Personal Liability Coverage: Safeguarding Your Finances and Assets

One accident or injury on your property could lead to a lawsuit that threatens your savings and assets. Personal liability coverage protects you from these financial disasters by covering legal fees, medical expenses, and court judgments.

At H&K Insurance Agency, we’ve seen how quickly liability claims can drain a family’s finances. That’s why understanding your coverage options is the first step toward real financial security.

Why Personal Liability Coverage Protects Your Wealth

A single incident can cost you tens of thousands of dollars in legal fees and settlements. If someone trips on your porch and breaks their leg, or your dog bites a neighbor, you face medical bills that reach $50,000 or more, plus attorney fees that climb to $10,000–$25,000. Personal liability coverage pays these costs before they drain your savings. Without it, you remain personally responsible for damages up to the full judgment amount-which means creditors can pursue your bank accounts, wages, and assets.

Coverage Limits That Match Your Assets

Most standard homeowners policies include liability coverage starting at $100,000, but this limit often falls short for households with meaningful wealth. Try to carry a limit that matches or exceeds your net worth, which means many families need $300,000 to $500,000 in coverage. If your assets exceed $500,000, an umbrella policy extends protection beyond your homeowners or auto policy at a relatively low cost-often just $150–$300 annually for $1 million in additional coverage.

The real advantage here is that personal liability coverage ranks as typically the least expensive part of your home policy. Increasing your limits from $100,000 to $300,000 usually adds only $15–$30 to your annual premium. This means you can significantly strengthen your financial protection for almost nothing.

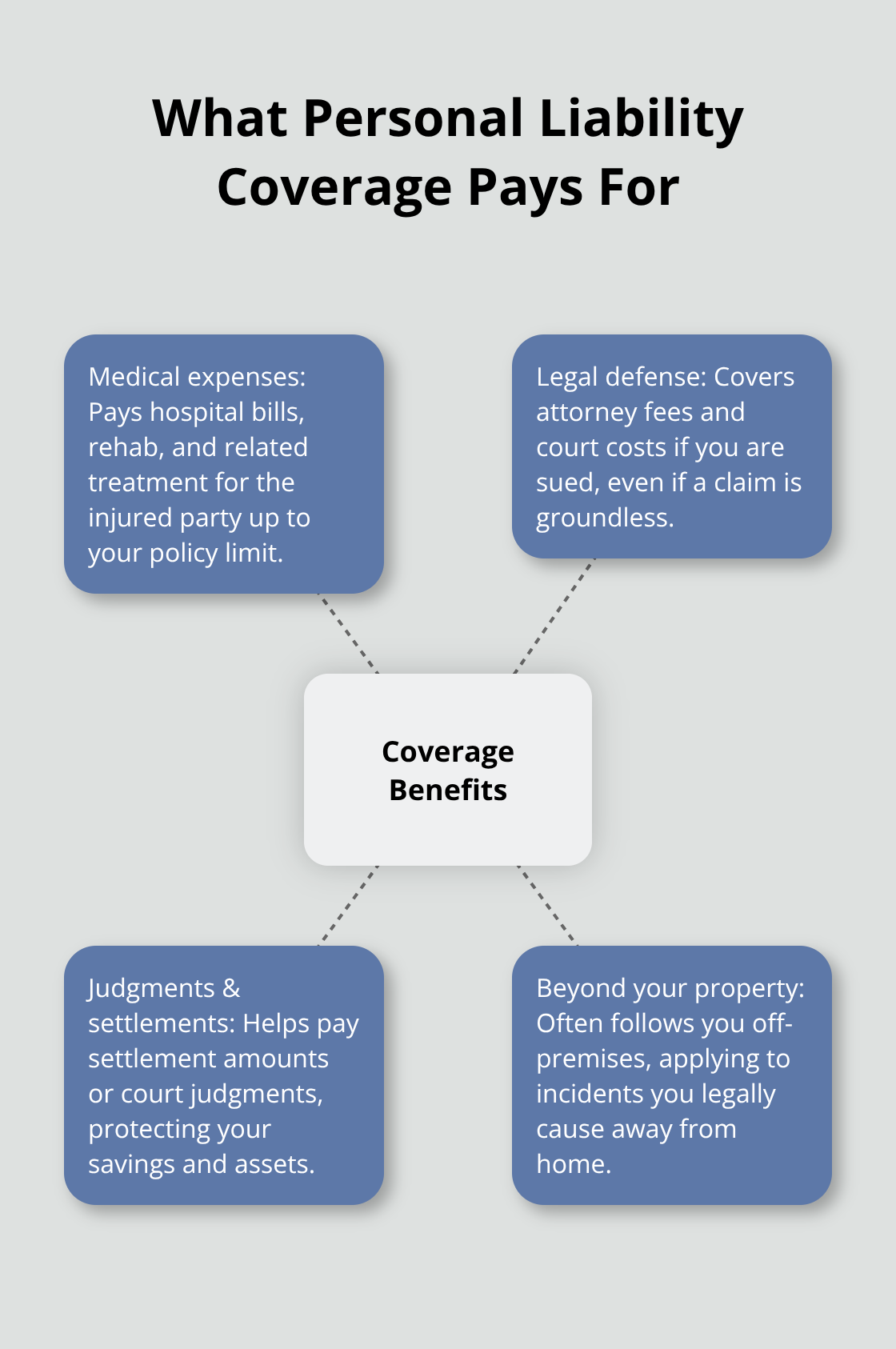

What Your Coverage Actually Pays For

Medical expenses and legal defense costs represent the two biggest financial threats after an accident on your property or one you cause elsewhere. Your liability coverage pays hospital bills, rehabilitation costs, and lost wages for the injured person-up to your policy limit. It also covers your legal defense if you’re sued, including attorney fees, court costs, and settlement amounts if you lose.

This protection applies whether the accident happens at your home, at a neighbor’s property, or even at a public venue where you’re found legally responsible. Dog bites represent one of the most common liability claims, with California reporting 2,417 claims in 2024 averaging $86,229 per claim.

High-Risk Properties Demand Higher Protection

Pools and trampolines dramatically increase your liability risk, which is why properties with these attractive nuisances should carry higher limits. Installing a fenced pool with a locking gate and securing trampolines with safety nets reduces claims frequency and may lower your premiums. However, coverage limits remain your primary defense against catastrophic costs-and understanding which scenarios pose the greatest risk helps you prepare for what comes next.

Types of Personal Liability Coverage

Homeowners Insurance Liability

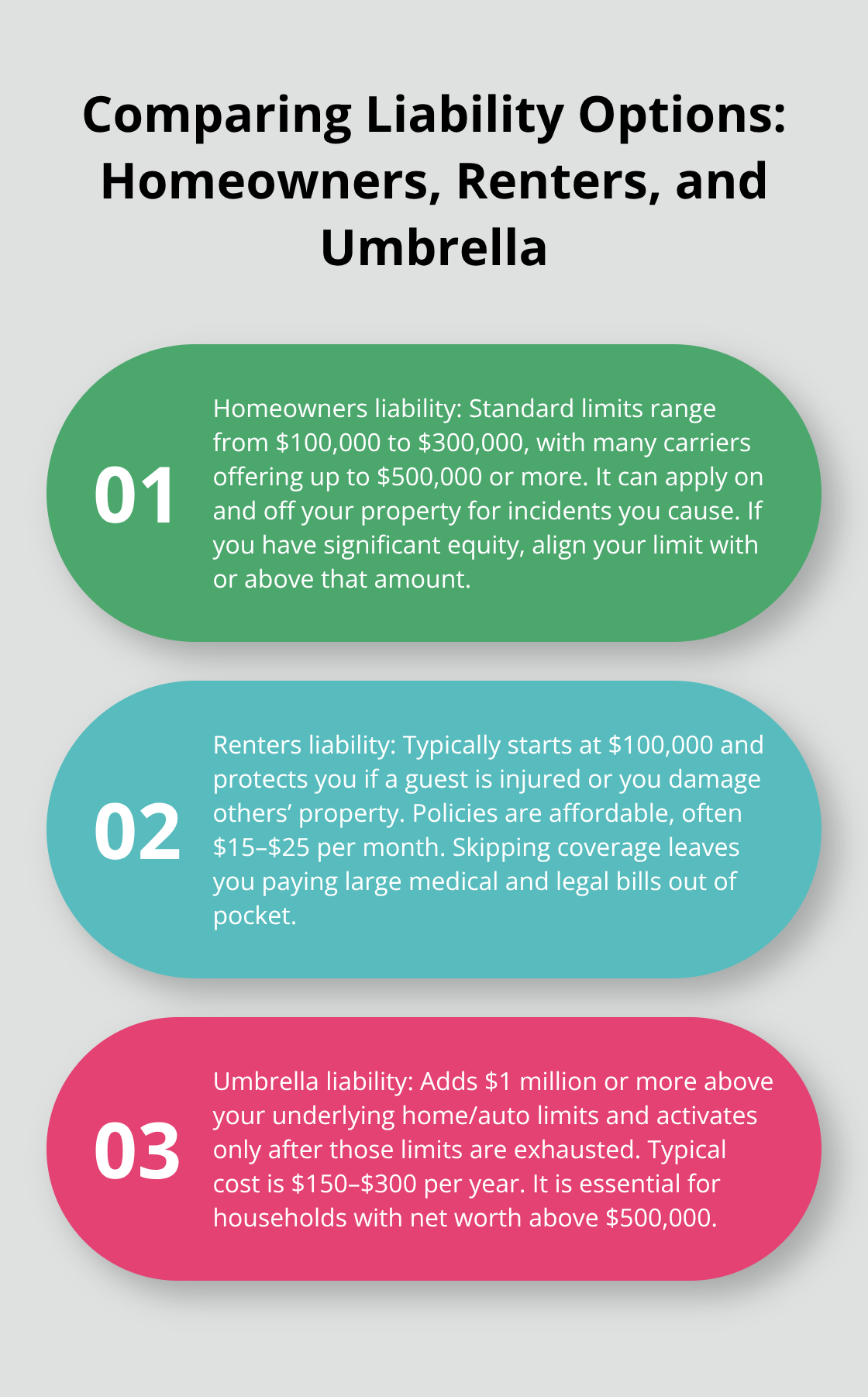

Your homeowners policy provides the foundation for personal liability protection, but the coverage varies significantly depending on your property type and carrier. Standard homeowners insurance includes personal liability limits of $100,000 to $300,000, though many carriers now offer higher limits up to $500,000 or more. This coverage applies to incidents on your property and, in many cases, to accidents you cause away from home-like accidentally breaking a neighbor’s window or injuring someone at a public event. Most homeowners carry far less protection than their actual assets warrant, which exposes them to serious financial risk. If you own your home outright or have significant equity, your liability limit should match or exceed that equity to prevent creditors from pursuing your assets after a judgment.

Renters Insurance Liability

Renters face different circumstances since they don’t own the building itself, yet they remain fully liable for injuries or damage they cause. A renter’s policy includes personal liability coverage starting at $100,000, which protects you if a guest is injured in your apartment or if you accidentally damage someone else’s property. Many renters skip liability coverage altogether, which is a dangerous mistake-a single slip-and-fall accident results in a $50,000 medical bill plus $15,000 in legal fees that you’d pay personally. Renters insurance costs between $15 and $25 monthly, making liability protection almost negligible in price. This low cost means you gain substantial financial protection for less than the price of a coffee subscription.

Umbrella Policies Extend Your Protection

Umbrella policies operate as a separate layer of protection that sits above your homeowners or auto policy limits. These policies activate only after your underlying coverage is exhausted, meaning they don’t replace your standard liability protection-they extend it. A $1 million umbrella policy typically costs $150 to $300 annually, making it the most cost-effective way to protect substantial assets. If your net worth exceeds $500,000, an umbrella policy becomes essential because standard homeowners coverage maxes out far below what you need.

Properties with high-risk features like pools or trampolines become stronger candidates for umbrella coverage because these features generate more frequent and larger claims. Some carriers impose requirements before issuing umbrella policies, such as maintaining minimum underlying liability limits of $300,000 on your homeowners policy, so coordinate with your agent before applying. The umbrella policy also covers liability gaps that homeowners policies don’t address, including certain rental property incidents or professional liability scenarios depending on your policy wording.

Why Asset Protection Demands Umbrella Coverage

Choosing not to add umbrella coverage when you have meaningful assets exposes you to catastrophic financial loss. A single major claim could wipe out decades of savings, leaving you vulnerable to wage garnishment and asset seizure. The combination of low cost and substantial protection makes umbrella policies the most rational financial decision for anyone with net worth above $500,000. Once you understand your current liability limits and identify gaps in your protection, the next step involves evaluating which specific scenarios pose the greatest risk to your household.

Common Scenarios Where Personal Liability Claims Strike

Accidents on Your Property Create Immediate Exposure

A guest slips on your wet kitchen tile and fractures their wrist-hospital bills hit $47,000, and they hire an attorney. Your teenager kicks a soccer ball through a neighbor’s window, cracking the glass and damaging interior shelving worth $3,200. Your dog lunges at a mail carrier, inflicting a bite that requires emergency room treatment and plastic surgery. These aren’t hypothetical scenarios. They happen constantly, and most homeowners and renters drastically underestimate both the frequency and cost of liability claims.

A slip-and-fall accident on residential property generates average settlements ranging from $30,000 to $60,000, though cases involving serious injuries can reach $500,000 to $2,000,000 or more. Add legal defense costs of $10,000 to $25,000, and you face a significant event that exhausts a standard $100,000 liability limit immediately. Dog bite claims average $86,229 in California alone, with some severe cases exceeding $200,000 when facial reconstruction or permanent disability results.

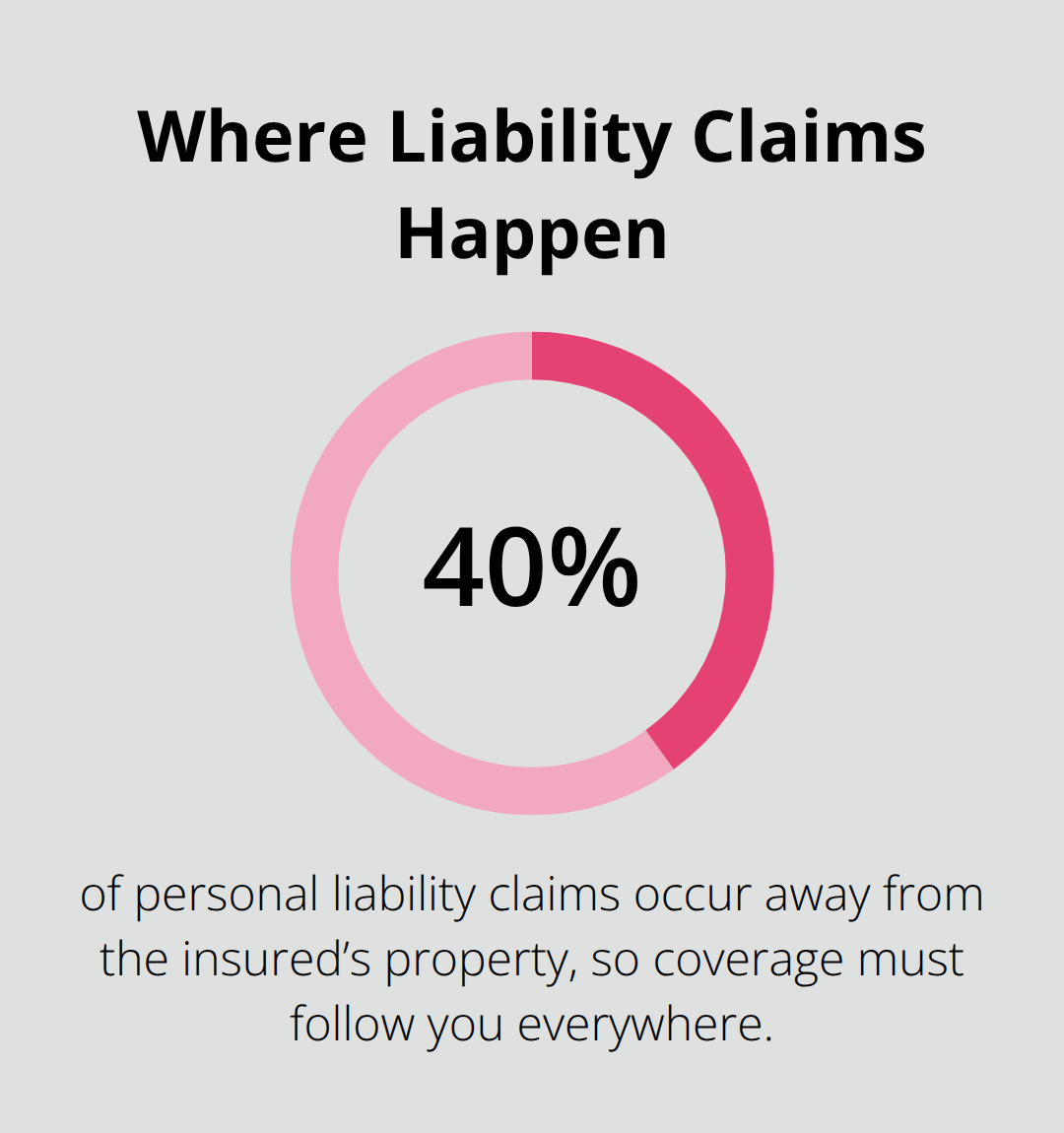

Off-Property Liability Catches Most People Off Guard

The second major liability exposure occurs away from your property, in situations where most people don’t even realize they’re at risk. If you accidentally injure someone at a public event, hit a pedestrian with a golf ball at the course, or cause property damage at someone else’s home, your personal liability coverage extends to cover these incidents. A golf ball strike that injures someone’s eye can result in $50,000 in medical bills plus vision loss claims pushing total damages beyond $100,000.

Renters face identical exposure despite not owning property-a renter who damages a neighbor’s apartment during a party remains fully liable for repairs, which can easily exceed $15,000 to $30,000 for water damage or fire damage to adjacent units. Approximately 40 percent of liability claims originate from incidents away from the insured’s property, meaning your coverage must follow you everywhere.

Why Your Coverage Limits Matter More Than You Think

If you own significant assets or earn a solid income, carrying only $100,000 in liability coverage leaves you vulnerable to wage garnishment for years after a judgment. We at H&K Insurance Agency recommend carrying at minimum $300,000 in liability coverage if you own your home, because the gap between what accidents actually cost and what most people carry creates dangerous financial exposure.

Umbrella policies activate only after your underlying homeowners or renters coverage exhausts, so a $1 million umbrella doesn’t increase your out-of-pocket costs for smaller claims-it simply protects your assets when a major claim exceeds your base limits. This layered approach (homeowners liability plus umbrella coverage) provides the comprehensive protection that substantial net worth demands.

Final Thoughts

Personal liability coverage protects your financial future from accidents that strike without warning. A single incident on your property or one you cause elsewhere can generate medical bills exceeding $50,000 plus legal fees reaching $25,000 or more, and without adequate coverage, you face wage garnishment and asset seizure that could take years to recover from. Start by reviewing your current homeowners or renters policy to identify your existing liability limits and compare this amount against your net worth.

The math strongly favors increasing your coverage because moving from $100,000 to $300,000 in liability protection typically costs only $15 to $30 annually. An umbrella policy adding $1 million in additional protection runs $150 to $300 per year-amounts that pale in comparison to the financial devastation a major claim creates. Most standard policies include $100,000 in coverage, which falls dangerously short if you own meaningful assets or earn a solid income.

Contact H&K Insurance Agency to review your current coverage and identify the gaps that could cost you everything. Our team compares rates across multiple carriers to find you the right protection at competitive prices, whether you need to increase your homeowners liability limits, add renters coverage, or layer in an umbrella policy.