Multifamily Homeowners Policy: Insuring More Units With Confidence

Owning multiple residential units comes with unique insurance challenges that standard homeowners policies simply don’t address. A multifamily homeowners policy fills that gap by providing coverage tailored to landlords and property owners managing several units at once.

At H&K Insurance Agency, we help property owners understand what protection they actually need. This guide walks you through the coverage options, how to compare them, and how to build a policy that matches your specific situation.

What Multifamily Coverage Actually Protects

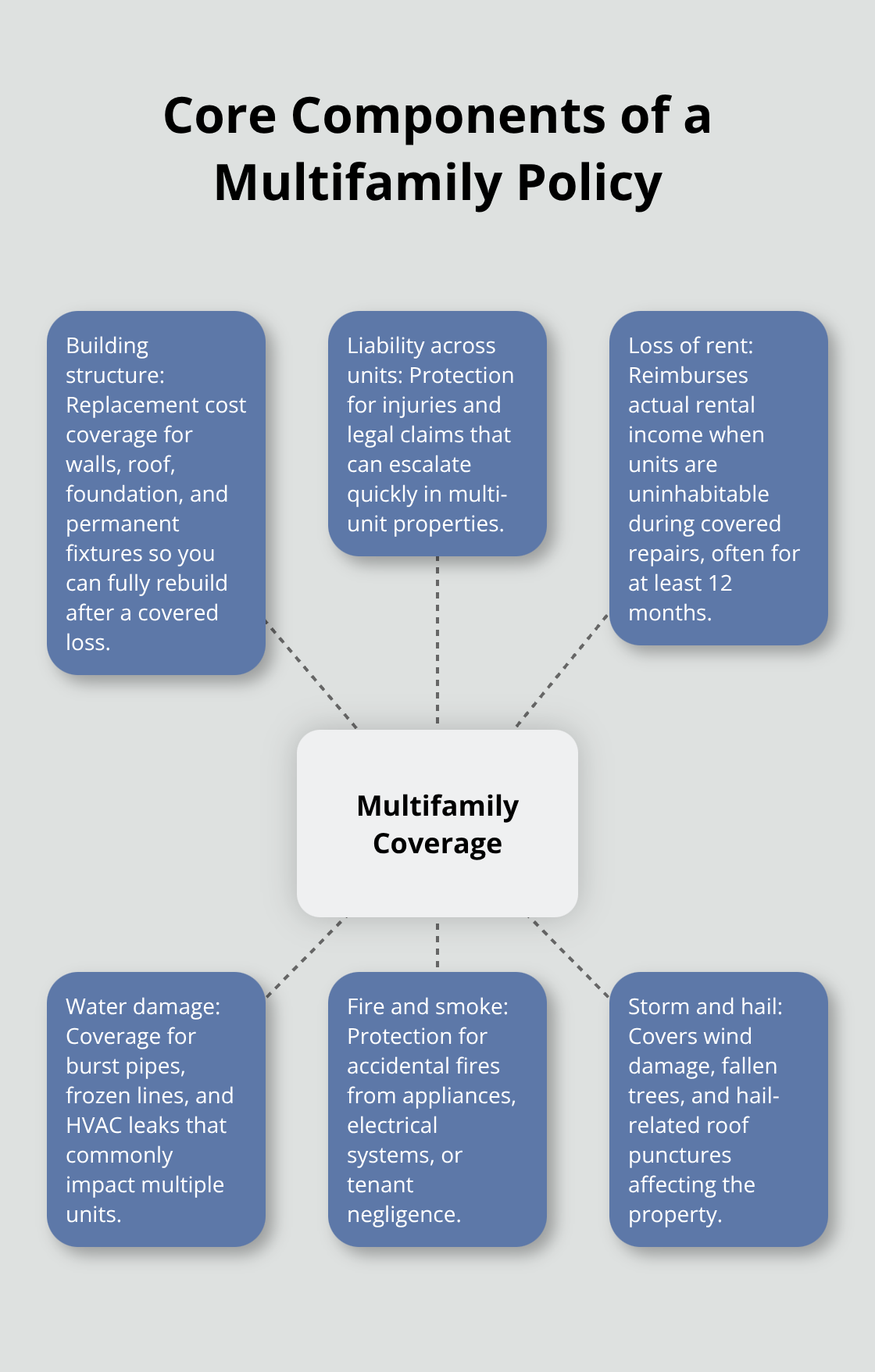

A multifamily homeowners policy serves one specific purpose: it protects rental income and property when you own multiple units. Standard homeowners policies exclude rental activity entirely, which means the moment you rent out a unit, your coverage vanishes. Multifamily policies flip that logic. They cover the building structure, liability across all units, and the rental income you lose when a property becomes uninhabitable due to a covered event. Core coverage typically includes replacement cost for the building itself (never actual cash value, which pays far less), liability limits ranging from $300,000 to $2,000,000 depending on your portfolio size, and loss of rent protection for at least 12 months.

For a 200-unit portfolio in Ohio’s tertiary markets, real-world costs run about $510 per unit annually, translating to roughly $44,000 per year with a $10,000 deductible. This isn’t cheap, but it’s essential. The policy also covers water damage from burst pipes and HVAC leaks, fire and smoke damage, storm and hail damage including fallen trees, and legal liability if a tenant or visitor gets injured on your property. Vacancy periods and restoration work are insurable too, which matters when you’re between tenants or mid-renovation.

Why Standard Homeowners Policies Fail Landlords

Standard homeowners policies carry explicit exclusions for rental activity. Insurers assume you live in the home, so they exclude fire caused by tenant negligence, liability claims from tenants, and loss of rental income entirely. If you’re renting out even one unit and a pipe bursts, your standard policy won’t cover the lost rent while repairs happen. Multifamily policies eliminate this gap by treating rental exposure as the primary risk, not an afterthought. They also account for higher replacement costs in multi-unit buildings, which have multiple kitchens, bathrooms, and mechanical systems that drive up repair expenses. A duplex isn’t just twice the risk of a single-family home; it’s exponentially more complex from an insurance standpoint.

Building Protection and Liability Across Units

The building structure coverage in multifamily policies protects against reconstruction costs after fire, wind, hail, or water damage. Common areas like hallways, laundry rooms, and parking lots are included, not optional add-ons. Liability coverage is where multifamily policies truly diverge from standard homeowners coverage. One tenant slip-and-fall claim can exceed $100,000 in medical costs and legal fees. With multiple units, your exposure multiplies. That’s why multifamily policies emphasize strong liability limits and why you should try at least $1 million in coverage for portfolios above five units. For larger portfolios, a commercial umbrella policy extends liability protection beyond standard limits and becomes essential. Loss of rent coverage reimburses you if the property becomes uninhabitable during repairs, protecting cash flow during the exact period when you can’t afford to lose income.

How Loss of Rent Coverage Protects Your Cash Flow

Loss of rent coverage represents the most valuable protection in a multifamily policy. This coverage reimburses you when tenants can’t occupy units due to a covered loss-whether that’s fire damage, water intrusion, or storm destruction. Without this protection, you absorb the full financial hit while contractors repair the damage. A three-month repair period on a 10-unit building with $1,000 monthly rent per unit means $30,000 in lost income. Loss of rent coverage eliminates that exposure. Most policies cover a minimum of 12 months of lost rent, though you can adjust this based on your market and typical repair timelines. This coverage is the difference between a manageable setback and financial strain.

Choosing the Right Coverage Limits for Your Portfolio

Coverage limits should match your actual exposure, not just the cheapest option available. A 50-unit portfolio needs different protection than a five-unit duplex. Liability limits of $300,000 work for small portfolios, but $1 million becomes standard as you add units. For portfolios exceeding 50 units, consider whether $2 million in liability coverage makes sense given your tenant mix and property location. High-crime areas and older buildings typically warrant higher limits. The same logic applies to loss of rent coverage-longer protection periods cost more but provide better security during extended repairs. Work with an independent agent who represents multiple carriers to compare how different insurers price these limits and what they actually cover under each scenario.

What Your Multifamily Policy Actually Covers

Building Structure Protection at Replacement Cost

Building structure protection forms the foundation of any multifamily policy, but most landlords underestimate what the coverage includes. Your policy covers the dwelling itself-walls, roof, foundation, permanent fixtures-at replacement cost, meaning the insurer pays what it actually costs to rebuild, not some depreciated figure from 20 years ago. Common areas receive the same protection: hallways, stairwells, laundry facilities, parking lots, and trash enclosures all fall under building coverage. Water damage from burst pipes, frozen lines, and HVAC leaks is included. Fire and smoke damage coverage applies to accidental fires caused by appliances, electrical systems, or tenant negligence. Storm and hail protection covers wind damage, fallen trees, and roof punctures from hail.

What Tenants Must Cover Themselves

The critical detail most landlords miss: these coverages apply to the structure you own, not tenant belongings. Tenants must carry renters insurance for their personal property, and smart leases require this in writing. This distinction protects both parties-your policy handles the building, theirs handles their possessions. For a 200-unit Ohio portfolio paying $510 per unit annually, the building structure coverage represents roughly 40 percent of that premium, reflecting the replacement cost exposure in older, remodeled Class B and C properties.

Liability Coverage Multiplies With Every Unit You Add

Liability coverage across multiple units demands serious attention because your exposure multiplies with every tenant you add. One slip-and-fall injury can generate $100,000 in medical costs and legal defense fees within weeks. Standard policies offer $300,000 to $2,000,000 in liability limits, but the right choice depends on your portfolio size and risk profile. Five-unit buildings can operate safely at $300,000, but ten units should move toward $500,000 minimum. Portfolios exceeding 50 units typically need $1 million or higher, and high-crime areas or buildings with aging infrastructure warrant the upper range.

For serious portfolios exceeding 100 units, a commercial umbrella policy extends an additional $2 million to $5 million above your primary policy and becomes essential. The cost of a single catastrophic liability claim can exceed your annual premium by tenfold, making this protection a financial necessity rather than an optional add-on.

Loss of Rent Coverage Protects Your Cash Flow During Repairs

Loss of rent coverage protects your cash flow when units become uninhabitable during repairs. This coverage reimburses you for lost rental income during the repair period, typically covering 12 months minimum. A 10-unit building with $1,000 monthly rent per unit facing a three-month reconstruction period would lose $30,000 without this protection. The policy reimburses you at your actual rental rate, not some arbitrary figure, so accurate rent documentation matters when you file a claim. This protection becomes your financial lifeline when major damage forces you to halt rent collection while contractors work.

Understanding these coverage components helps you assess whether your current limits match your actual exposure. The next step involves comparing how different carriers price these protections and which ones offer the flexibility your portfolio needs.

Sizing Your Coverage to Match What You Actually Own

The biggest mistake multifamily owners make is letting their agent pick coverage limits instead of doing the math themselves. Your portfolio size and tenant composition determine what you need, and there’s no one-size-fits-all answer. A five-unit duplex in a stable neighborhood requires fundamentally different protection than a 50-unit complex in a high-turnover urban market.

Calculate Your Replacement Cost

Start with your actual replacement cost for the building structure. For older Class B and C properties like the 200-unit Ohio portfolio paying $510 per unit annually, replacement costs typically run $80,000 to $120,000 per unit depending on local construction costs and building condition. Multiply that by your unit count, and you’ll know the ballpark figure your policy must cover. This number forms the foundation of your coverage decision and prevents you from underinsuring your assets.

Assess Your Liability Exposure Honestly

Properties with younger tenants, ground-floor units, or swimming pools generate more injury claims than small owner-occupied duplexes. High-crime neighborhoods increase both property damage and liability risk. One slip-and-fall injury can cost $100,000 in medical expenses and legal defense fees within weeks. Document your actual monthly rent per unit because loss of rent coverage reimburses based on what tenants actually pay, not what you think they should pay. A $950 monthly rent on a 10-unit building means $9,500 per month in potential lost income during repairs.

Choose Loss of Rent and Deductible Levels

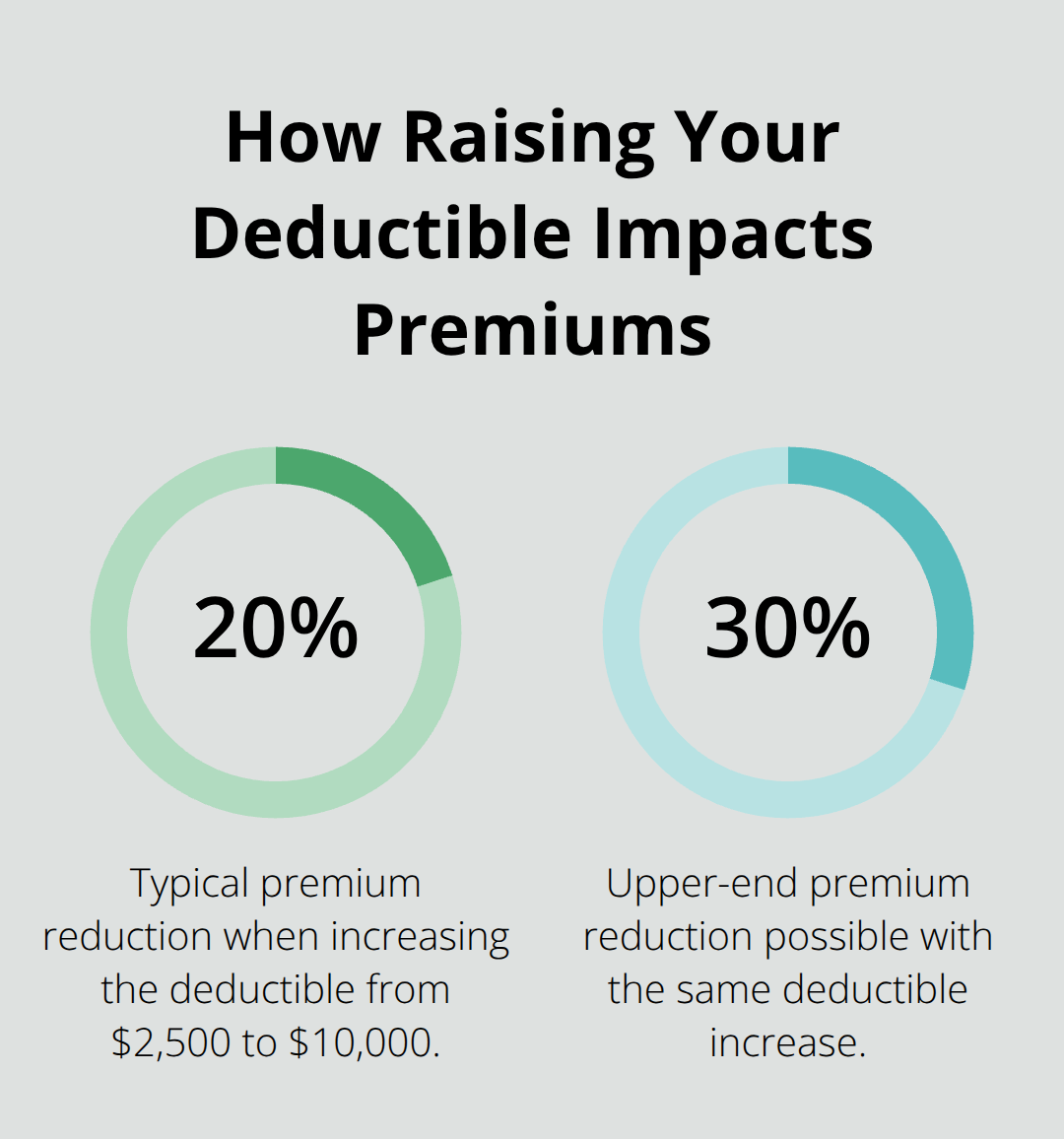

Loss of rent protection should cover at least 12 months, though properties in areas with lengthy permit delays or older buildings needing extensive work might justify 18 or 24 months of coverage. Your deductible choice directly impacts your annual premium, and this is where many owners leave money on the table. Increasing your deductible from $2,500 to $10,000 can cut your premium by 20 to 30 percent, but only if you can absorb that out-of-pocket cost without financial strain. For the Ohio portfolio, the $10,000 deductible reduced the total annual cost to roughly $44,000, making it a reasonable choice for cash-flowing properties.

Compare Quotes Across Multiple Carriers

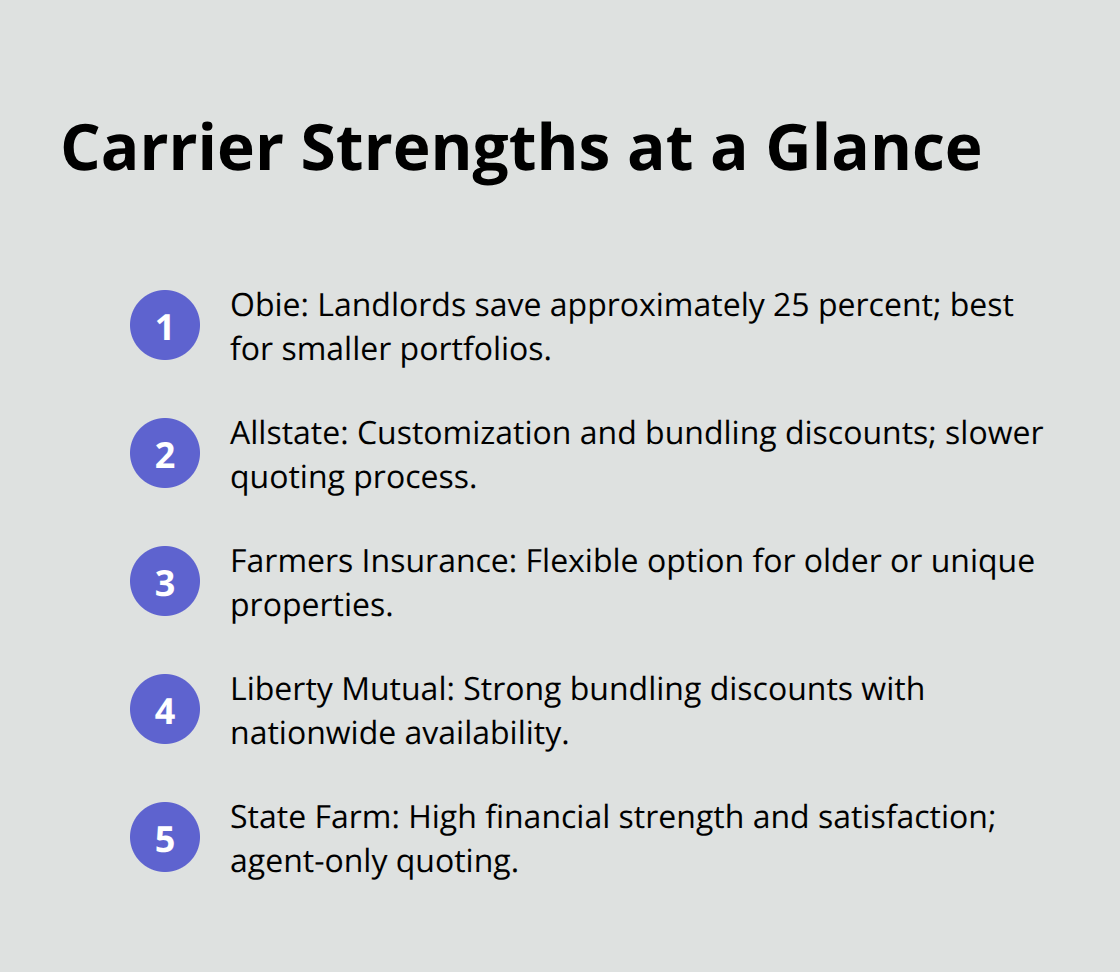

Comparing quotes across multiple carriers reveals how dramatically pricing varies for identical coverage. Obie, a digital-first insurtech, reports that landlords save approximately 25 percent on premiums through their platform compared to traditional carriers, though their model works best for smaller portfolios. Allstate emphasizes customization and bundling discounts when you combine multiple policies, but their quoting process moves slower than digital competitors.

Farmers Insurance excels with older or unique properties, offering flexibility that standard carriers won’t match. Liberty Mutual provides strong bundling discounts and nationwide availability, making it attractive if you want a single provider managing all your insurance needs. State Farm’s rental dwelling policies carry high financial strength ratings and strong customer satisfaction scores, but they require working through exclusive local agents without direct online quoting.

Get at least three quotes from different carrier types-an insurtech for speed, a traditional carrier for bundling potential, and a commercial specialist for larger portfolios. When comparing, ignore the headline premium number. Instead, compare what each carrier includes in their base coverage, what costs extra, and how they handle loss of rent calculations. Some carriers reimburse actual rent lost; others use a percentage of your annual rent. Some include water damage from all sources; others exclude sewer backup unless you add a rider. Request quotes with identical deductibles and liability limits so the numbers actually mean something.

Work With an Independent Agent

An independent agent representing multiple carriers becomes invaluable because they understand how different companies price risk and which ones align with your specific situation. This approach takes more time upfront but typically saves owners thousands annually while delivering coverage that actually fits your portfolio rather than some generic template.

Final Thoughts

A multifamily homeowners policy protects what matters most to your rental business: your property, your tenants’ safety, and your cash flow. The coverage you’ve learned about in this guide-replacement cost protection, liability limits scaled to your portfolio size, and loss of rent reimbursement-forms a financial safety net that standard homeowners policies simply cannot provide. Without these protections, a single fire, water damage event, or tenant injury claim can devastate your investment and eliminate months of rental income while repairs happen.

The real cost of inadequate coverage isn’t the premium you save by cutting corners. It’s the $30,000 in lost rent during a three-month repair period, the $100,000 liability settlement from a slip-and-fall injury, or the $500,000 reconstruction bill after a major loss. These scenarios happen regularly to multifamily owners who underestimated their exposure or chose the cheapest quote without understanding what they were actually buying. Getting the right coverage requires three concrete steps: calculate your actual replacement cost by multiplying your per-unit construction cost by your total unit count, assess your liability exposure honestly by considering your tenant demographics and property location, and request quotes from at least three different carriers using identical coverage specifications so you can compare apples to apples.

An independent agent who represents multiple carriers becomes your partner in this process. H&K Insurance Agency serves landlords and property owners throughout the Puget Sound region by comparing rates across top carriers and customizing coverage that fits your specific portfolio. Contact us today to discuss your multifamily homeowners policy needs and get a quote that reflects what you actually own.