Home Relocation Insurance WA: Safeguard Your Move With Flexible Coverage

Moving to Washington means protecting more than just your belongings. Weather, distance, and liability risks make home relocation insurance WA essential for anyone relocating to the state.

At H&K Insurance Agency, we help families and individuals understand what coverage actually matters for their move. The right policy can mean the difference between a smooth transition and financial loss when something goes wrong.

Why Washington Moves Need Extra Protection

Washington’s relocation landscape presents three distinct challenges that standard homeowners insurance simply doesn’t address. Household goods lose coverage the moment they leave your home. Standard home contents insurance stops protecting your belongings during transit, creating a dangerous gap that most people don’t realize exists until damage occurs. A $50,000 household inventory crossing Washington state or arriving from out of state sits completely unprotected unless you secure transit insurance. This isn’t theoretical-it’s a real liability that affects every move into or within the state.

Weather and Distance Compound Your Risk

Washington’s Puget Sound region presents specific environmental hazards that increase damage probability during moves. Extreme weather patterns, including heavy rain, wind, and occasional heat waves, expose your belongings to moisture damage and temperature fluctuations during loading, transport, and unloading. Long-distance relocations to Washington compound this exposure significantly. A move from California or the East Coast means your goods spend days exposed to changing conditions across multiple states. Professional movers reduce this risk through climate-controlled transport and proper packing, but basic removalist liability-the free coverage movers provide-typically caps at only $100–$200 per item or $1,000–$2,000 per kilogram. That means a damaged 50-pound television valued at $1,500 would only pay $30 under released value protection. Full replacement cost coverage, which actually protects your belongings at current market value, costs roughly 1–2% of your declared shipment value. For a $50,000 move, expect about $500–$1,000 in transit insurance premiums.

Liability Gaps Leave You Exposed

The legal minimum coverage movers carry protects them, not you. If a mover damages your furniture during loading or an accident occurs during transport, the mover’s liability insurance has strict limits and exclusions. High-value items require written declarations before moving day, and failure to declare items properly can result in significant underpayment. Self-packed boxes face even stricter limitations, often capped at around $100 per carton regardless of actual contents.

Washington relocations also involve unique risks: multiple loading and unloading points increase damage probability, and the state’s varied terrain means potential for delays or complications. Most households contain $40,000–$100,000 in goods, yet many people underestimate this amount when declaring value to movers. You should walk through your home, photograph belongings, and assign realistic replacement costs-not depreciated values. This step directly influences your coverage adequacy and claim outcomes if something goes wrong.

What Separates Basic Coverage From Real Protection

Separating basic removalist liability from optional transit insurance matters more than most people realize. The mover’s free liability covers minimal scenarios and excludes weather damage, self-packed box damage, and items you fail to declare. Optional transit insurance fills these gaps and covers your belongings at replacement cost rather than depreciated value. Third-party moving insurance can supplement mover coverage, usually costing about 1–5% of your shipment value and covering scenarios the mover’s policy doesn’t address.

Understanding these distinctions helps you make informed decisions about what protection your household actually needs. The next section walks through the specific coverage options available for Washington relocations and how to evaluate which combination works best for your situation.

Your Coverage Options for Washington Moves

Full Replacement Cost Protects Your Actual Investment

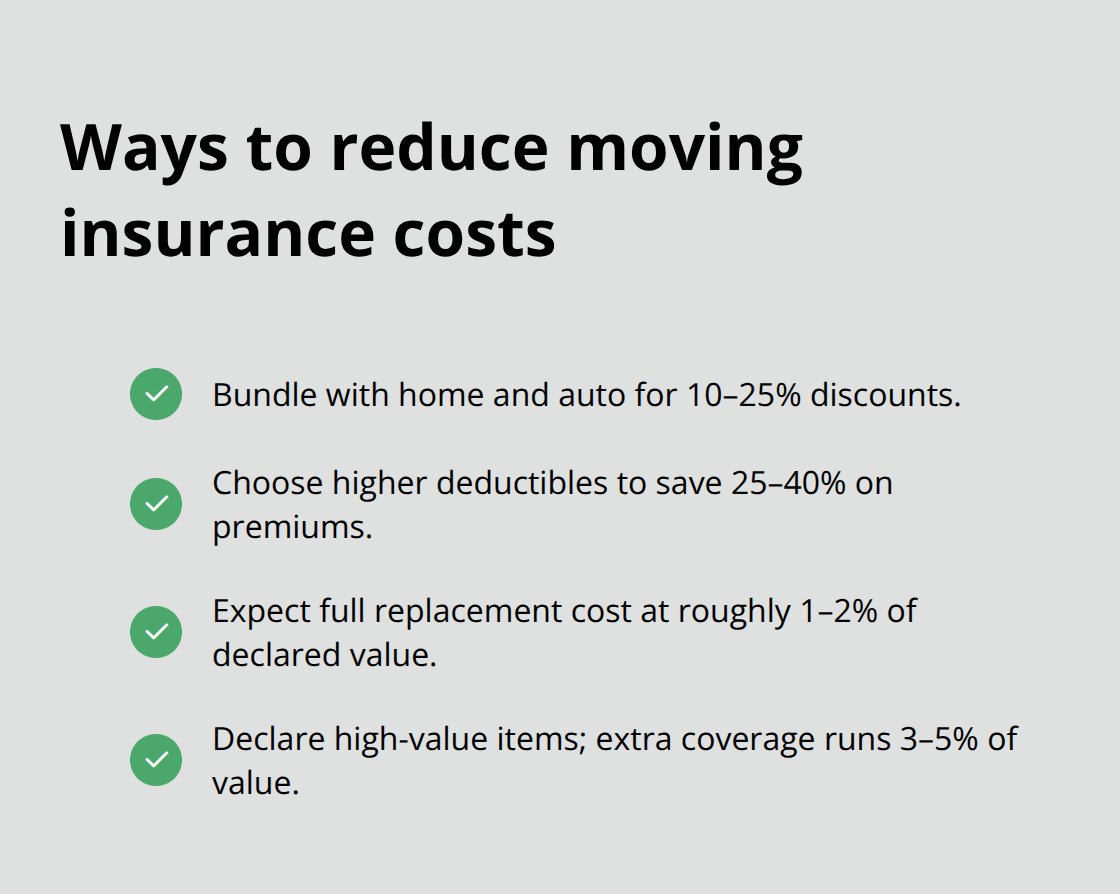

Full replacement cost coverage and actual cash value represent fundamentally different approaches to protecting your belongings, and full replacement cost stands as the superior choice for Washington relocations. Full replacement cost pays what it actually costs to replace damaged items at today’s prices, while actual cash value deducts depreciation, leaving you significantly undercompensated. A five-year-old couch worth $2,000 new might only pay $600 under actual cash value, forcing you to absorb the $1,400 difference yourself. For Washington moves where a $50,000 household inventory is common, this depreciation penalty across multiple items can easily cost you $10,000 or more in uncompensated losses. Full replacement cost typically costs 1–2% of your declared shipment value, making it roughly $500–$1,000 for that $50,000 move. This modest premium translates to genuine protection rather than financial disappointment after damage occurs.

High-Value Items Require Written Declaration

High-value items demand separate attention because standard transit coverage includes per-item caps, typically ranging from $5,000 to $10,000. If you own jewelry, fine art, antiques, or electronics worth more than these thresholds, you must declare them in writing before moving day with supporting documentation like appraisals or receipts. A declared diamond ring valued at $15,000 receives full protection; the same ring without declaration might only pay $5,000 if damaged. Extra coverage for high-value items typically costs 3–5% of their declared value, so protecting that $15,000 ring might cost $450–$750.

Weather and Road Conditions Create Real Exposure

Weather damage and road condition damage receive variable treatment depending on your coverage type. Released value protection, the free mover liability, often excludes weather-related damage entirely, meaning moisture from Pacific Northwest rain or temperature swings during transport leave you unprotected. Comprehensive transit insurance covers these scenarios, protecting against the moisture damage that affects roughly 15–20% of long-distance moves according to industry experience. Road condition damage, including damage from potholes or sudden stops, gets covered under full value protection but not basic removalist liability. For Washington specifically, where you might encounter everything from I-5 traffic delays to mountain passes on eastbound moves, comprehensive coverage addresses these realistic risks.

The specific coverage combination you select directly determines what happens when damage occurs during your move. Understanding these distinctions helps you evaluate which protection your household actually needs before moving day arrives.

How to Choose the Right Moving Insurance Policy

Calculate Your Household Inventory and Its True Value

Walk through your entire home and document what you actually own. Open closets, check the garage, photograph electronics and furniture, then assign realistic replacement costs for each item at today’s prices, not what you paid five years ago. A typical family room alone-couch, chairs, entertainment system, coffee table-easily totals $5,000 to $8,000 at replacement cost.

Create a detailed spreadsheet listing room-by-room inventory with values. This exercise serves two critical purposes: it reveals your actual coverage needs and provides documentation if you need to file a claim. Without this inventory, you’ll either over-insure and waste money or under-insure and face catastrophic losses.

Match Coverage Levels to Your Declared Value

Once you know your total household value, you can calculate appropriate coverage. For a $50,000 inventory, full replacement cost coverage runs approximately $500 to $1,000 in premiums-roughly 1 to 2% of declared value. This cost directly correlates to protection level.

A $0 deductible costs more than a $500 or $1,000 deductible, but selecting higher deductibles can reduce premiums by 25 to 40% according to industry data. The math matters: if you choose a $1,000 deductible instead of $0, you might save $250 to $400 on premiums while accepting slightly more personal risk. Consider your financial situation and risk tolerance when making this decision.

Declare High-Value Items in Writing

Jewelry, fine art, antiques, collectibles, and high-end electronics typically face per-item caps under standard transit coverage. If you own items exceeding these thresholds, you must declare them in writing with supporting documentation-appraisals, receipts, photographs-before moving day. Extra coverage for high-value items costs 3 to 5% of their declared value, so protecting a $15,000 piece of jewelry costs approximately $450 to $750 in additional premiums.

Bundle Coverage With Your Existing Policies

Combining your moving coverage with your existing homeowners and auto policies through a local agent who understands Washington’s specific risks makes financial sense. Many insurers offer discounts of 10 to 25% when you bundle multiple policies, potentially offsetting moving insurance costs entirely. An agent familiar with the Puget Sound region can identify coverage gaps your current policies create during transit and recommend solutions tailored to your situation.

H&K Insurance Agency represents multiple top local and national carriers, allowing them to compare rates across providers and customize packages that protect your move while optimizing your overall insurance costs through bundling discounts and regional expertise.

Final Steps Before Your Move

Read through your coverage documents carefully and identify exactly what you’ve purchased, what gets covered, and what exclusions apply to your situation. Pay particular attention to per-item caps, deductible amounts, and whether weather damage or self-packed box damage receives coverage. Call your insurance provider with questions about scenarios that concern you-a five-minute conversation clarifies coverage details and prevents costly surprises when damage occurs.

Walk through your home with a camera and photograph every room, every piece of furniture, and valuable items from multiple angles. Capture serial numbers on electronics, condition details on antiques, and any existing damage so you can prove what condition items were in before moving day. Store this documentation separately from your belongings, either digitally in cloud storage or physically in a safe location, because concrete evidence supports your claim far better than memory or estimates.

H&K Insurance Agency represents multiple top local and national carriers, allowing them to compare rates across providers and customize home relocation insurance WA packages that protect your move while optimizing your overall insurance costs. Their team understands the Puget Sound region’s specific relocation challenges and guides you toward coverage that matches your household’s actual value and risk profile. Contact them before your move to verify your protection is complete.