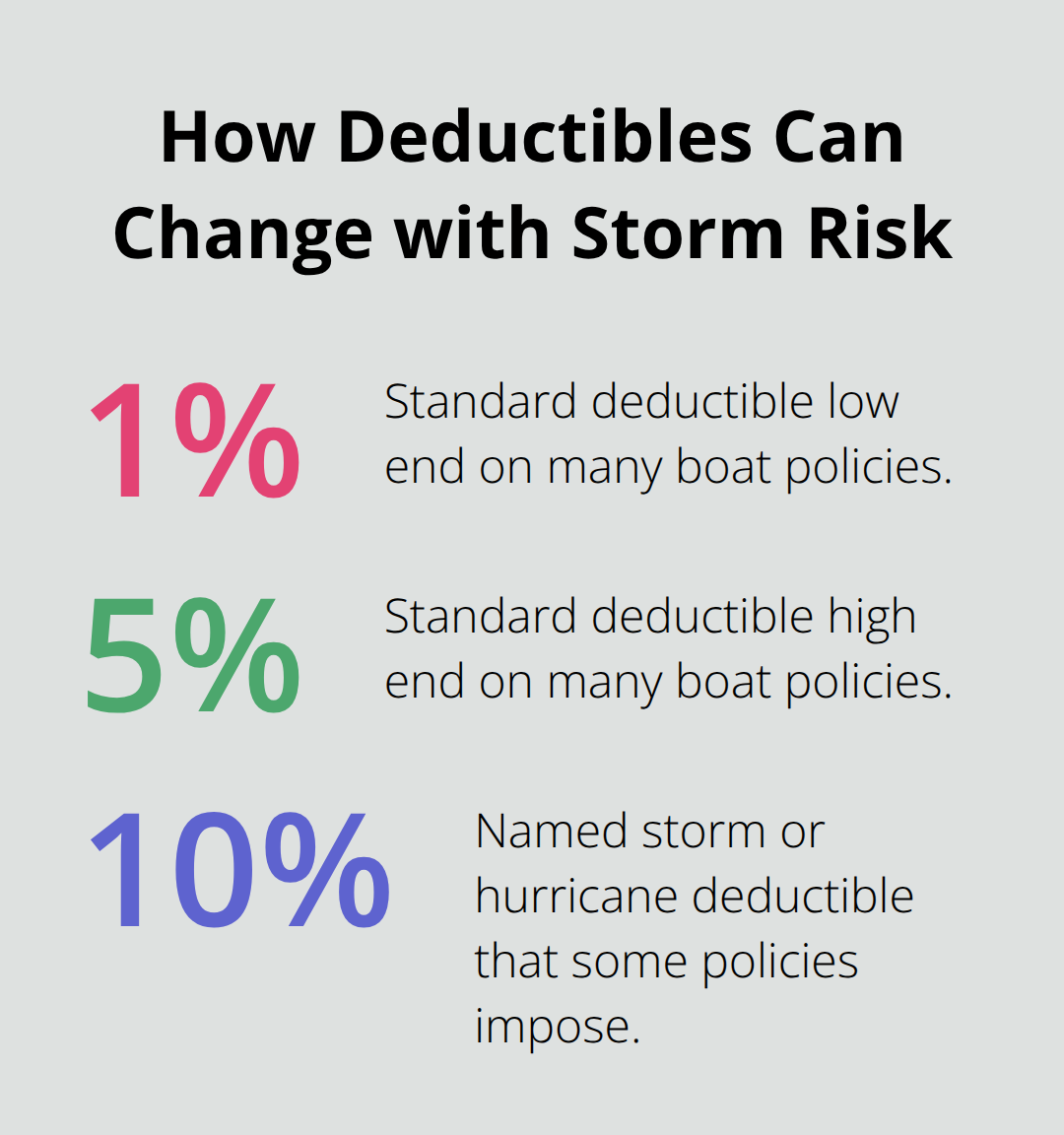

Your policy also specifies coverage limits-the maximum amount the insurer will pay-and deductibles, which are your out-of-pocket costs per claim. A typical boat insurance deductible ranges from 1% to 5% of your boat’s insured value, meaning a $200,000 boat might carry a $2,000 to $10,000 deductible. Higher deductibles lower your premium but increase what you pay when you file a claim.

What Your Policy Actually Covers

Read the exclusions section carefully, because what’s excluded matters more than what’s included when you need help. Weather-related damage tops the list of boat insurance claims in Florida and nationwide, but some policies impose higher deductibles for named storms or hurricanes-sometimes 10% of the boat’s value instead of the standard 1–5%.

Collision with docks, submerged objects, or other boats falls under most policies, but grounding due to tides and hitting rocks require active hull coverage. Theft and vandalism typically fall under comprehensive coverage, though personal property like electronics and fishing gear may have separate limits.

One critical gap: homeowners insurance does not cover boats, period. If you rely on your home policy for boat protection, you have zero coverage. Emergency towing and assistance coverage reimburses towing costs, fuel delivery, and emergency labor-essential if your engine fails offshore. Medical payments coverage covers injuries to people aboard, but you must verify per-person limits and whether it applies during boarding or when being towed.

Organize Your Documents Now

When you file a claim, speed depends on how quickly you provide what the insurer needs. Collect your policy documents, vessel registration, proof of ownership, and your insurance agent’s contact information into one folder-digital or physical. If you’ve had a marine survey completed, locate that report and any maintenance records showing regular upkeep, because insurers use these to verify your boat’s condition and value. Keep receipts for recent upgrades or improvements, because these affect settlement amounts if the boat sustains damage.

Store copies in multiple places: one at home, one in a waterproof folder on the boat, and one digitally in cloud storage. When you file a claim, you’ll also need the other party’s insurance information if a collision occurred, or police reports if theft happened. Having these organized cuts claim processing time significantly. Contact your insurance agent to review your specific coverage limits and exclusions, especially if you boat in different regions or plan to charter.

With your policy understood and your documents organized, you’re ready to act fast when damage strikes-and the next section shows you exactly what to do in those critical first hours.

What to Do in the First 24 Hours After Damage

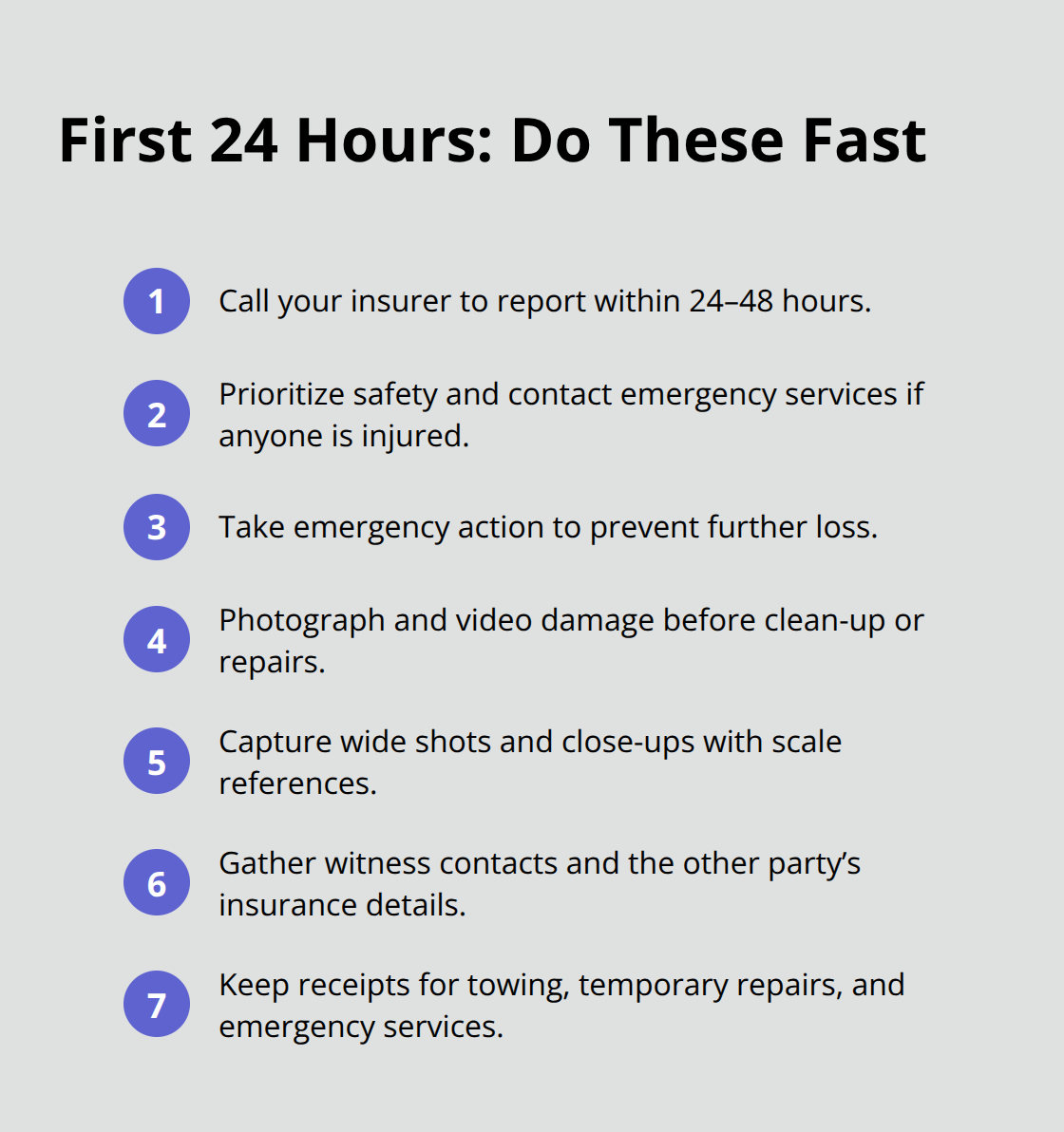

The hours immediately after boat damage determine how smoothly your claim moves forward. Most insurers expect you to report within 24–48 hours, and delaying that call creates unnecessary friction. File your claim before you do anything else except address immediate safety concerns. If anyone is injured, contact emergency services first. If fuel is leaking or the boat is at risk of sinking, take emergency action to prevent further loss. Then pick up the phone and call your insurance company.

Many carriers offer 24/7 emergency claims support, so time of day doesn’t matter.

Report the Incident Immediately

When you call, have your policy number ready and provide a brief, factual account of what happened: the date, time, location, weather conditions, and what the boat struck or what happened to it. Do not speculate about fault or cause. Stick to observable facts. The insurer will assign a claims specialist or adjuster immediately, and that person becomes your point of contact for everything that follows. Ask for their direct number and email, because you’ll need to coordinate inspections and provide documentation through them.

Document the Damage Thoroughly

While waiting for the adjuster to contact you, photograph and video the damage from multiple angles. Take wide shots showing the overall condition and close-ups of specific damage areas. Include reference objects in photos so the scale of damage is clear. Photograph the boat’s condition before you clean up debris or attempt repairs, because insurers need to see the damage exactly as it occurred. If weather caused the damage, photograph the surrounding area and any weather-related debris. If another boat or object caused the collision, photograph the other vessel or object if possible and obtain contact information from witnesses.

Preserve Evidence and Prevent Further Loss

For theft or vandalism, file a police report immediately and obtain the report number, because your insurer will require it. Do not touch or move damaged equipment unless absolutely necessary to prevent additional harm. Take action only to stop further deterioration: pump bilges if the boat is taking on water, cover exposed areas with tarps, or arrange emergency towing to a safe location. Keep receipts for any emergency services, temporary repairs, or towing costs, because these become part of your claim. The adjuster will want to see your documentation and understand what you did to prevent additional loss. Insurers expect policyholders to act reasonably to protect their property, and failing to do so can create coverage disputes.

Your proactive steps during these first 24 hours make the difference between a claim that settles in weeks and one that stalls for months. The next section shows you how to work with the adjuster and provide the detailed information that accelerates your settlement.

Working with Your Adjuster to Accelerate Settlement

Once you report your claim, an adjuster or marine claims specialist will contact you within 24 hours to schedule an inspection. This person controls the timeline and determines what gets paid, so treat this relationship as a partnership, not an adversarial process. When the adjuster calls, have your documentation ready: photos, videos, receipts for emergency repairs, maintenance records, and a written account of exactly what happened. Write down the adjuster’s name, direct number, and email immediately.

Provide Detailed Information to Speed Up Investigation

Provide a detailed chronological narrative of the incident-the weather conditions, what you were doing when damage occurred, who was present, and what you observed. Vague accounts slow investigations because adjusters must follow up with additional questions, extending the process by days or weeks. Specific details resolve uncertainties faster. If another boat was involved, provide names and contact information for witnesses. If theft occurred, include your police report number. The adjuster will also assign a marine surveyor or estimator to inspect the boat and assess damage.

Cooperate Fully During the Inspection Process

Cooperate fully with the inspection: be present if possible, answer questions directly, and provide any documentation the surveyor requests on the spot. Disagreements about damage scope or repair costs often arise during this phase, so document any concerns in writing immediately after the inspection and send them to your adjuster via email. This creates a record that protects you if the initial estimate undervalues the damage.

Review the Settlement Offer Carefully

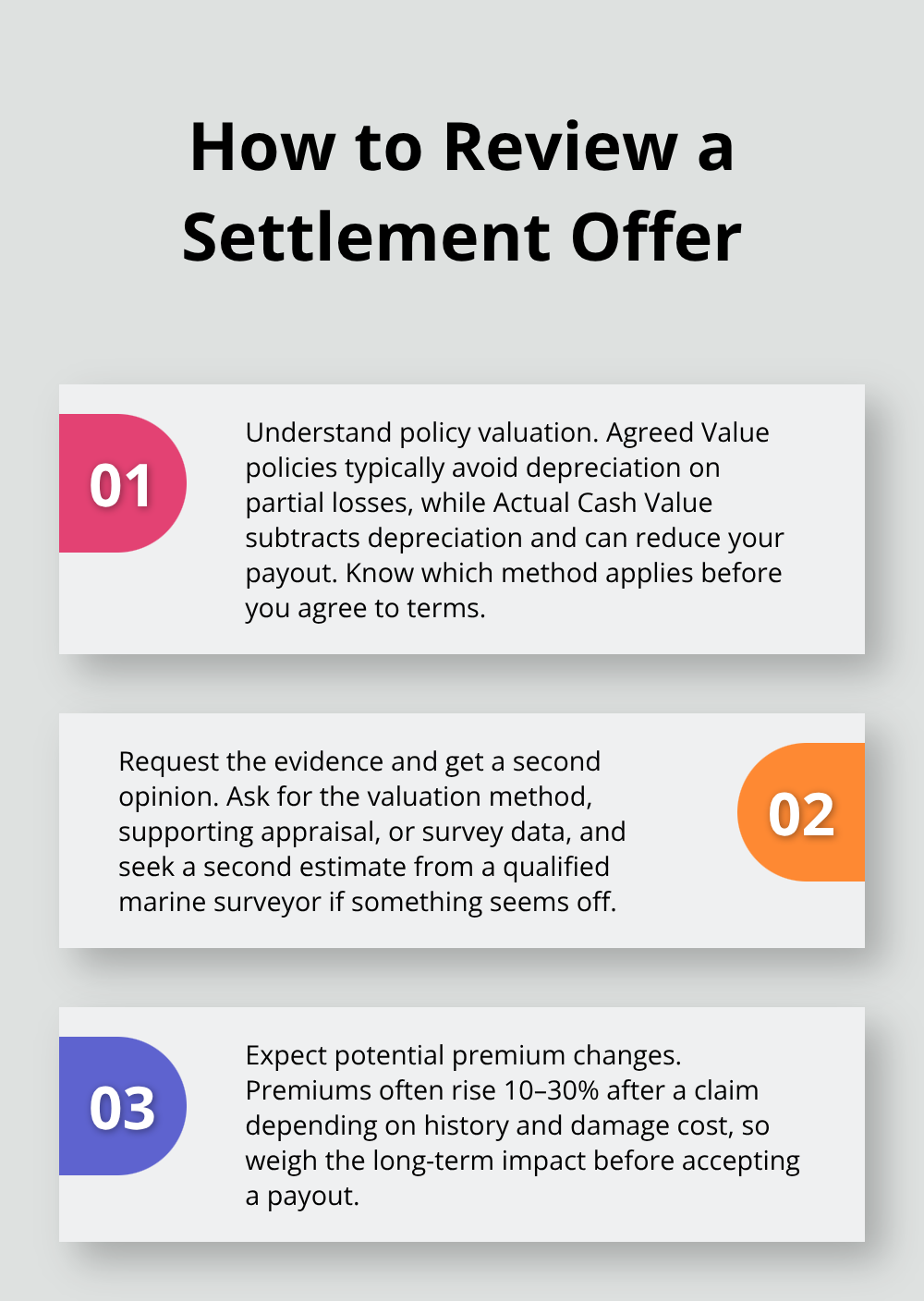

Settlement amounts depend entirely on the repair estimate, and this is where many boat owners lose money. The adjuster will review repair costs with you and explain what your deductible covers and what the insurer will pay. If repairs aren’t practical, the boat may be declared a total loss, and the payout depends on your coverage type-Agreed Value policies typically pay replacement cost for partial losses without depreciation, while Actual Cash Value policies subtract depreciation and reduce your payout. Ask the adjuster to explain the valuation method used and request the appraisal or survey data supporting the value calculation. If you disagree with the settlement offer, say so immediately and request a second estimate from another qualified marine surveyor. Premiums typically rise 10–30% after a claim depending on your prior record and damage cost, so understanding the settlement amount before accepting it matters significantly.

Monitor Repairs and Stay Informed

Once you accept the settlement and repairs begin, request weekly updates on progress and estimated completion dates. Most repair shops provide status updates based on parts availability and labor schedules, so staying informed prevents surprises. If you choose not to repair the boat, the insurer pays the estimate amount minus your deductible, and you can use those funds as you see fit. Throughout this process, ask questions whenever something is unclear-adjusters expect this and view it as normal. The goal is a settlement that fairly reflects your loss and gets your boat back in operation as quickly as possible.

Final Thoughts

The boat insurance claims process moves fastest when you act decisively and provide complete information upfront. Report your claim within 24 hours, document everything with photos and videos, and gather your policy documents before the adjuster calls. During the inspection phase, be present, answer questions directly, and request clarification on any settlement offer that seems low. Review repair estimates carefully and don’t accept a payout without understanding how your insurer calculated the value.

After your claim settles and repairs begin, stay engaged with weekly progress updates and maintain communication with your repair shop. Expect your premium to rise 10–30% depending on your claims history and damage cost, but this is manageable if you’ve secured the right coverage from the start. The entire process typically takes 4–8 weeks from initial report to final payment, though complex claims involving multiple parties or total losses may extend longer.

Prevent future claims by maintaining your boat regularly and documenting all service work with receipts. Store your policy documents, vessel registration, and maintenance records in multiple locations so they’re accessible when you need them. We at H&K Insurance Agency represent multiple carriers and can customize a boat insurance package that matches your specific needs and budget-contact us today to review your current coverage or obtain a personalized quote that protects your investment and gives you peace of mind on the water.