Multi-Unit Landlord Policy: Coverage That Protects Your Investment

Owning multiple rental units means managing more risk than a single-family home. Standard homeowners insurance simply won’t cut it-you need a multi-unit landlord policy designed for your specific situation.

At H&K Insurance Agency, we’ve seen too many landlords discover gaps in their coverage when it’s too late. The right policy protects your property, your tenants, and your income stream.

What Your Multi-Unit Landlord Policy Actually Covers

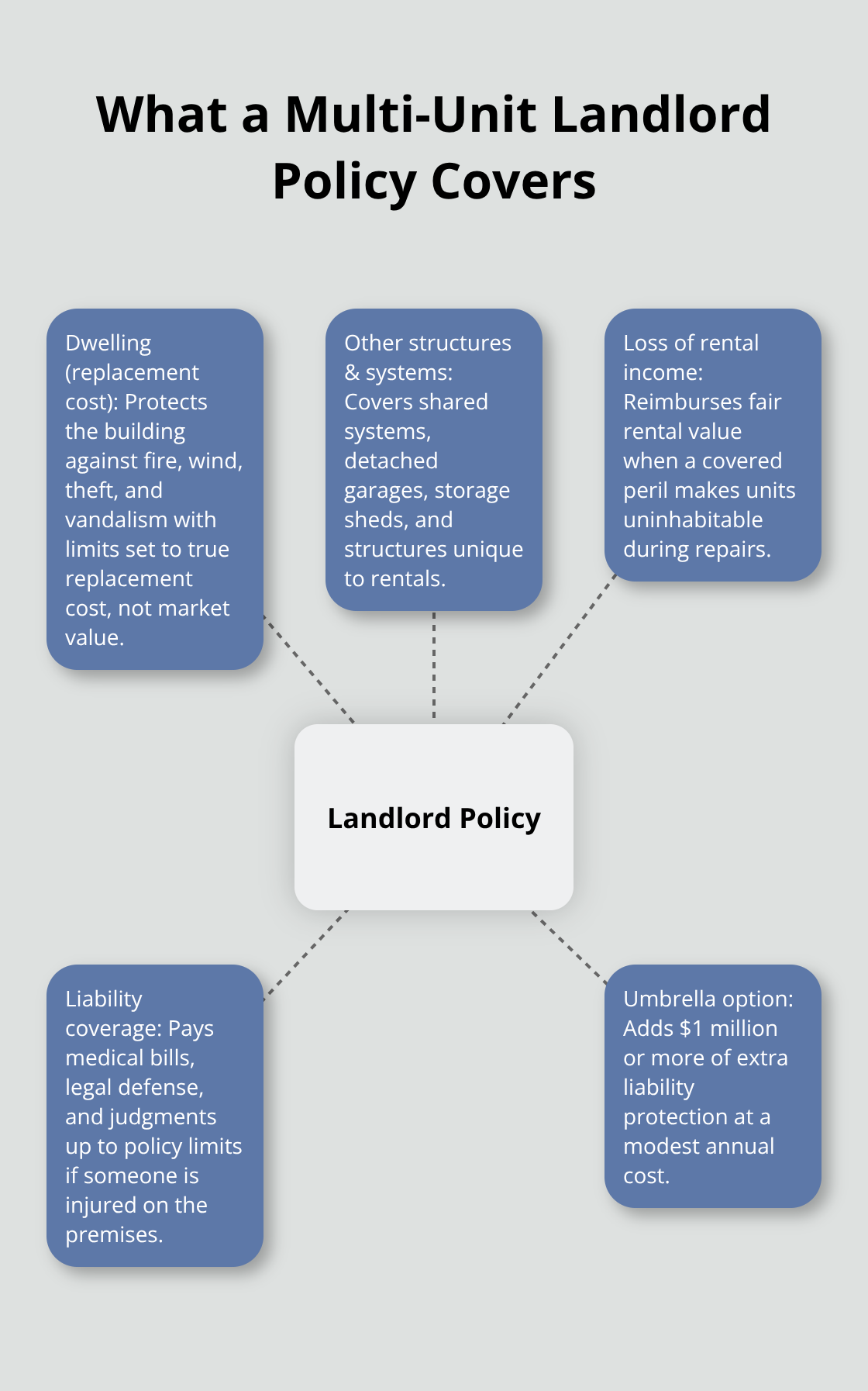

A multi-unit landlord policy covers three critical areas that standard homeowners insurance abandons the moment your property becomes a rental. The dwelling structure itself receives protection against fire, wind, theft, and vandalism, but here’s what matters: coverage limits must reflect replacement cost, not market value. If your four-unit building costs $450,000 to rebuild after a fire, your policy needs to match that number. Many landlords underestimate replacement costs and end up thousands of dollars short after a claim.

Your policy also covers the systems and structures unique to rental properties-the furnaces serving multiple units, detached garages, storage sheds, and other structures on the property. Loss of rental income coverage protects your cash flow when a covered peril makes the property uninhabitable. If a pipe bursts and damages two units, with repairs taking three months, this coverage reimburses the rent you’d normally collect, typically covering fair rental value for the period the property sits unlivable.

Liability Protection for Multi-Unit Exposure

Liability coverage is where multi-unit properties expose you to serious risk. A tenant’s guest slips on ice in the common hallway and breaks their leg-they sue you for medical bills and pain and suffering. Your liability coverage pays for their medical expenses, legal defense, and any judgment up to your policy limits. Most landlord policies include medical payments coverage as standard, which covers immediate medical costs without requiring a lawsuit, but the limits are often modest.

For a four-unit building, standard liability limits of $100,000 or $300,000 may not be enough if multiple people are injured in a single incident. Many multi-unit landlords add umbrella liability insurance on top of their base policy, extending protection to $1 million or more. The cost is reasonable-umbrella policies typically run $150–$300 annually for that extra million dollars of coverage.

How Risk Management Affects Your Rates

Your property management practices and tenant screening directly influence what insurers charge for liability. Properties with documented maintenance records and thorough tenant screening typically qualify for better rates because insurers see lower claims frequency. You should maintain maintenance logs, tenant applications, and safety inspections-these documents prove that you manage risk responsibly and can help you secure more favorable pricing when you shop for coverage.

Why Standard Homeowners Insurance Fails Multi-Unit Landlords

Homeowners insurance is written for owner-occupied properties where you live in the home. The moment tenants move in, that policy becomes nearly worthless for protecting your rental income and liability exposure. Insurers explicitly exclude rental properties from standard homeowners coverage because tenant-occupied buildings present fundamentally different risks than owner-occupied homes. A homeowners policy assumes you maintain the property to your own standards and live there daily, which changes the entire risk profile. Once you rent units out, you need a completely different contract designed for landlords managing multiple tenants and income streams.

Coverage Limits Fall Short for Multi-Unit Reconstruction

Standard homeowners policies cap coverage at levels appropriate for a single-family home you occupy yourself. If your four-unit building costs $500,000 to rebuild after a major fire, a homeowners policy might max out at $200,000 or $300,000 in dwelling coverage. You absorb the difference personally. Multi-unit landlord policies let you set coverage limits based on actual replacement cost for your specific building, accounting for the complexity of multiple units with shared systems, common areas, and higher reconstruction expenses.

The cost to rebuild a multi-unit structure substantially exceeds a single-family home because you rebuild multiple kitchens, bathrooms, electrical systems, and plumbing networks simultaneously. A homeowners policy simply does not contemplate this reality, leaving you dramatically underinsured when disaster strikes.

Liability Exposure Multiplies with Each Tenant

A single-family homeowners policy typically includes $100,000 to $300,000 in liability coverage. With a four-unit building, you have at least four separate households plus their guests, contractors, and visitors moving through your property daily. The probability of someone getting injured on your premises increases proportionally with occupancy.

If a tenant’s guest slips on ice in a common stairwell and suffers a serious injury requiring surgery and ongoing care, liability claims can easily exceed $500,000. A standard homeowners policy provides nowhere near adequate protection for this exposure. Multi-unit landlord policies recognize this multiplied risk and allow you to purchase higher liability limits that match your actual exposure, with umbrella coverage available to extend protection to $1 million or more when needed.

Personal Property Coverage Gaps in Rental Units

Homeowners insurance covers personal property belonging to the homeowner, but it explicitly excludes belongings that tenants own. Your policy will not reimburse a tenant for damaged furniture, electronics, or clothing after a fire or water damage. Tenants must carry their own renters insurance to protect their belongings. This creates a critical gap: if tenants lack renters insurance and suffer losses, they may pursue legal action against you, claiming you failed to maintain the property adequately. Multi-unit landlord policies address this by clarifying what you cover (landlord-owned furnishings and appliances) and what tenants must cover themselves, reducing ambiguity and potential disputes.

How to Move Forward with Proper Coverage

The gap between homeowners insurance and multi-unit landlord insurance is not a minor technicality-it represents the difference between financial protection and catastrophic loss. When you assess your current coverage, you need to evaluate whether your policy actually covers rental income loss, whether liability limits match your exposure across multiple units, and whether replacement cost values reflect what you’d actually spend to rebuild. An independent agent can review your existing homeowners policy and show you exactly where it fails to protect your multi-unit investment, then help you transition to a landlord policy that covers the risks you actually face.

How to Choose the Right Multi-Unit Landlord Policy

Calculate Your True Replacement Cost

Start with your actual replacement cost, not your property’s market value or what you paid for it. Contact a contractor or use online replacement cost calculation for your region and building type. For a four-unit apartment building in Washington state, you might find that reconstruction costs run $450,000 to $550,000 even if you purchased the property for $380,000. Insurers will ask detailed questions about square footage, year built, number of bathrooms, roofing material, and whether the building has a basement or crawlspace. These specifics directly drive the replacement cost calculation.

Once you have an accurate number, your dwelling coverage limit must match it. Underestimating by $50,000 or $100,000 leaves you personally responsible for that gap after a total loss. This is non-negotiable.

Document Your Property Management Practices

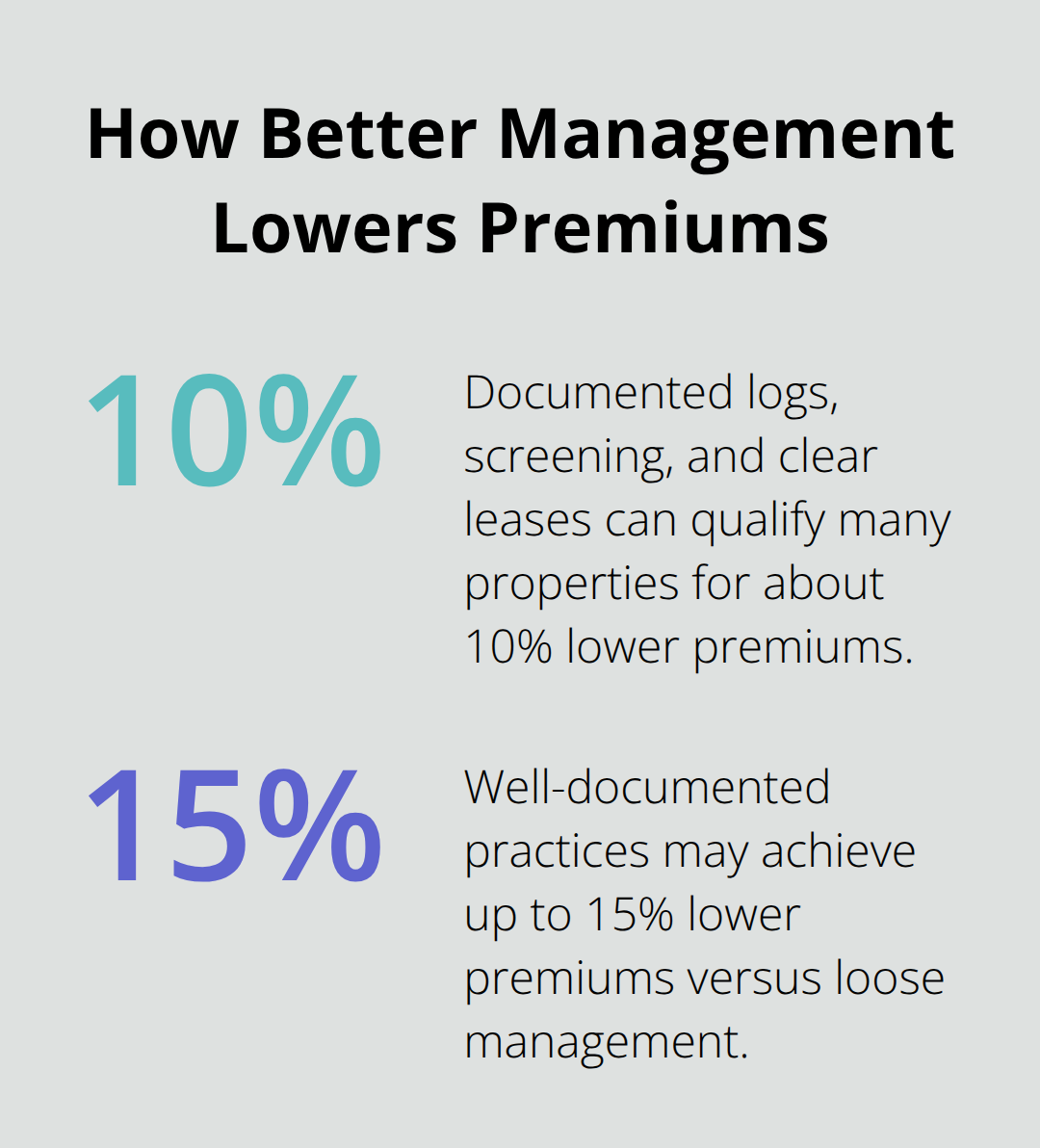

Your property management practices and tenant screening habits matter far more to insurers than most landlords realize. Carriers now review maintenance documentation, tenant application standards, and your track record of addressing repairs quickly. Properties with documented maintenance logs, background checks on tenants, and written lease agreements that specify maintenance responsibilities typically qualify for 10% to 15% lower premiums than properties with loose management practices.

Start maintaining detailed records now, including dates of inspections, repairs completed, and contractor invoices. This documentation becomes invaluable when you apply for coverage or file a claim. Insurers view landlords who select the right policy for their property type and tenant situation as significantly lower risk, which directly translates to better rates.

Compare Quotes Across Multiple Carriers

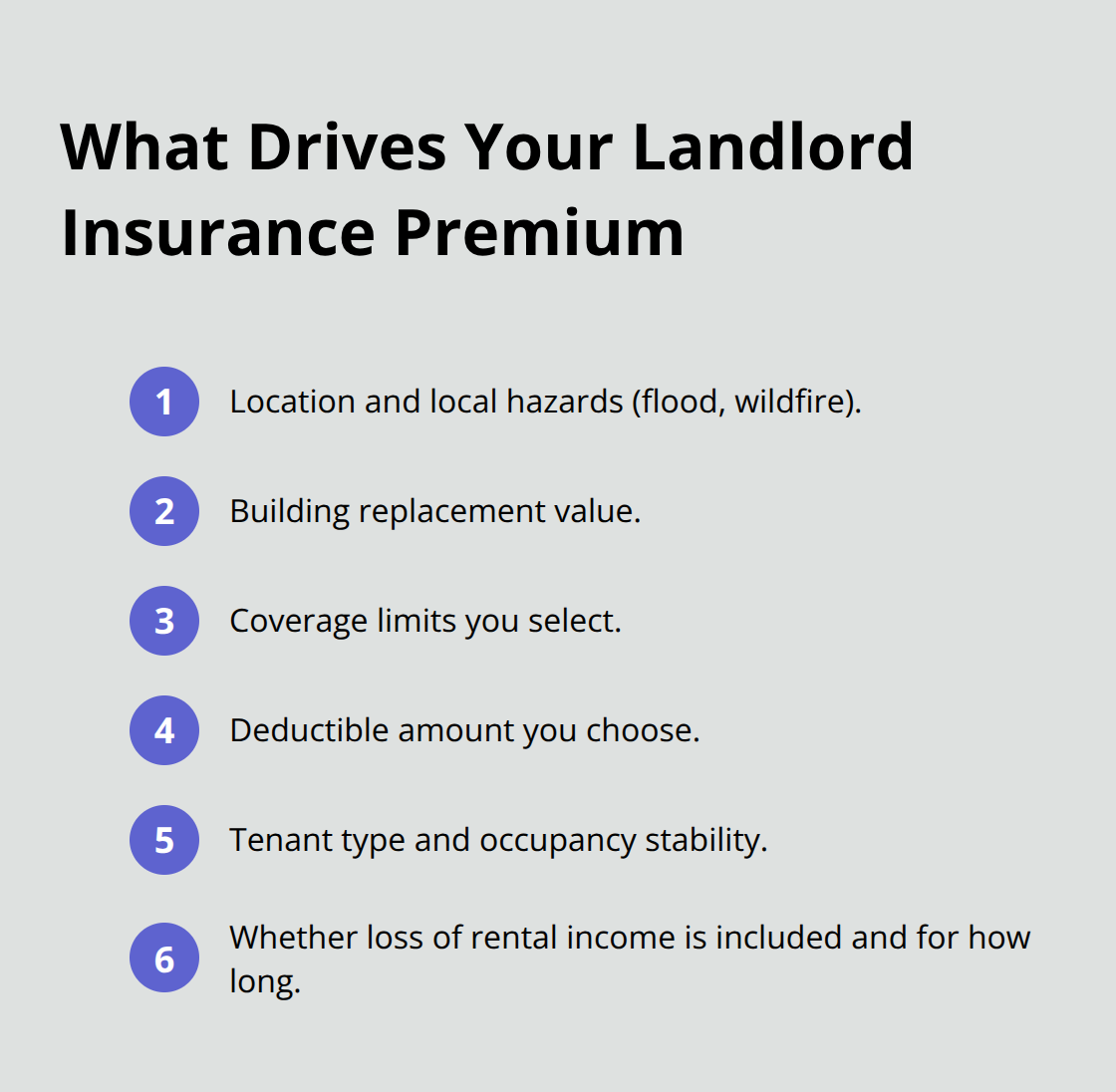

Shopping for quotes requires contacting multiple carriers directly or working with an independent broker who represents several insurers. The average landlord insurance cost sits around $1,895 annually, but your actual premium depends entirely on location, property value, coverage limits, deductible selection, and the specific tenant type occupying your units. Properties in flood-prone or wildfire-prone areas of Washington state will cost substantially more than similar buildings in lower-risk zones. A four-unit building with professional long-term tenants will cost less to insure than the same building rented to students or short-term occupants.

When you receive quotes, compare not just the annual premium but the specific coverage limits, deductibles, and whether loss of rental income is included and for how long. Some policies cover three months of lost rent; others extend to six months or more.

Select the Right Deductible for Your Situation

Deductible selection dramatically affects your premium. Choosing a $2,500 deductible instead of $500 might reduce your annual cost by $300 to $400, but you’ll pay that amount out of pocket for each claim. Evaluate whether your cash reserves can absorb a $2,500 claim without stress. An independent agent can help you choose the right policy for your situation, pulling quotes from different insurers simultaneously and explaining how each policy handles your specific risks, saving you hours of phone calls and providing transparency around why prices differ between carriers.

Final Thoughts

Multi-unit landlord policies protect your investment in ways standard homeowners insurance simply cannot. Replacement cost coverage must match your actual rebuilding expenses, liability limits must account for multiple tenants and their guests, and loss of rental income protection keeps your cash flow stable when disaster strikes. The gap between adequate coverage and inadequate coverage often means the difference between recovering financially after a loss and absorbing tens of thousands of dollars personally.

Your next step is straightforward: gather your property details, calculate accurate replacement costs, and request quotes from multiple carriers. Document your maintenance practices and tenant screening standards, as these directly influence what insurers charge. Compare not just premiums but coverage limits, deductibles, and whether loss of rental income is included for the duration you need-the average landlord insurance cost around $1,895 annually varies significantly based on location, property value, and tenant type, so shopping across carriers reveals real savings opportunities.

An independent agent transforms this process from overwhelming to manageable by pulling quotes simultaneously from multiple top carriers, explaining how each multi-unit landlord policy handles your specific risks, and identifying which deductible level makes sense for your cash reserves. Contact H&K Insurance Agency to review your current coverage and discover how proper protection accounts for local flood and wildfire risks in the Puget Sound region, helping you avoid the costly gaps that leave landlords underinsured.