Rental Property Insurance Bremerton: Landlord Insurance That Covers Your Assets

Owning rental property in Bremerton comes with real financial exposure. Standard homeowners insurance won’t protect your investment because it doesn’t cover the unique risks landlords face.

At H&K Insurance Agency, we’ve seen too many property owners discover gaps in their coverage when it’s too late. Rental property insurance in Bremerton is specifically designed to handle what homeowners policies miss.

What Your Landlord Insurance Actually Protects

Landlord insurance in Bremerton covers three critical areas that standard homeowners policies explicitly exclude. First, it protects the building structure itself-your dwelling, attached structures, and permanently installed fixtures-using a DP-3 form with replacement cost value rather than actual cash value. This matters because Washington construction costs rose about 15% from 2020 to 2023, according to the WA State Office of the Insurance Commissioner, and Bremerton rebuild costs now run $350 to $500 per square foot. When a covered peril like fire, wind, or theft damages your rental, replacement cost coverage pays what it actually costs to rebuild today, not what the structure depreciated to. Second, landlord policies include liability protection specifically for rental activities. Standard homeowners liability tops out at $100,000 to $300,000, which is dangerously low in Washington. Washington’s comparative negligence laws raise your exposure significantly-a tenant injured on your property or someone hurt due to your negligence could claim $50,000 to $100,000 or more. You need at least $500,000 in liability coverage per occurrence, and if you own multiple properties or have high-risk features like pools, an umbrella policy of $1 million or more is essential. Third, loss of rental income coverage reimburses your actual lost rent when a covered peril makes units uninhabitable. In Seattle, six months of vacancy can exceed $13,000 in gross rent alone, and most policies cover 12 to 24 months of lost income. This protects your cash flow during the critical recovery period after a loss.

Why Replacement Cost Matters More Than You Think

Actual cash value policies pay depreciated amounts, leaving you short when rebuilding. A 20-year-old roof worth $8,000 in actual cash value might cost $15,000 to replace today. Replacement cost eliminates this gap. When you compare quotes, verify every policy uses replacement cost value and DP-3 coverage, not actual cash value or DP-1. This single choice can mean the difference between recovering fully and absorbing thousands in out-of-pocket costs after a loss.

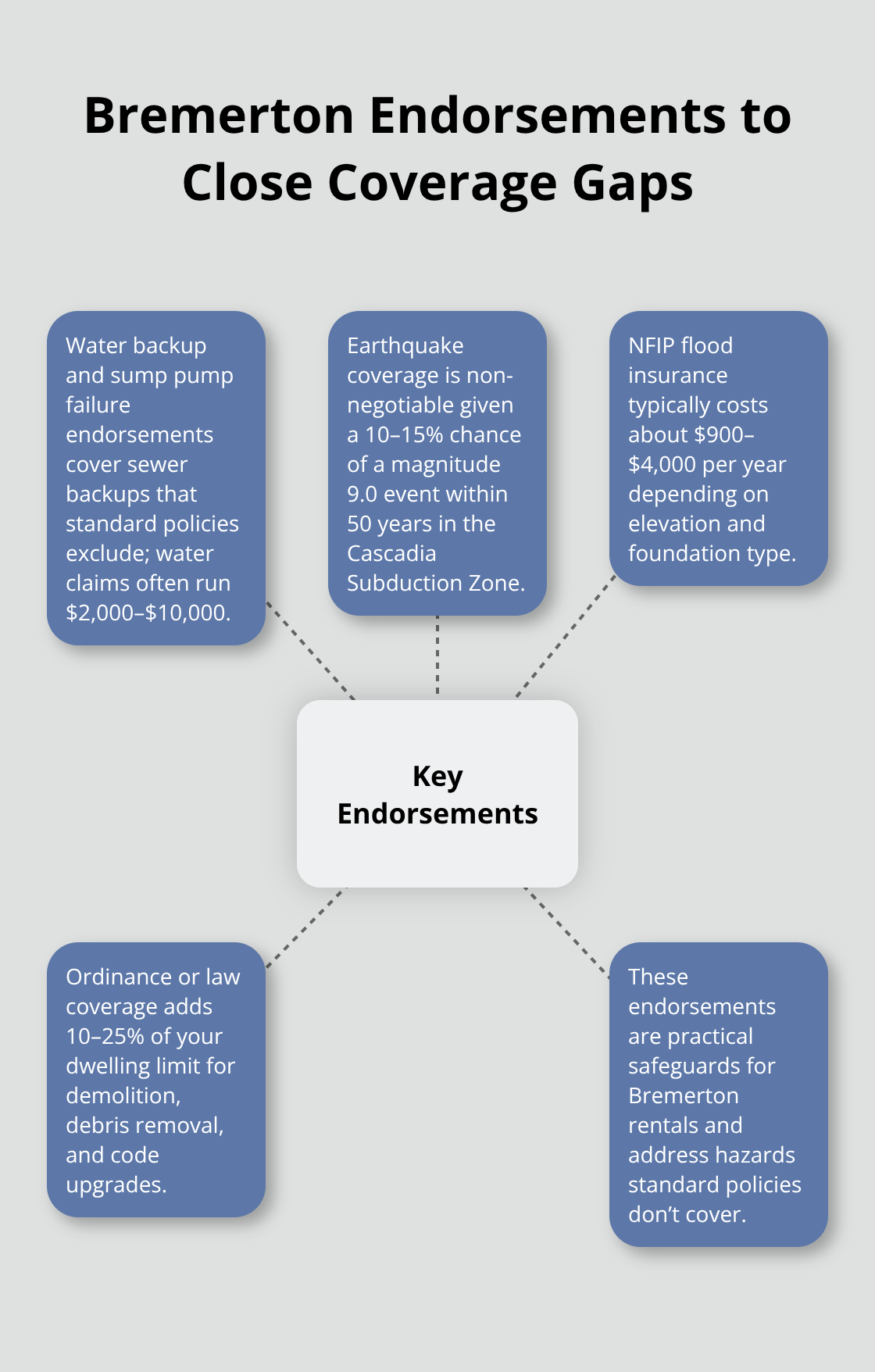

Special Endorsements for Bremerton Properties

Water damage claims in Washington typically range from $2,000 to $10,000, and standard policies exclude sewer backups-a common problem in the Puget Sound area. You should add water backup and sump pump failure endorsements to close this gap. The Cascadia Subduction Zone carries a 10 to 15 percent probability of a magnitude 9.0 earthquake within 50 years, according to the USGS, making earthquake coverage non-negotiable for Bremerton landlords. About 175,000 structures statewide sit in mapped floodplains, and flood insurance through the National Flood Insurance Program costs roughly $900 to $4,000 per year depending on elevation and foundation type. Ordinance or law coverage adds 10 to 25 percent of your dwelling limit to cover demolition, debris removal, and code upgrades during rebuilding-expenses standard policies don’t address.

These endorsements aren’t optional extras; they’re practical safeguards against the specific hazards Bremerton rental properties face.

How to Identify Coverage Gaps in Your Current Policy

Most landlords don’t realize their standard homeowners policy excludes rental income protection until they file a claim. You need to pull your current policy and check three things: whether it covers loss of rent, whether it includes water backup protection, and whether earthquake or flood coverage is listed. If any of these protections are missing, your policy leaves you exposed to the exact risks that hit Bremerton properties most often. An independent agency representing multiple carriers can help you spot these gaps and fill them without overpaying for unnecessary coverage.

Why Your Homeowners Policy Won’t Protect Your Rental

Standard homeowners policies are written for owner-occupied homes, not rental properties. The moment you rent out your home or purchase a property specifically for rental income, your standard policy becomes practically worthless. Insurance companies explicitly exclude loss of rental income, meaning if a fire makes your unit uninhabitable for six months, you absorb every penny of lost rent with no coverage. This isn’t a loophole or a technicality-it’s a deliberate exclusion built into every homeowners policy sold in Washington. Many landlords don’t realize this gap exists until they file a claim and face denial. The liability exposure is even worse. Standard homeowners liability covers injuries or property damage that occur at your owner-occupied home, but rental properties trigger a completely different risk profile. A tenant slips on your stairs, a guest gets injured, or someone claims negligence related to maintenance-these situations fall outside your homeowners liability limits. Washington’s comparative negligence laws mean you’re financially responsible for a percentage of damages based on your degree of fault, even if you’re only partially to blame. A $100,000 homeowners liability limit evaporates instantly in a serious claim. Landlords need at least $500,000 per occurrence, and multiple properties or high-risk features demand $1 million or more through an umbrella policy.

The Rental Income Problem Homeowners Policies Ignore

Losing six months of rent isn’t just an inconvenience-it’s a financial catastrophe most landlords can’t absorb. In Seattle, six months of vacancy on a typical rental exceeds $13,000 in gross rent alone, and Bremerton properties follow similar patterns. Standard homeowners insurance pays zero during this period. Your mortgage, property taxes, maintenance costs, and utilities continue while your income stops. Landlord policies cover 12 to 24 months of lost rental income, protecting your cash flow during the critical recovery period after a covered loss. Without this protection, you’re essentially self-insuring the income gap, which is financially reckless for any serious property owner.

Liability Claims Expose Your Personal Assets

Washington’s liability environment makes adequate coverage non-negotiable. Property crime in Washington exceeds the national average according to FBI crime statistics, and landlords face liability claims ranging from $5,000 for minor injuries to $100,000 or more for serious incidents. A tenant injured due to faulty wiring, a visitor hurt by a collapsing deck, or property damage caused by your negligence-these claims hit hard and fast. Your homeowners policy’s $100,000 to $300,000 liability limit won’t cover the gap. Courts routinely award judgments well above standard homeowners limits, and your personal assets become vulnerable. A proper landlord policy with $500,000 minimum liability protection, combined with an umbrella policy for additional coverage, protects your savings, your primary residence, and your future income from catastrophic claims. This protection is especially critical in Bremerton, where the military presence and strong rental market create dense tenant populations and higher accident exposure.

What Happens When You File a Claim

When a covered loss strikes your rental property, your homeowners insurer will deny the claim if rental activity is involved. The policy language explicitly states that coverage applies only to owner-occupied dwellings. You’ll receive a denial letter, and you’ll be left to cover repair costs, lost income, and liability exposure entirely out of pocket. This scenario plays out repeatedly for landlords who assume their homeowners policy provides adequate protection. A landlord policy, by contrast, accepts the rental nature of your property and covers the specific perils that affect rental operations. The claims process moves forward without the denial that would accompany a homeowners policy claim. Understanding this distinction before a loss occurs allows you to secure the right coverage and avoid financial devastation when you need protection most.

Finding the Right Coverage for Your Bremerton Rental

Gather Your Property Details Before Requesting Quotes

Start by pulling together three pieces of information about your property before requesting any quotes. Document the year built, square footage, construction type, number of units, and current replacement cost estimate for the building. If you’ve had a recent appraisal or contractor estimate, that information helps insurers set dwelling limits accurately. Next, detail your tenant situation: are you renting long-term, short-term through platforms like Airbnb, or both? Short-term rentals carry premiums 20 to 40 percent higher than long-term rentals and are frequently excluded by standard carriers without specialized riders, so this distinction matters enormously for pricing. Include information about any high-risk features like pools, trampolines, or previous claims on the property. This groundwork prevents quote delays and ensures you compare apples to apples across different carriers.

Compare Quotes from Multiple Insurers

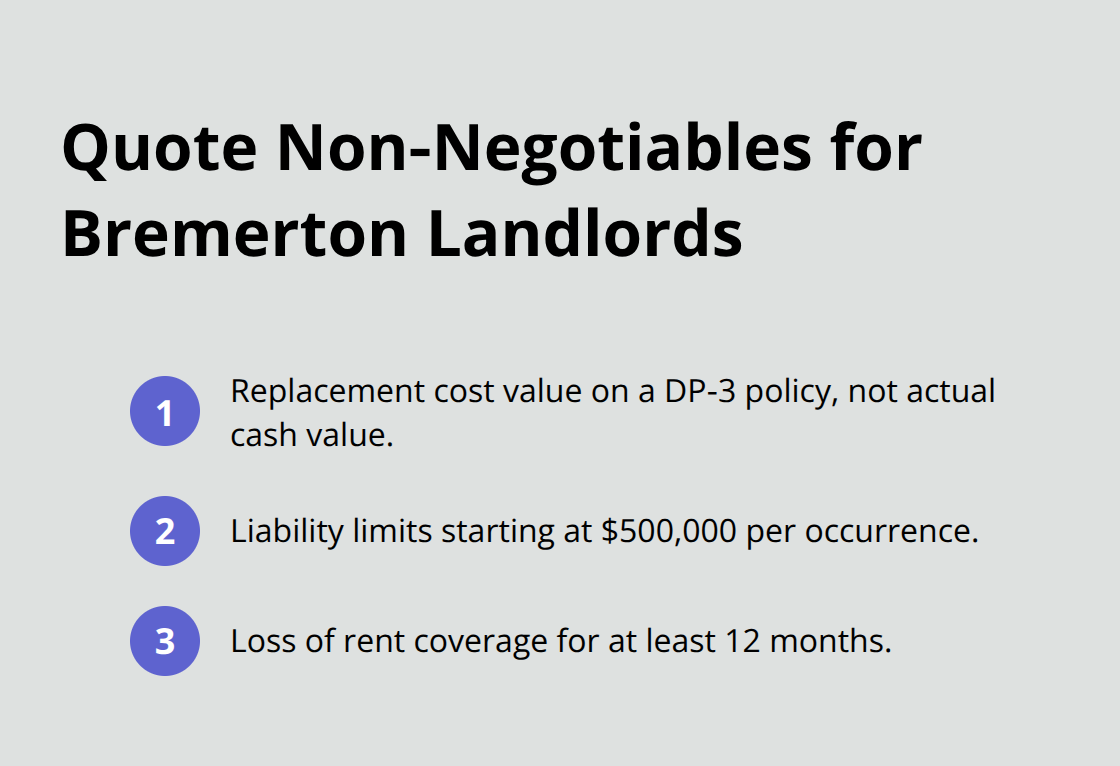

Get quotes from at least three insurers using identical property details-premium variation for identical coverage regularly exceeds 35 percent, meaning the difference between a $1,200 annual policy and a $1,600 policy for the same protection is completely normal. When comparing quotes, verify three non-negotiable elements: replacement cost value (never actual cash value), liability limits starting at $500,000 per occurrence, and loss of rent coverage for at least 12 months.

If a quote is missing any of these, reject it immediately rather than trying to negotiate later. Check the insurer’s financial strength with AM Best ratings of A− or higher-you want confidence they’ll pay when disaster strikes.

Maximize Savings Through Bundling and Deductible Adjustments

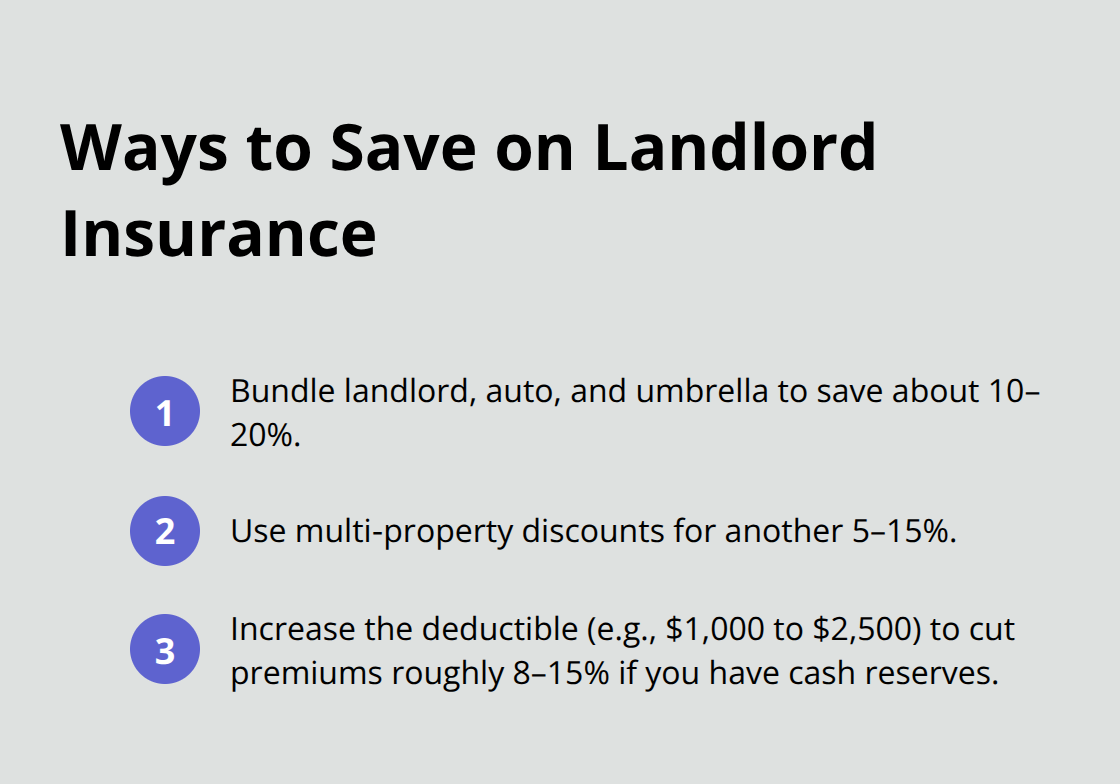

Bundling landlord coverage with auto, umbrella, or other policies cuts total premiums by 10 to 20 percent, and multi-property discounts can save an additional 5 to 15 percent. If you own two rentals and carry auto insurance elsewhere, consolidating everything with one carrier typically yields larger savings than keeping policies scattered. Increasing your deductible from $1,000 to $2,500 reduces premiums by roughly 8 to 15 percent, but only make this move if you have cash reserves to cover larger out-of-pocket losses after a claim.

Act Before Rate Increases Take Effect

Washington home insurance rates rose 19.5 percent over the past year, so locking in favorable terms before your renewal is critical. Rate increases accelerate during renewal periods, and delays cost you money. An independent agency representing multiple top carriers beats shopping solo because they handle the comparison work and tailor options to your specific property type and risk profile without steering you into overpriced standard programs. In Bremerton, an independent agency familiar with local hazards and rental market conditions can match you with carriers that understand Puget Sound risks and price accordingly.

Final Thoughts

Rental property insurance in Bremerton protects your investment where standard homeowners policies fail completely. You’ve learned the gaps: missing rental income coverage, inadequate liability limits, and exclusions for the exact perils that threaten Puget Sound properties. The right landlord policy combines replacement cost dwelling coverage, at least $500,000 in liability protection, 12 months of loss of rent coverage, and specialized endorsements for water damage, earthquakes, and floods.

Your specific property and tenant situation demand customized coverage that most landlords overlook. A single-family long-term rental has different needs than a multi-unit building or short-term rental property, and your deductible choice, bundling strategy, and endorsement selections all affect both your premium and your protection level. An agent who understands your property type and local risk factors prevents you from overpaying for unnecessary coverage or leaving dangerous gaps in protection.

We at H&K Insurance Agency represent multiple top carriers and compare rates across all of them so you receive the right protection at competitive prices. Washington home insurance rates rose 19.5 percent over the past year, making timing critical-contact H&K Insurance Agency today to request quotes for your Bremerton rental property and lock in favorable terms before your renewal.