Kitsap Landlord Insurance: Bundle and Protect Your Rental

Owning rental property in Kitsap County comes with real financial exposure. Standard homeowners policies won’t protect you from tenant disputes, lost rent, or liability claims specific to rental operations.

We at H&K Insurance Agency help landlords close these gaps with Kitsap landlord insurance that actually covers what matters. The right policy, combined with smart bundling, keeps your investment secure without draining your cash flow.

Why Kitsap Landlords Can’t Rely on Standard Homeowners Coverage

Tenant Liability Claims Expose You to Six-Figure Losses

Tenant disputes hit your bottom line faster than property damage ever will. A single liability claim from an injured tenant can cost $50,000 to $100,000 or more in legal fees and settlements, yet standard homeowners policies exclude rental operations entirely. Washington comparative negligence laws make this worse-you remain liable even if a tenant is partially at fault. Start with at least $500,000 in liability per occurrence for any rental property, and many landlords should consider an umbrella policy of $1 million or more to cover defense costs and damages that exceed your base policy limits.

Lost Rent Income Drains Your Cash Flow During Reconstruction

Tenants also create income risk that homeowners policies simply don’t address. If a fire, windstorm, or water damage makes your rental uninhabitable, you lose rent during the entire reconstruction period. In Kitsap County, a six-month vacancy can erase more than $13,000 in gross rent income, yet standard homeowners coverage won’t reimburse a single dollar of lost rental income. Landlord policies include loss of rent coverage that reimburses your actual lost revenue during rebuilding, which is the difference between weathering a loss and facing financial hardship.

Construction Costs Rise Faster Than Your Coverage Limits

Construction costs in Washington rose about 15% from 2020 to 2023, and Seattle-area rebuilding costs now run roughly $350 to $500 per square foot. That means a 1,500-square-foot rental could cost $525,000 to $750,000 to rebuild from scratch. If you insure with actual cash value instead of replacement cost value, you’ll face a massive shortfall because ACV depreciates your building’s value year after year.

Choose a DP-3 landlord policy with replacement cost value to avoid underinsuring as construction costs keep rising.

Average landlord property damage claims exceeded $9,800 in 2022, which means most claims fall within typical dwelling limits, but tail risks remain severe if you’re underinsured.

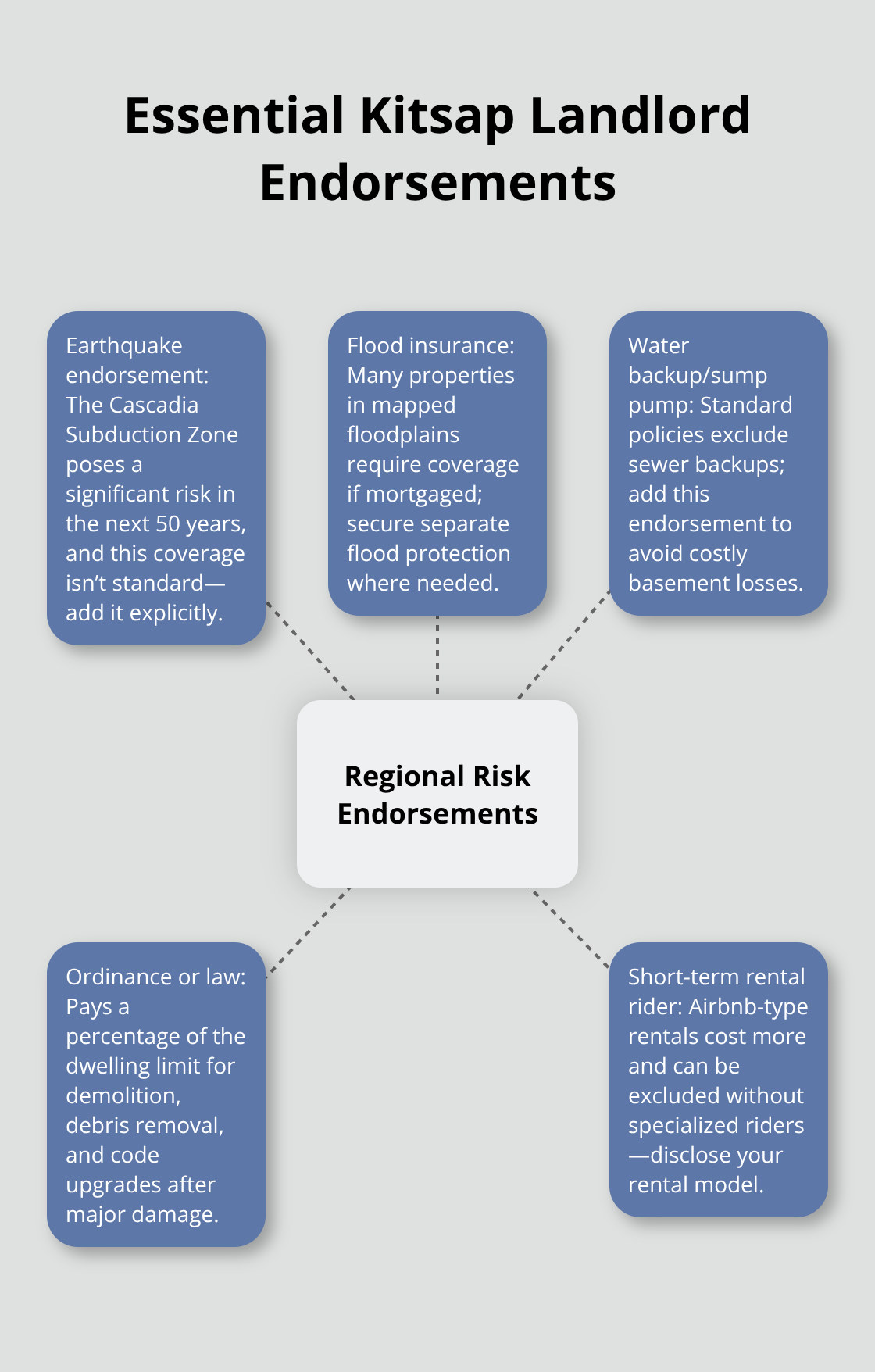

Regional Hazards Require Explicit Endorsements

Kitsap County faces unique hazards that standard policies may exclude or limit. The Cascadia Subduction Zone presents a 10–15% chance of a magnitude 9.0 earthquake within the next 50 years, and more than 175,000 structures in mapped Washington floodplains require flood coverage if mortgaged. Earthquake and flood endorsements are not standard; you must add them explicitly to your landlord policy.

Bundling these specialized coverages with your auto or home insurance often reduces total premiums by 10–20%, which makes protecting against regional risks far more affordable than most landlords expect. Understanding what your current coverage actually includes-and what it leaves exposed-is the first step toward closing these gaps.

What Landlord Insurance Actually Covers

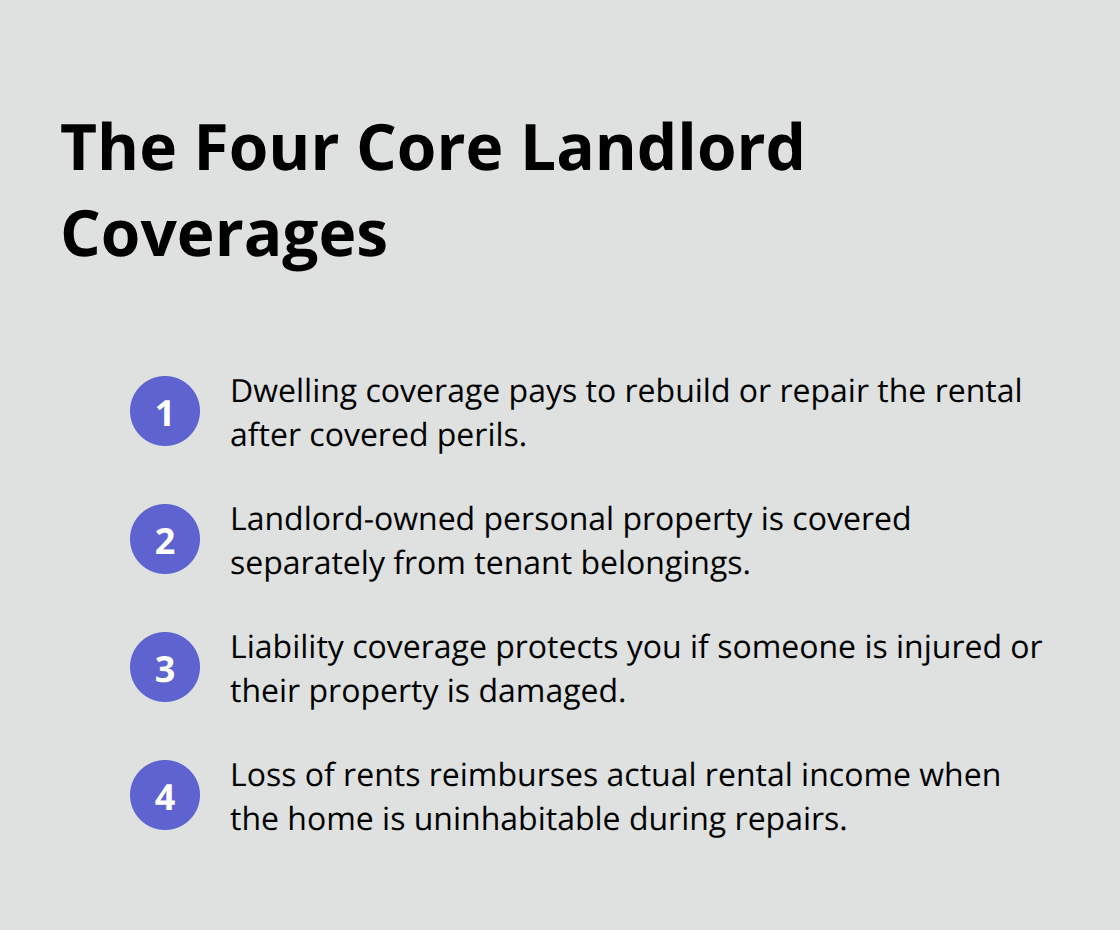

Four Core Coverage Types Protect Your Rental Investment

Landlord insurance for Kitsap County rental properties includes four core coverage types that work together to protect your investment. Dwelling coverage pays to rebuild or repair the rental structure after fire, windstorm, theft, or other covered perils. Your personal property inside the rental-furniture, appliances, and equipment you own-receives separate coverage from what tenants bring in. Liability coverage protects you when someone is injured on the property or their property is damaged, and medical payments coverage handles minor injury expenses without requiring a lawsuit. Most landlord policies also include loss of rents coverage, which reimburses your actual rental income if the property becomes uninhabitable during repairs.

Replacement Cost Value Prevents Massive Coverage Shortfalls

The critical choice you face is replacement cost value versus actual cash value. With replacement cost value, the insurer pays what it costs to rebuild today-roughly $350 to $500 per square foot in the Seattle area. With actual cash value, you get depreciated amounts that fall thousands of dollars short. For a 1,500-square-foot rental, that gap between ACV and replacement cost can exceed $100,000. Choose replacement cost value for every landlord policy in Washington to avoid underinsuring as construction costs rise.

Bundling and Deductible Strategies Cut Premiums Significantly

Bundling your landlord policy with auto, home, or umbrella coverage cuts your total insurance costs by 10–20%, and multi-policy discounts often add another 5–15% on top of that. Increasing your deductible from $1,000 to $2,500 typically saves 8–15% on your premium-but only do this if you have liquid cash reserves to cover the higher out-of-pocket costs when a claim hits. Get three quotes from different carriers using identical property details; premium differences for the same coverage can exceed 35%, so shopping matters. When comparing quotes, confirm each one specifies replacement cost value, includes minimum liability of $500,000, and covers loss of rental income for at least 12 months.

Essential Endorsements Address Kitsap County Hazards

Water backup and sump pump failure endorsements are essential in Kitsap County because standard policies exclude sewer backups, yet these losses happen regularly. Ordinance or law coverage pays 10–25% of your dwelling limit for demolition, debris removal, and code-upgrade costs during rebuilding, which becomes critical after major damage. Short-term rentals like Airbnb properties cost 20–40% more than long-term rentals, and many standard carriers exclude them without specialized riders, so disclose your rental model before purchasing.

Local Expertise Simplifies Multi-Property Management

An independent agent who understands Puget Sound regional hazards and has access to multiple top carriers can customize packages so you compare rates without the legwork. This approach saves both time and money when you manage multiple properties across King, Snohomish, or Pierce counties. Your agent should confirm that your policy covers the specific hazards your properties face-from earthquake and flood risks to tenant liability exposure-before you finalize coverage.

Common Gaps in Landlord Coverage and How to Avoid Them

Your current landlord policy might look solid until you file a claim and discover what actually isn’t covered. Standard homeowners policies reject rental claims outright, but even dedicated landlord policies have blind spots that catch owners off guard. The gap between what you think you’re insured for and what your policy actually pays can cost tens of thousands of dollars.

Standard Policies Leave Rental Operations Unprotected

Most landlords in Kitsap County don’t realize their coverage falls short until a sewer backup floods the basement, a tenant gets injured, or they face code-upgrade costs after a fire. These aren’t rare edge cases-they’re common scenarios that standard landlord policies routinely exclude unless you add specific endorsements. Water backup coverage costs just a few dollars monthly but prevents five-figure losses from drain or sump pump failures. Flood insurance through the National Flood Insurance Program runs $900 to over $4,000 annually depending on elevation and foundation type, yet many mortgaged properties in Washington floodplains legally require it.

Regional Hazards Demand Explicit Coverage

Earthquake coverage is optional but prudent given the Cascadia Subduction Zone‘s risk in the next 50 years. Short-term rentals like Airbnb properties face 20–40% higher premiums than long-term rentals and get excluded entirely without specialized riders, so misrepresenting your rental type voids coverage when claims hit. Ordinance or law endorsements pay 10–25% of your dwelling limit for code-upgrade costs during rebuilding, which becomes critical in older Kitsap neighborhoods where modern building codes demand expensive improvements after major damage.

Premium Variations Across Carriers Exceed 35 Percent

Shopping for quotes reveals how dramatically premiums vary for identical coverage across carriers-differences often exceed 35%, which means getting three quotes from different carriers isn’t optional, it’s essential. When comparing quotes, confirm each specifies replacement cost value rather than actual cash value, includes at least $500,000 in liability per occurrence, and covers loss of rental income for a minimum of 12 months.

Local Agents Identify Gaps Faster Than Solo Shopping

An independent agent with access to multiple carriers and deep knowledge of Puget Sound hazards can identify coverage gaps faster than you’ll spot them alone. Your agent should walk you through exactly what your policy covers and what it leaves exposed before you sign, because discovering gaps after a loss costs far more than spending an hour upfront reviewing endorsements and limits. Bundling with auto or home insurance cuts total premiums by 10–20% while addressing regional risks-earthquake, flood, water backup, and tenant liability exposure-that standard policies routinely miss.

Final Thoughts

Protecting your Kitsap landlord insurance investment requires three core actions: select replacement cost value over actual cash value, bundle your policy with auto or home coverage to cut premiums by 10–20%, and add regional endorsements for earthquake, flood, and water backup risks. Premium differences for identical coverage exceed 35% across carriers, so obtaining three quotes from different insurers using the same property details prevents you from overpaying by thousands of dollars annually. Most landlords spot coverage gaps only after filing a claim, which costs far more than spending an hour upfront to review what your policy actually covers.

Your policy should include at least $500,000 in liability per occurrence, loss of rental income coverage for a minimum of 12 months, and explicit endorsements addressing local hazards (especially if you manage multiple properties across King, Snohomish, or Pierce counties). Confirm your quotes specify replacement cost value, verify loss of rental income limits, and ask about bundling discounts before finalizing any policy. Each location faces different earthquake and flood risk profiles that affect both coverage needs and pricing.

We at H&K Insurance Agency represent multiple top carriers and customize packages so you compare rates without the legwork. Our team understands Puget Sound regional hazards and identifies coverage gaps faster than solo shopping ever will. Contact H&K Insurance Agency today to review your current coverage, get competitive quotes, and build a landlord policy that protects your rental income and property investment.