Smart Auto Insurance Quotes Seattle To Lock In The Best Rate

Auto insurance quotes in Seattle vary wildly depending on your driving history, vehicle type, and coverage choices. Getting multiple quotes is the only way to find rates that actually match your situation.

We at H&K Insurance Agency help Seattle drivers compare options and cut through the noise. This guide walks you through how quotes work, proven strategies to lower costs, and what to evaluate when choosing coverage.

How Auto Insurance Quotes Work in Seattle

Understanding Rate Factors Insurers Use

Insurers in Seattle calculate your rate using seven core factors, and understanding them helps you anticipate what quotes will show. Your driving history carries the most weight-even one minor violation can lead to higher costs. Age matters significantly; a 20-year-old pays around $6,011 annually for full coverage while a 35-year-old pays $2,877, according to NerdWallet’s January 2026 analysis. Your vehicle itself affects cost substantially-a 2013 Toyota Corolla averages $176.13 monthly in Seattle while a 2023 Tesla Model 3 averages $102.17, showing that newer safety features lower rates. Location within Seattle creates dramatic variation; ZIP code 98110 averages $65.42 monthly while 98101 averages $143.81 for the same driver profile. Credit score impacts pricing even though it seems unrelated to driving ability-poor credit can add hundreds annually. Finally, your coverage choices determine the quote; full coverage costs more than minimum liability, but the protection difference is substantial when accidents happen.

Why Multiple Quotes Matter for Finding Better Rates

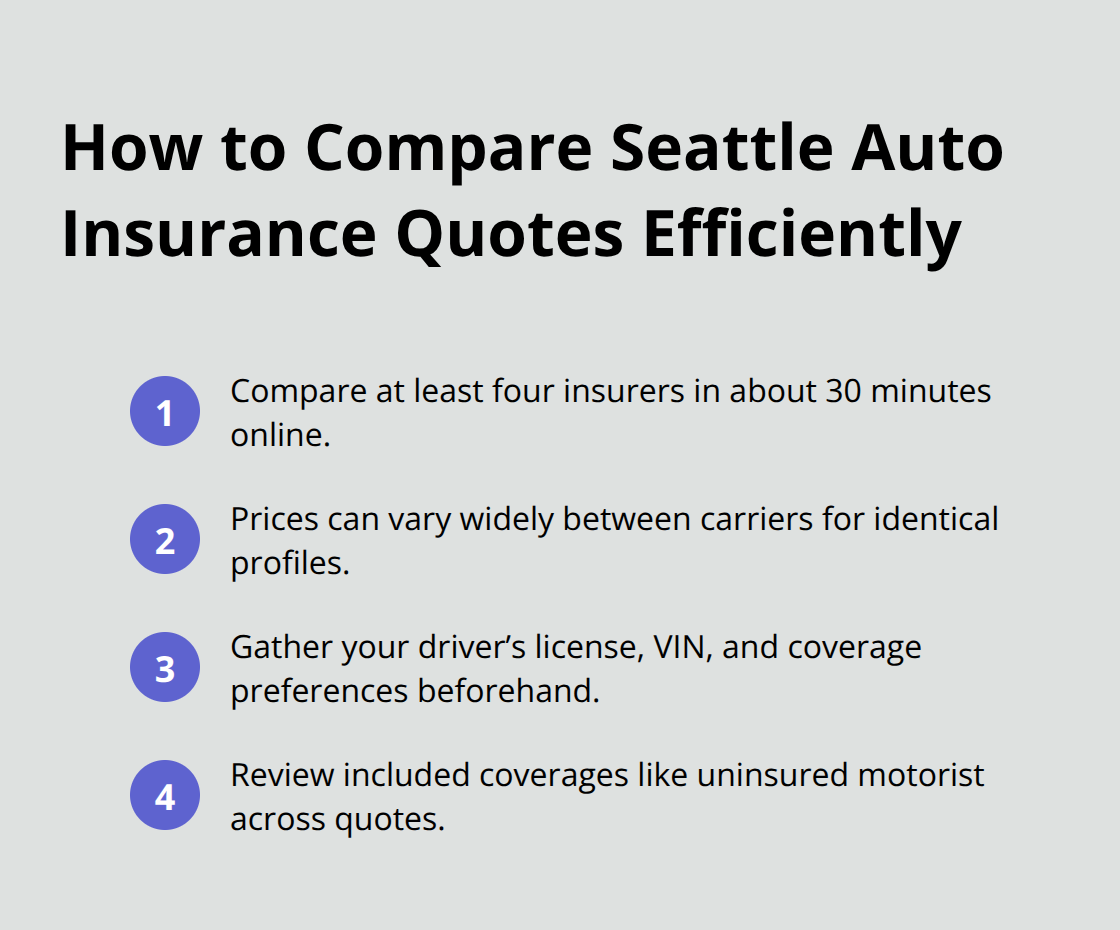

One quote tells you nothing about your real options in Seattle. Direct General averages $46.02 monthly for some drivers while State Farm averages $101.80 for identical profiles, a difference of over $660 annually. Collecting quotes from at least four different insurers takes roughly 30 minutes online and reveals which carriers price your specific situation competitively.

USAA, Kemper, and Travelers consistently appear among the lowest-cost options for drivers with clean records, but their rates only matter if they serve your profile-USAA limits membership to military families and veterans. Infinity Special offers competitive rates for teen drivers at $51.98 monthly compared to Dairyland Auto at $75.86, yet neither insurer works well for every age group. The quote process itself is straightforward; you provide your driver’s license, vehicle identification number, and coverage preferences, then receive estimates within minutes. Comparing quotes reveals not just price differences but coverage variations-one insurer might include uninsured motorist protection while another charges extra for identical protection.

Timeline for Getting Quotes and Comparing Options

Quote validity typically lasts 30 to 45 days, meaning you have roughly five weeks to decide before needing fresh quotes. Seattle’s insurance market moves quickly; rates shift based on seasonal claims data and carrier adjustments, so delaying comparison costs money. Once you identify your best option, purchasing coverage takes 15 minutes online or a quick call to an agent. The comparison window matters because premium increases happen frequently-waiting two months for a quote might mean paying 5 to 10 percent more when rates adjust. Taking action within your 30 to 45-day quote window locks in current pricing and gets you covered without unnecessary delays. With multiple quotes in hand and a clear timeline, you’re ready to explore the strategies that actually reduce what you pay each month.

Strategies to Lower Your Auto Insurance Costs

Bundle Policies for Maximum Discounts

Bundling auto insurance with homeowners or renters coverage can save you up to $1,356 when bundling auto and home insurance, making it an effective way to lower your monthly bill. Most Seattle drivers spread policies across multiple insurers, but consolidating everything under one carrier triggers substantial discounts. Managing claims becomes simpler when one insurer handles both your auto accident and home damage claim.

You avoid coordinating between separate companies and reduce administrative hassle. H&K Insurance Agency represents multiple top local and national carriers, allowing you to compare bundled rates and customize packages so you get the right protection at competitive prices. However, bundling only works if the combined rate beats what you’d pay separately, so always compare the bundled quote against individual policies before committing. Some carriers bundle more aggressively than others; USAA and Kemper offer competitive bundled rates for eligible members, while Direct General focuses primarily on auto coverage.

Adjust Coverage Levels Based on Your Vehicle and Driving Habits

Raising your deductible from $500 to $1,000 typically lowers your monthly premium by 10 to 15 percent, but only choose this option if you can reliably cover the higher out-of-pocket cost when an accident happens. Your vehicle choice matters significantly-a 2023 Tesla Model 3 costs $102.17 monthly to insure in Seattle while a 2013 Toyota Corolla costs $176.13, so collision and comprehensive coverage on older vehicles sometimes costs more than the vehicle’s actual value.

If your car is paid off and worth under $5,000, dropping collision and comprehensive coverage and keeping only liability makes financial sense. You protect your assets without overpaying for protection on a depreciating vehicle. Seattle drivers with good records and clean credit should ask about low-mileage discounts if they drive fewer than 10,000 miles annually; this alone can reduce rates by 5 to 15 percent.

Take Advantage of Safety Features and Low-Mileage Discounts

Anti-lock brakes trigger roughly 3 percent discounts, while bundling auto-pay typically saves another 5 percent, so combining these adjustments stacks savings across multiple categories. You accumulate discounts by addressing each factor rather than overlooking smaller opportunities. The key is comparing your actual quote changes when you adjust each setting rather than assuming standard discount amounts apply to your specific situation.

With these cost-reduction strategies in hand, you’re ready to evaluate which quotes actually deliver the best value for your specific needs and driving profile.

What to Look for When Comparing Seattle Auto Insurance Quotes

Evaluating Coverage Limits and Deductibles

Coverage limits and deductibles form the foundation of your comparison and directly determine what you pay after an accident. Washington requires minimum liability of 25/50/10-$25,000 per person, $50,000 per accident for bodily injury, and $10,000 for property damage-but this baseline leaves you exposed if you’re at fault in a serious crash. Seattle experienced 7,908 crashes in 2024 with 2,700 injuries, meaning the risk of exceeding minimum coverage is real. A driver with $50,000 in liability limits who causes a multi-vehicle accident faces personal asset liability beyond that amount, making higher limits worth the modest premium increase.

Compare quotes at $50,000, $100,000, and $250,000 liability levels rather than accepting each carrier’s standard recommendation. Deductible comparisons reveal hidden costs; a $500 deductible quote looks cheaper until a claim happens and you owe $500 out of pocket, while a $1,000 deductible might save $15 monthly but costs twice as much when you file. Calculate your total cost if a claim occurs, not just the premium amount.

Assessing Customer Service and Claims Support

Customer service quality and financial stability separate insurers that simply take your money from those that actually pay claims when needed. Seattle drivers filing claims during rain-heavy months face processing delays with some carriers while others prioritize quick resolution, yet this performance difference rarely appears in online quotes.

Call each insurer’s claims line before purchasing and describe a hypothetical accident; note response time, clarity of instructions, and whether they offer 24/7 support or business-hours-only service.

Ask quotes specifically about digital claims filing and photo submission since Seattle’s frequent accidents mean faster processing saves time and frustration. The cheapest quote becomes expensive fast when claims take months to resolve or get denied due to carrier problems.

Checking Financial Stability of Insurance Carriers

Financial strength matters critically because an insolvent insurer cannot pay your claim regardless of your policy language. Check each carrier’s financial stability of insurance carriers through AM Best, which rates insurers A++ down to C; carriers rated A- or better have minimal failure risk, while anything below A- signals potential problems. USAA, Kemper, and Travelers maintain A+ ratings according to AM Best data, while Direct General holds an A rating, making all viable options for claims reliability.

An independent agency like H&K Insurance Agency represents multiple top carriers with strong ratings, allowing you to compare both price and service quality rather than choosing blindly between unknown options.

Final Thoughts

The difference between the cheapest and most expensive auto insurance quotes Seattle offers for your profile can exceed $660 annually, making comparison non-negotiable if you want competitive pricing. Gather quotes from at least four different carriers this week and provide identical information to each insurer so comparisons stay accurate. Evaluate not just price but coverage limits, deductible options, and financial stability ratings through AM Best to confirm each carrier can pay claims when needed.

Calculate your total cost if an accident occurs rather than focusing only on monthly premiums, since a $15 monthly savings vanishes fast when your deductible doubles. Check AM Best ratings for each carrier before purchasing, and compare quotes at multiple liability levels ($50,000, $100,000, and $250,000) rather than accepting default recommendations. Take action within your 30 to 45-day quote validity window before rates shift again and lock in your best rate.

Contact H&K Insurance Agency to start comparing quotes today or call to discuss your specific situation with an agent who understands Seattle’s driving conditions and local insurance market. We represent multiple top local and national carriers, which means we compare rates and customize packages so you get the right protection at competitive prices. Rather than shopping alone across dozens of websites, working with a local independent agent saves time and reveals bundling opportunities you might miss.