Personal Umbrella Coverage Puget Sound: Extra Liability When It Matters

Your home and auto insurance policies have limits. When a serious accident happens, those limits can vanish in days.

We at H&K Insurance Agency see this problem regularly in the Puget Sound area. Personal umbrella coverage Puget Sound residents need fills the gap between what your standard policies cover and what you actually owe after a major incident.

Why Standard Coverage Falls Short

Washington’s Minimum Requirements Leave You Exposed

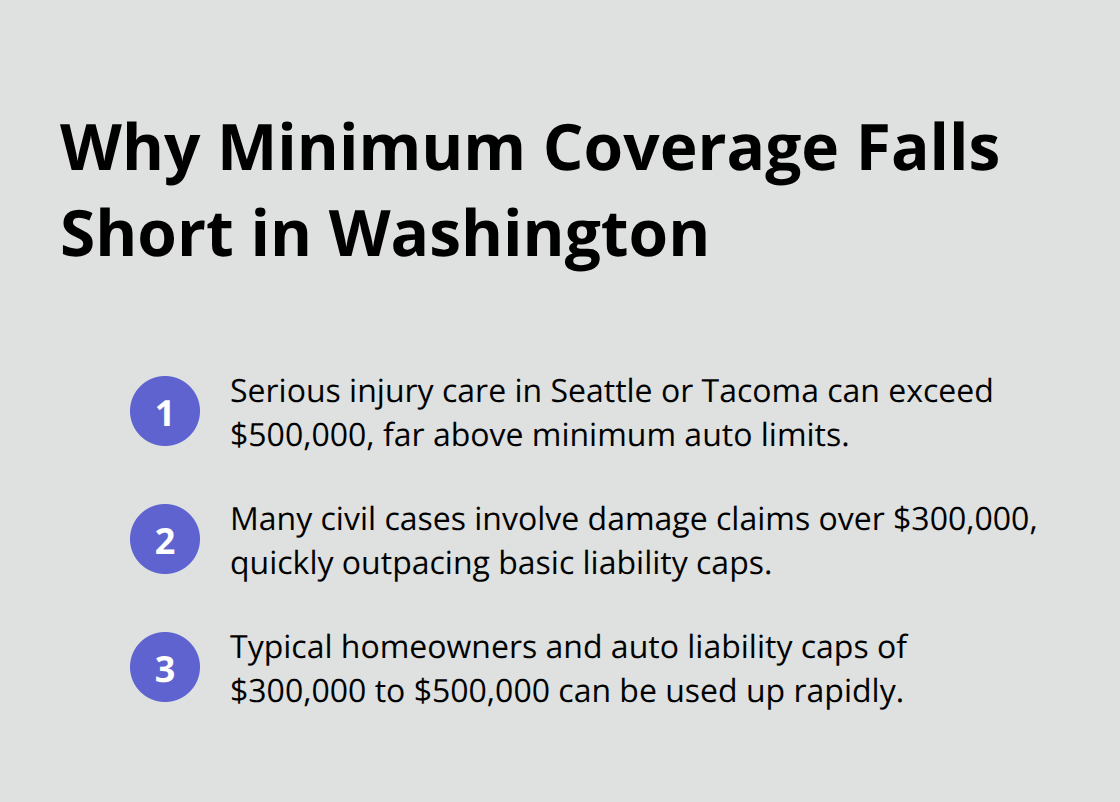

In Washington, the minimum auto liability requirement is $25,000 per person for bodily injury-a number that hasn’t kept pace with real-world accident costs. A single serious injury claim at a hospital in Seattle or Tacoma reaches $500,000 or more when you factor in ongoing medical care, lost wages, and pain and suffering damages. Washington state trial courts processed more than 81,000 civil cases in 2022, and roughly one in five involved damage claims exceeding $300,000. Your homeowners policy typically caps personal liability at $300,000 to $500,000, and your auto policy at similar levels.

When a major accident happens, these limits evaporate within days.

Medical Bills and Legal Fees Accumulate Rapidly

Medical bills alone from a severe injury-surgery, rehabilitation, long-term care-easily top $400,000. Add attorney fees, court costs, and the gap widens fast. Legal defense costs alone can reach $150,000 to $250,000 in a contested case, and many standard policies exhaust their limits before litigation even concludes. These expenses stack on top of the actual settlement or judgment, leaving you personally responsible for amounts your policies don’t cover.

Your Assets Face Real Risk in the Puget Sound Region

A backyard accident on your property or a traffic incident you cause can result in a judgment far larger than your policy limits. The plaintiff’s attorney will pursue your personal assets-your savings, home equity, and future wages-if the judgment exceeds what your policies pay. In the Puget Sound region, median home values surpassed $590,000 in 2023 according to the Northwest Multiple Listing Service, meaning your equity is substantial and therefore vulnerable. If you own rental property or have multiple vehicles, your exposure multiplies. Boating on Lake Union or hosting social events on your property increases the likelihood of a serious claim. One catastrophic incident can wipe out decades of financial progress, which is why understanding your actual liability exposure matters before a claim arrives.

How Umbrella Coverage Actually Works

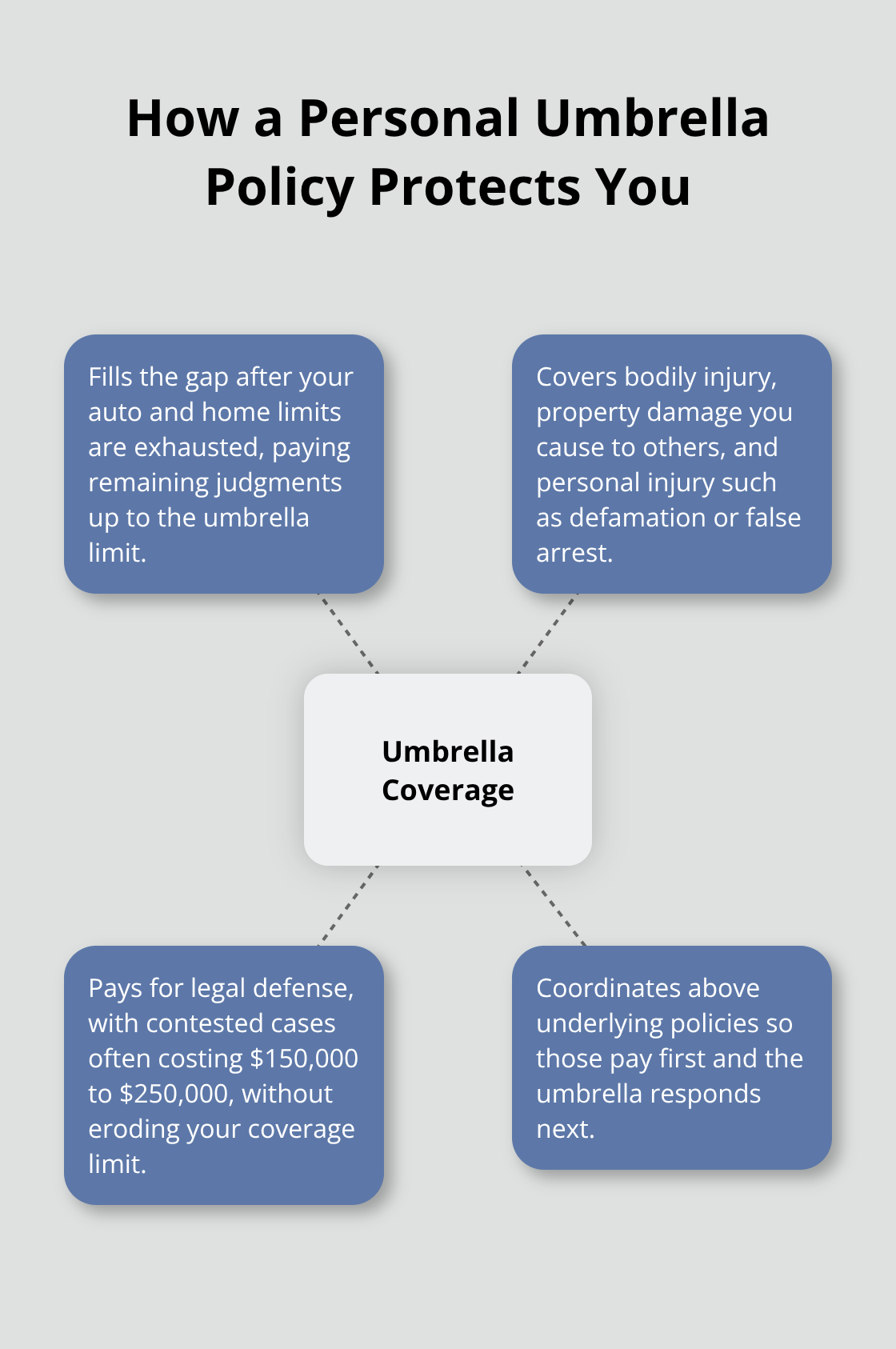

Personal umbrella insurance sits on top of your auto and home policies and activates only after those limits are exhausted. Here’s how it works: if a lawsuit results in a $1.2 million judgment and your auto policy covers $300,000 while your homeowners covers $500,000, your umbrella policy covers the remaining $400,000 up to its limit. This layered structure means your underlying policies pay first, then the umbrella fills the gap. The coverage applies to bodily injury claims, property damage you cause to others, and personal injury claims like defamation or false arrest. The umbrella also covers legal defense costs, which typically run $150,000 to $250,000 in contested cases.

These defense expenses often sit outside your underlying policy limits, so the umbrella absorbs them without reducing your coverage amount. A $1 million umbrella policy in Washington costs roughly $190 to $340 annually according to 2024 market data, making it surprisingly affordable given the protection it provides. The affordability works because you’re not duplicating coverage-your umbrella sits on top of existing policies rather than replacing them.

What the Umbrella Actually Covers

Your umbrella protects your assets when a claim exceeds what your standard policies will pay. In the Puget Sound region, real incidents demonstrate this value: a backyard trampoline injury with $900,000 in damages required the umbrella to cover $600,000 after the homeowners limit was reached, or a multi-vehicle accident on I-405 that exhausted a $300,000 auto limit left the umbrella to pay $1.4 million in excess damages plus $200,000 in legal fees. The umbrella extends to liability from rental properties you own, protecting against tenant injury claims or property incidents. It also covers boating, RVs, or motorcycles if you add the right riders. This coverage works regardless of which carrier holds your underlying policies, though bundling with one insurer typically simplifies claims coordination.

Eligibility Requirements and What You Need

To qualify for umbrella coverage, you need minimum underlying limits on auto and home policies-typically $300,000 in homeowners personal liability and similar auto bodily injury limits. If your current homeowners limit is only $100,000, you’ll need to raise it before an insurer will write your umbrella. The cost depends on your location within Puget Sound, number of homes and vehicles, driving history, and whether you own pools, trampolines, or have dogs. Starting at $1 million in coverage, most policies allow increments up to $10 million, and adding another $1 million typically costs $75 to $100 annually.

How to Get the Right Coverage for Your Situation

Your location, assets, and lifestyle in the Puget Sound region shape what umbrella limit makes sense. If your net worth exceeds $500,000, umbrella coverage becomes a practical necessity to protect your savings and home equity. An independent agent can compare quotes across multiple carriers and bundle your auto, home, and umbrella coverage to secure competitive rates and identify any gaps between policies. The right umbrella limit depends on your total assets and the specific risks you face-whether that’s waterfront property, rental income, or active boating on local lakes.

Puget Sound Risks That Standard Policies Miss

Boating and Water Activities Expose You to Massive Liability

The Puget Sound region presents liability exposures that most standard homeowners and auto policies simply don’t address adequately. Boating on Lake Union, Lake Washington, or Puget Sound itself creates substantial risk-a single collision between vessels or an injury to a passenger can generate claims exceeding $500,000 in medical costs and damages. Your homeowners policy typically excludes or severely limits boat liability, and your auto policy won’t touch watercraft incidents at all. If you own a boat, jet ski, or spend weekends on the water, umbrella coverage becomes essential because it extends to recreational watercraft with the right endorsements. Adding a boat or recreational vehicle rider to your umbrella typically costs $50 to $150 annually, making protection affordable relative to the exposure.

Backyard Incidents and Social Events Create Frequent Claims

The Puget Sound region’s active outdoor culture means properties host backyard gatherings, swimming pools, trampolines, and social events where injuries happen frequently. A guest slipping on your deck or a child injured on your trampoline can result in judgments that dwarf your standard homeowners limit of $300,000 to $500,000. Umbrella coverage fills this gap directly and affordably. These incidents occur regularly enough that insurers price umbrella policies to account for them, which is why the annual cost remains reasonable despite the serious nature of potential claims.

Rental Properties Generate Landlord Liability Your Homeowners Policy Won’t Cover

Rental properties in the Puget Sound area generate landlord liability exposure that standard homeowners policies don’t cover. If you own a condo, townhouse, or single-family rental, tenant injuries, property damage claims, or disputes escalate into lawsuits quickly, and your personal homeowners policy excludes these incidents. A tenant injured on your rental property’s stairs or a fire that damages adjacent units can produce judgments of $750,000 or more when you factor in legal defense costs. Umbrella policies specifically cover landlord liability once your underlying landlord policy limits are exhausted, protecting your rental income and personal assets from claims arising from properties you lease to others. The cost of adding landlord liability coverage to an umbrella policy runs $100 to $250 annually depending on the number of rental units and property values.

Coordination Across Multiple Carriers Prevents Coverage Gaps

Working with an independent agent ensures your umbrella coordinates seamlessly across multiple carriers-your auto insurer, homeowners carrier, and separate landlord policy all feed into one umbrella limit. This coordination prevents coverage gaps where a claim falls between policies or gets denied because insurers dispute which policy should pay first. An agent can confirm that your underlying policies meet the minimum limits required to qualify for umbrella protection and that endorsements on each policy align with your umbrella’s terms, eliminating disputes when a serious claim arrives.

Final Thoughts

A single serious accident in the Puget Sound region eliminates years of financial progress. A multi-vehicle collision on I-405, a guest injured at your home, or a tenant claim from your rental property generates judgments that far exceed what your standard auto and homeowners policies cover. When that judgment arrives, creditors pursue your savings, home equity, and future wages to satisfy the amount your policies won’t pay.

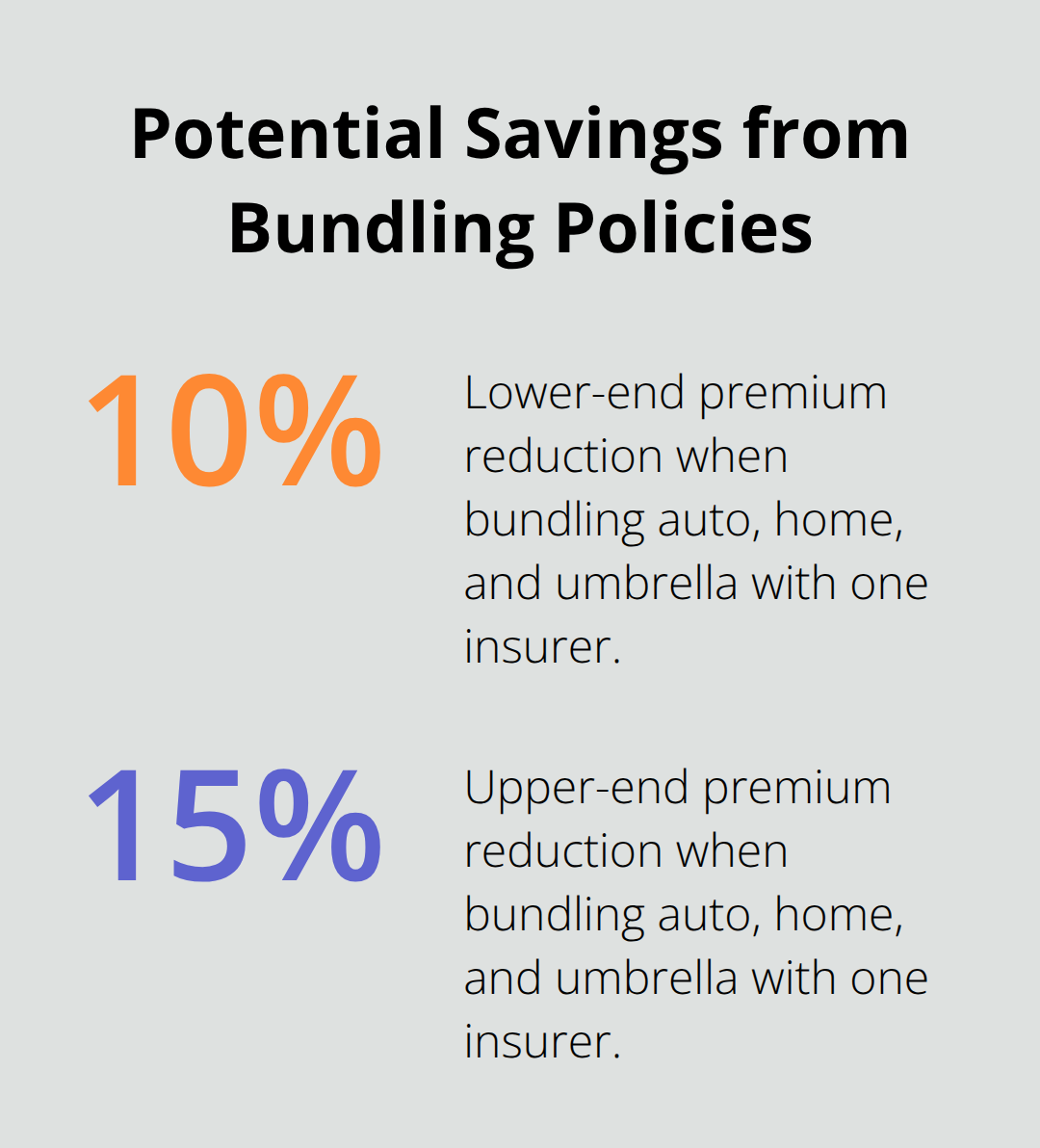

Personal umbrella coverage Puget Sound residents need costs far less than most people assume-a $1 million policy runs roughly $190 to $340 annually in Washington, which breaks down to less than $30 per month for protection that shields everything you’ve built. Adding another $1 million in coverage typically costs only $75 to $100 more per year, making higher limits surprisingly affordable as your assets grow. Bundling your auto, home, and umbrella coverage with one insurer reduces your total premiums by 10 to 15 percent across all policies combined.

Contact H&K Insurance Agency to discuss your umbrella needs and receive a quote that reflects your Puget Sound lifestyle and assets. We serve the Puget Sound region by comparing rates across multiple carriers and customizing packages that fit your actual exposure. As a locally owned, independent agency in Bremerton, we represent top carriers and can bundle your auto, home, boat, and umbrella coverage to secure competitive pricing while eliminating gaps between policies.