Marina Boat Coverage Kitsap: The Right Policy for Waterfront Access

Owning a boat slip or mooring in Kitsap County comes with unique risks that standard boat insurance simply doesn’t cover. Marina boat coverage in Kitsap protects your waterfront investment against local hazards, from Puget Sound storms to dock damage.

We at H&K Insurance Agency help boat owners navigate these specialized policies to find the right protection for their needs. This guide walks you through what marina coverage includes and how to choose the best policy for your situation.

What Marina Boat Coverage Actually Protects

Care, Custody, and Control Liability

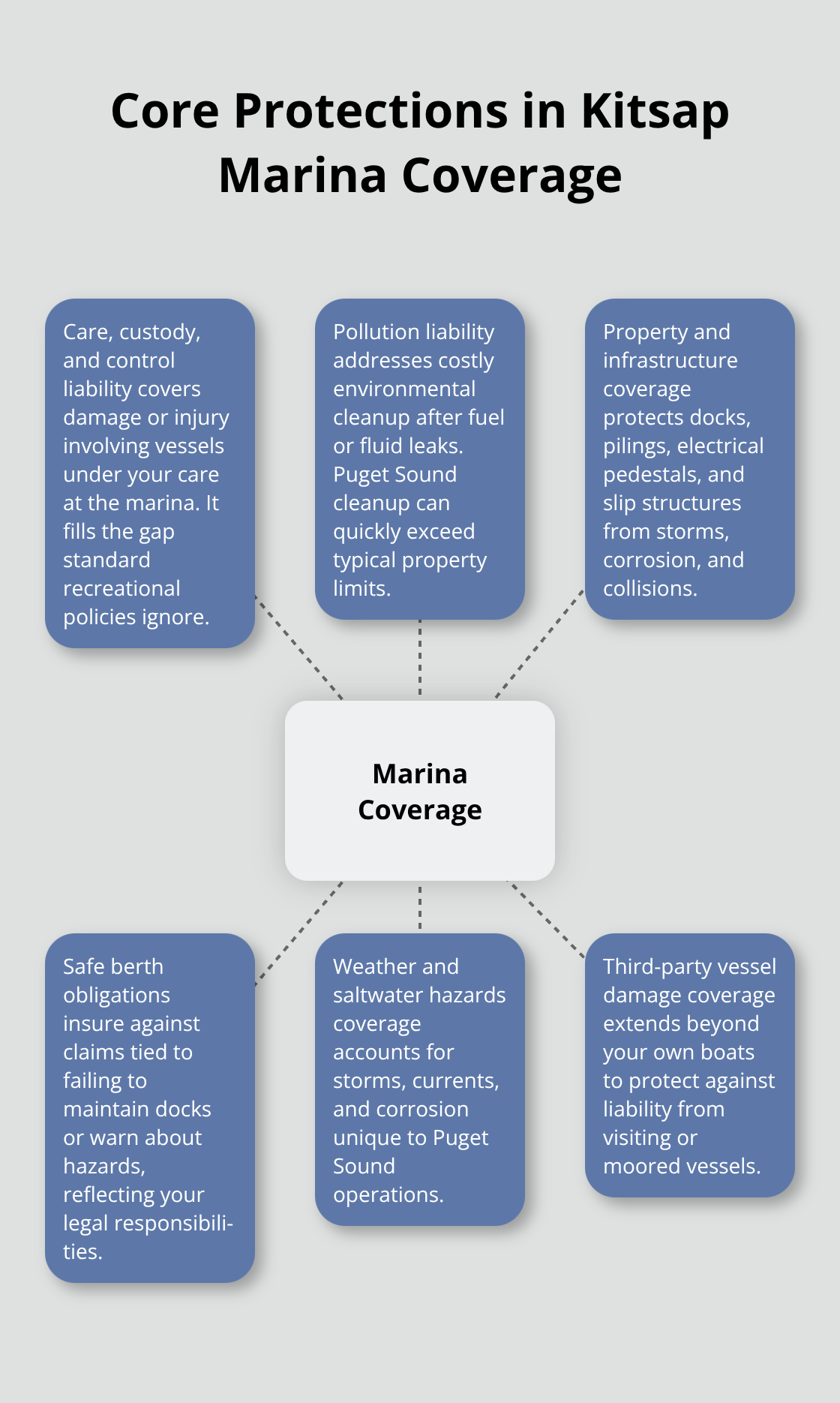

Marina boat coverage in Kitsap County protects against exposures that standard recreational boat policies simply ignore. The core protection is care, custody, and control liability, which covers you when a vessel under your care at the marina sustains damage or causes injury. If a boat sinks at your slip due to a dock defect, hull coverage pays for damage and salvage costs. However, environmental cleanup in Puget Sound can exceed $50,000, and some policies exclude pollution liability entirely, leaving you exposed to devastating costs.

Safe Berth Obligations and Legal Responsibility

Marina coverage addresses safe berth obligations, which means you hold legal responsibility for maintaining docks and warning boat owners about hazards. If someone suffers injury because you failed to disclose a hazard or maintain unsafe conditions, liability claims follow quickly. Standard boat insurance covers the boat itself, not the marina operator’s legal responsibility for vessels in your care or the property exposures of running a waterfront facility. This gap is why Kitsap marina owners who rely on a basic boat policy face significant financial risk.

Puget Sound’s Unique Environmental Risks

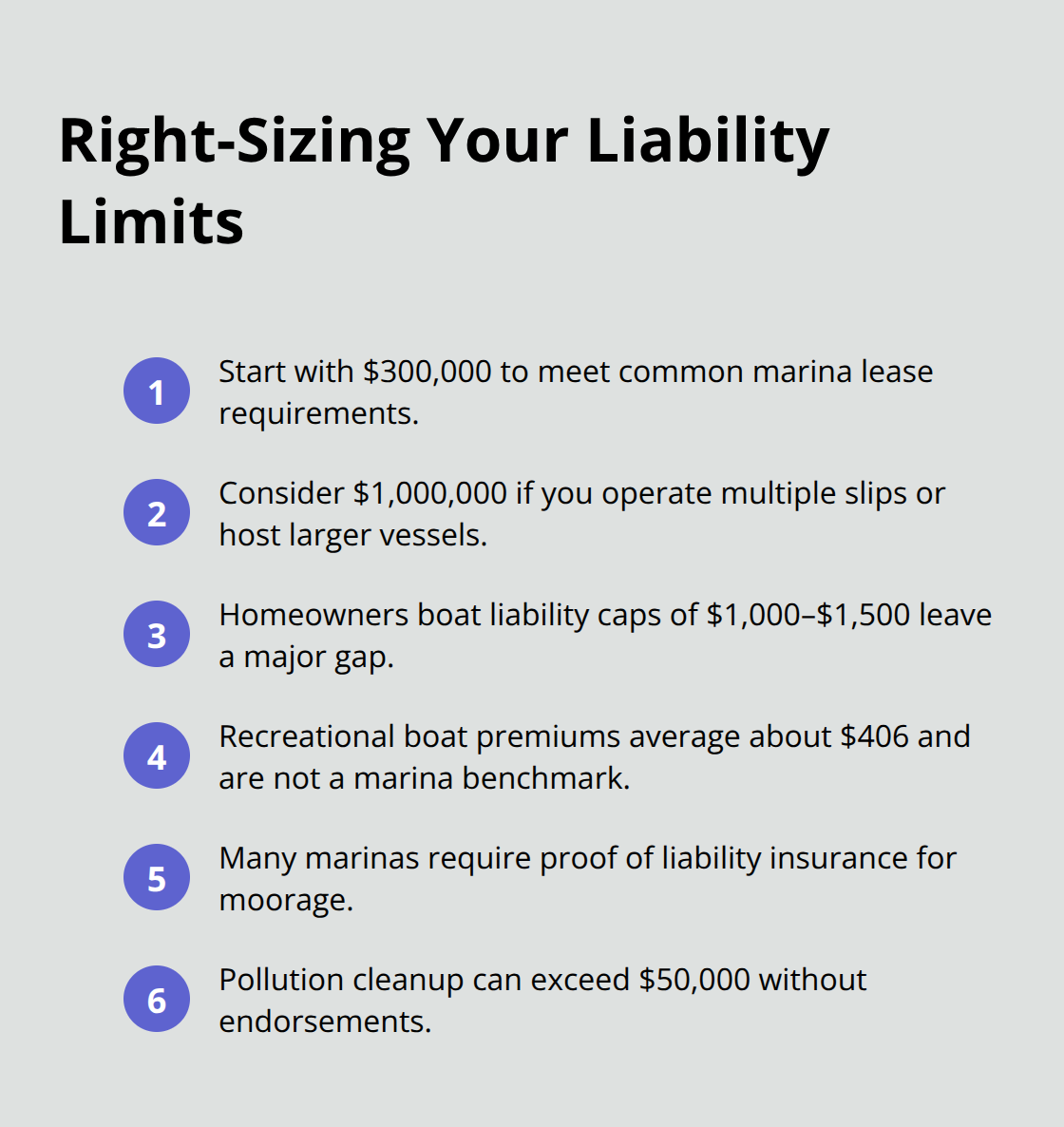

Kitsap’s waterfront environment amplifies these risks beyond what typical recreational boaters encounter. Puget Sound’s strong currents, heavy shipping traffic, unpredictable weather, and saltwater exposure create conditions where accidents and damage occur more frequently than in calm, protected waters. Bremerton-area marinas commonly require proof of liability insurance for moorage, with many demanding at least $500,000 per occurrence coverage. Your homeowners policy won’t help-it typically excludes boats or caps boat liability around $1,000 to $1,500, making a dedicated marina policy non-negotiable.

Why Specialized Underwriting Matters

The combination of Puget Sound hazards, regulatory requirements from local marinas, and the legal obligation to maintain safe berths means that marina operators need specialized underwriting that accounts for saltwater corrosion, frequent weather events, and third-party vessel damage. An independent agency representing multiple carriers can structure coverage that reflects the actual risks of operating waterfront property in the Puget Sound region. This approach ensures your policy covers both land-based facilities and waterborne exposures, not just the docking area itself.

How Much Liability Coverage Does Your Marina Actually Need

Starting with the Right Liability Limits

Liability protection forms the backbone of any marina policy, and the numbers matter far more than most Kitsap operators realize. Bremerton-area marinas commonly require at least $300,000 per occurrence in liability coverage before they’ll grant you a slip, yet many boat owners mistakenly assume their homeowners policy handles waterfront exposures. Standard homeowners policies cap boat liability at roughly $1,000 to $1,500, creating a catastrophic gap when someone gets injured at your dock or a visiting vessel sustains damage under your care. If a guest slips on a wet dock and requires hospitalization, or another boater’s $200,000 cabin cruiser collides with your moorings due to negligent maintenance, that $1,500 homeowners limit evaporates instantly.

Understanding Your True Exposure

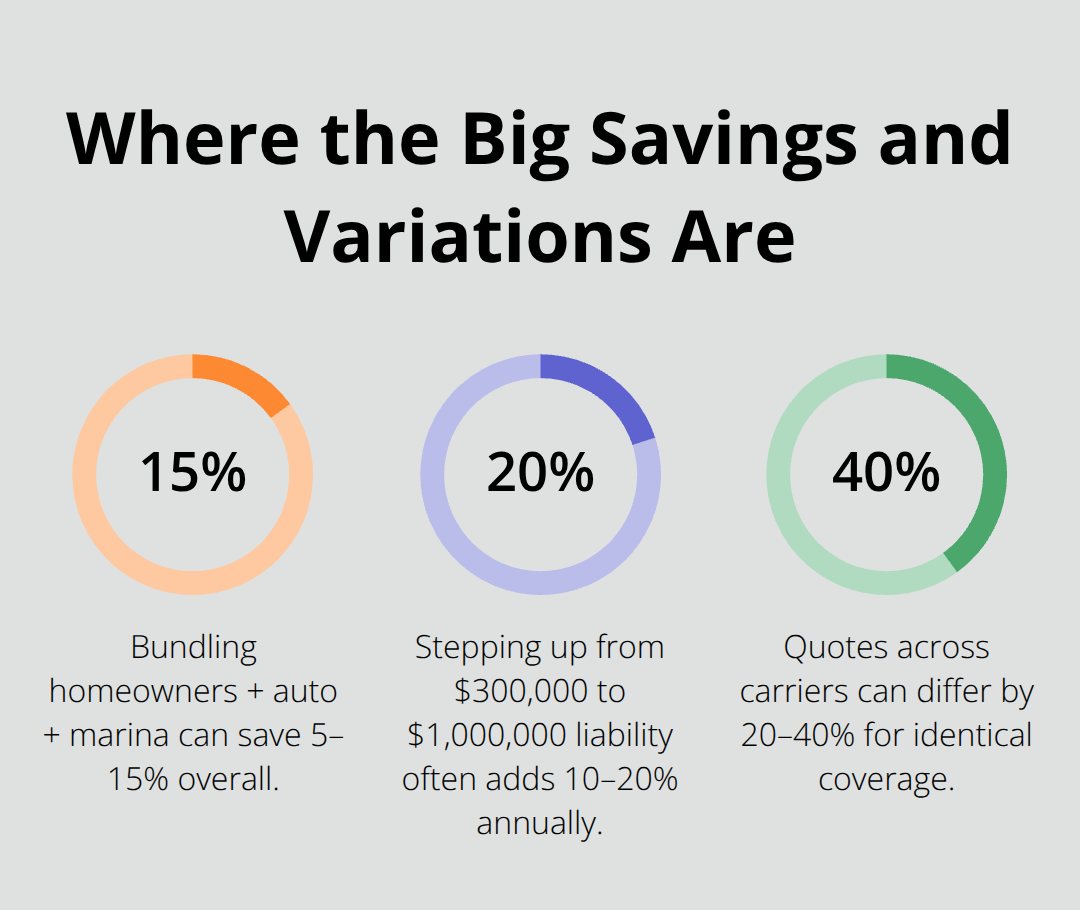

Marina operators face third-party liability that recreational boaters never encounter. Progressive data shows average boat insurance runs around $406 yearly for recreational vessels, but marina operators need specialized underwriting that accounts for third-party exposure, which costs more but protects your actual liability risk. Start with $300,000 minimum coverage to satisfy marina lease requirements, but strongly consider $1,000,000 if you operate a facility with multiple slips or regularly host larger vessels. The cost difference between $300,000 and $1,000,000 coverage typically runs 10–20% annually, a small premium relative to the financial devastation a serious injury claim can inflict.

Protecting Your Physical Property and Infrastructure

Your physical property exposures demand equally specific attention because docks, pilings, electrical pedestals, fuel systems, and slip infrastructure represent substantial assets that standard recreational policies ignore entirely. Hull coverage for vessels in your care protects against damage from weather, collision, or sinking, but environmental liability stands apart as a silent killer in Puget Sound operations. If a boat sinks at your marina and leaks fuel or hydraulic fluid, cleanup costs can exceed $50,000 without pollution liability endorsements, and many standard policies exclude this coverage entirely.

Accounting for Saltwater Corrosion and Weather Damage

Saltwater corrosion accelerates damage to dock structures and electrical systems, with typical repair costs for pilings running $3,000–$8,000 and weather-related damage to covered slips adding thousands more during winter storms. An independent agent representing multiple carriers can structure coverage that addresses both land-based exposures like dock maintenance and waterborne risks specific to Puget Sound’s harsh environment. Verify your policy covers docks, slips, and moorings explicitly rather than assuming general property protection applies, and confirm that pollution liability and environmental cleanup costs are included.

Maximizing Savings Through Strategic Bundling

Bundling marina coverage with your homeowners or auto policies typically yields 5–15% savings overall, making it worth consolidating your insurance at one agency that understands Kitsap’s waterfront operations. H&K Insurance Agency, a locally owned independent agency in Bremerton, represents multiple top carriers and can compare rates to customize packages that bundle marina coverage with your other policies. This approach ensures you capture available discounts while securing the specialized underwriting that marina operations demand in the Puget Sound region.

Why Multiple Carriers Matter for Marina Coverage

The Carrier Comparison Advantage

Kitsap marina operators make a critical mistake when they assume one insurance company can handle all their waterfront exposures. Marina coverage requires specialized underwriting that accounts for care, custody, and control liability, pollution exposure, dock infrastructure, and Puget Sound’s saltwater hazards-yet most standard carriers either avoid marina operators entirely or force generic templates that leave dangerous gaps. An independent agency representing multiple carriers like Progressive Insurance, Safeco Insurance, Travelers Insurance, and PEMCO Insurance can compare actual quotes across different underwriting approaches, revealing rate differences of 20–40% for identical coverage levels. This matters because marina operators need both competitive pricing and the flexibility to customize coverage that addresses your specific slip count, vessel types, and facility layout.

Matching Carrier Strengths to Your Specific Needs

Some carriers excel at pollution liability endorsements while others offer superior rates on property damage to docks and pilings. Shopping across multiple carriers prevents you from overpaying for coverage you don’t need while missing critical protections you do. An independent agent can structure a package where one carrier handles your marina operator’s liability while another provides superior property coverage for your dock infrastructure.

Bundling for Maximum Savings and Integration

Bundling everything with your homeowners and auto policies captures 5–15% savings across all policies. This approach eliminates the frustration of dealing with multiple agencies and ensures your marina coverage integrates cleanly with your household insurance rather than creating overlaps or gaps.

H&K Insurance Agency, a locally owned independent agency in Bremerton, represents multiple top carriers and can compare rates to customize packages that bundle marina coverage with your other policies.

Military Family Discounts and Regional Expertise

Military families in the Kitsap region often qualify for additional discounts when consolidating coverage. An independent agency representing multiple carriers can identify which companies offer the strongest military pricing while maintaining specialized marina underwriting. The reality is that no single carrier dominates marina coverage in Washington-the best protection comes from an agency with access to multiple underwriters and the expertise to match each carrier’s strengths to your specific waterfront operation.

Final Thoughts

Marina boat coverage in Kitsap protects your waterfront investment against exposures that standard recreational policies simply ignore. Care, custody, and control liability, safe berth obligations, and Puget Sound’s saltwater hazards demand specialized underwriting that accounts for the unique risks of operating a marina in the Puget Sound region. Starting with $300,000 in liability coverage satisfies most Bremerton-area marina lease requirements, but $500,000 to $1,000,000 provides realistic protection against serious injury claims or third-party vessel damage.

Your homeowners policy won’t help-it caps boat liability around $1,000 to $1,500, leaving you exposed to catastrophic financial loss. Different insurers excel at different aspects of marina coverage: some offer superior pollution liability endorsements while others provide better rates on dock and pilings protection. Bundling marina boat coverage Kitsap with your homeowners and auto policies captures 5–15% savings across all policies while ensuring your waterfront operation integrates cleanly with your household insurance.

H&K Insurance Agency, a locally owned independent agency in Bremerton, represents multiple top carriers and specializes in customized coverage for boats and waterfront properties throughout the Puget Sound region. Their team compares rates across different underwriters and structures packages that address your specific slip count, vessel types, and facility layout. Contact H&K for a free quote today.