SUV Auto Coverage Kitsap: Protecting Your Everyday Drive

SUVs dominate Kitsap County roads, but standard auto policies often miss the mark for these larger vehicles. At H&K Insurance Agency, we’ve seen firsthand how SUV owners face unique coverage challenges that put their finances at risk.

The right SUV auto coverage in Kitsap protects you from repair costs, liability exposure, and gaps that could leave you stranded. This guide walks you through the coverage options that actually work for your vehicle.

Why SUVs Cost More to Insure

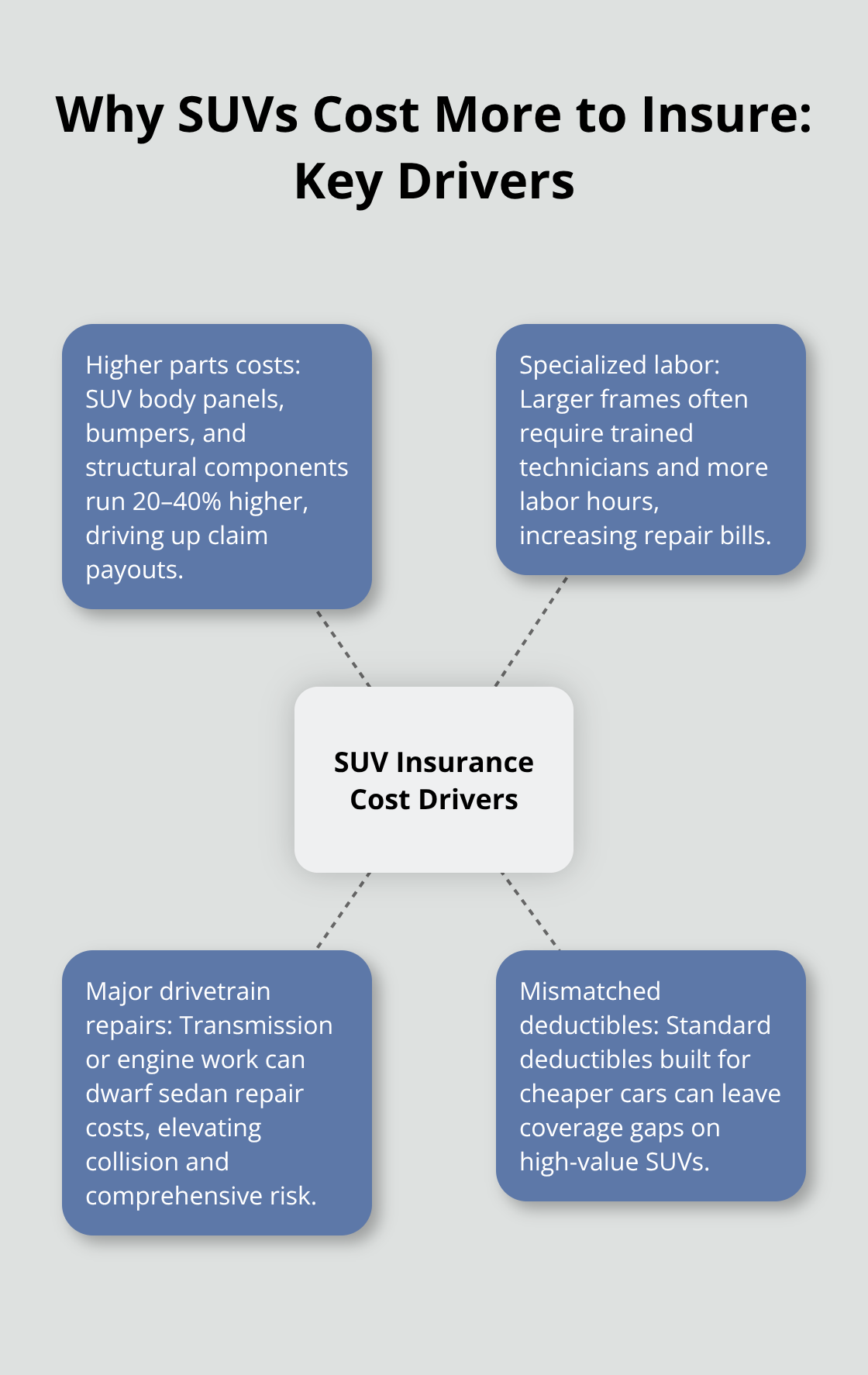

SUV repair bills hit differently than standard sedan damage. A single fender-bender on a Toyota 4Runner costs significantly more to fix than the same impact on a Honda Civic. SUV body panels, bumpers, and structural components run 20–40% higher in parts alone, and labor costs compound the problem because technicians need specialized training for larger frames. When your SUV needs a new transmission or engine work, you face repair costs that dwarf what sedan owners experience. This reality matters for your collision and comprehensive coverage limits.

Many drivers carry standard deductibles designed for cheaper vehicles, which means they’re underinsured for the actual replacement costs their SUV demands. You should review your coverage limits specifically against your vehicle’s current market value and repair history-not just the minimum your lender requires.

Liability exposure scales with your vehicle’s size

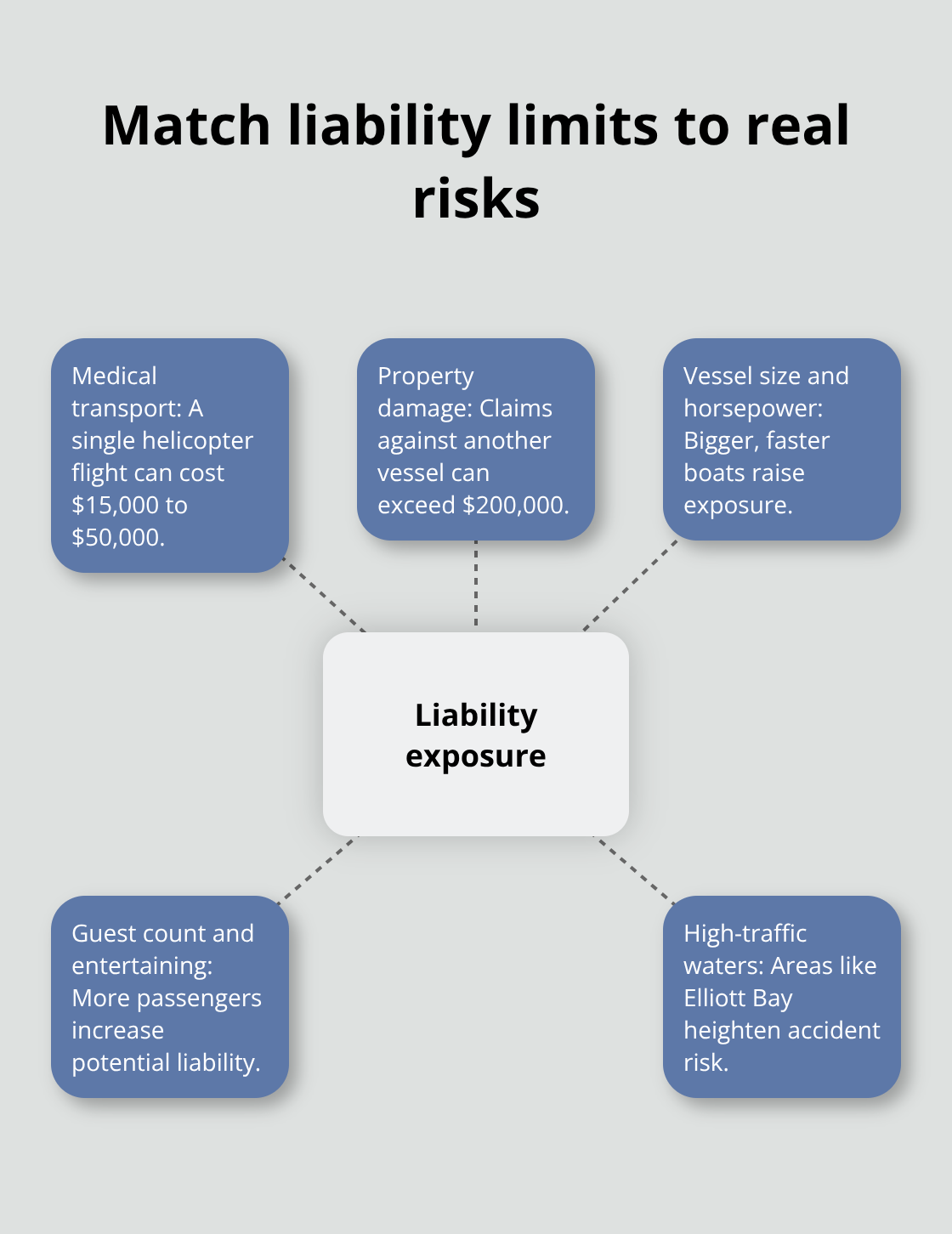

Kitsap County’s narrow roads and ferry traffic create dense driving conditions where a 5,000-pound SUV causes exponentially more damage than a 3,000-pound sedan in any collision. Washington state minimum liability coverage sits at 25/50/10, which covers $25,000 per person and $50,000 per accident in bodily injury plus $10,000 in property damage. That threshold sounds adequate until you calculate real-world medical costs-a serious injury claim easily reaches $75,000 to $150,000, leaving you personally liable for the gap. SUV owners need higher limits, and many insurance experts recommend at least 100/300/100 coverage. The gap between minimum and adequate coverage costs roughly $15–$30 monthly, a modest premium to avoid catastrophic financial exposure.

Standard policies often miss SUV-specific needs

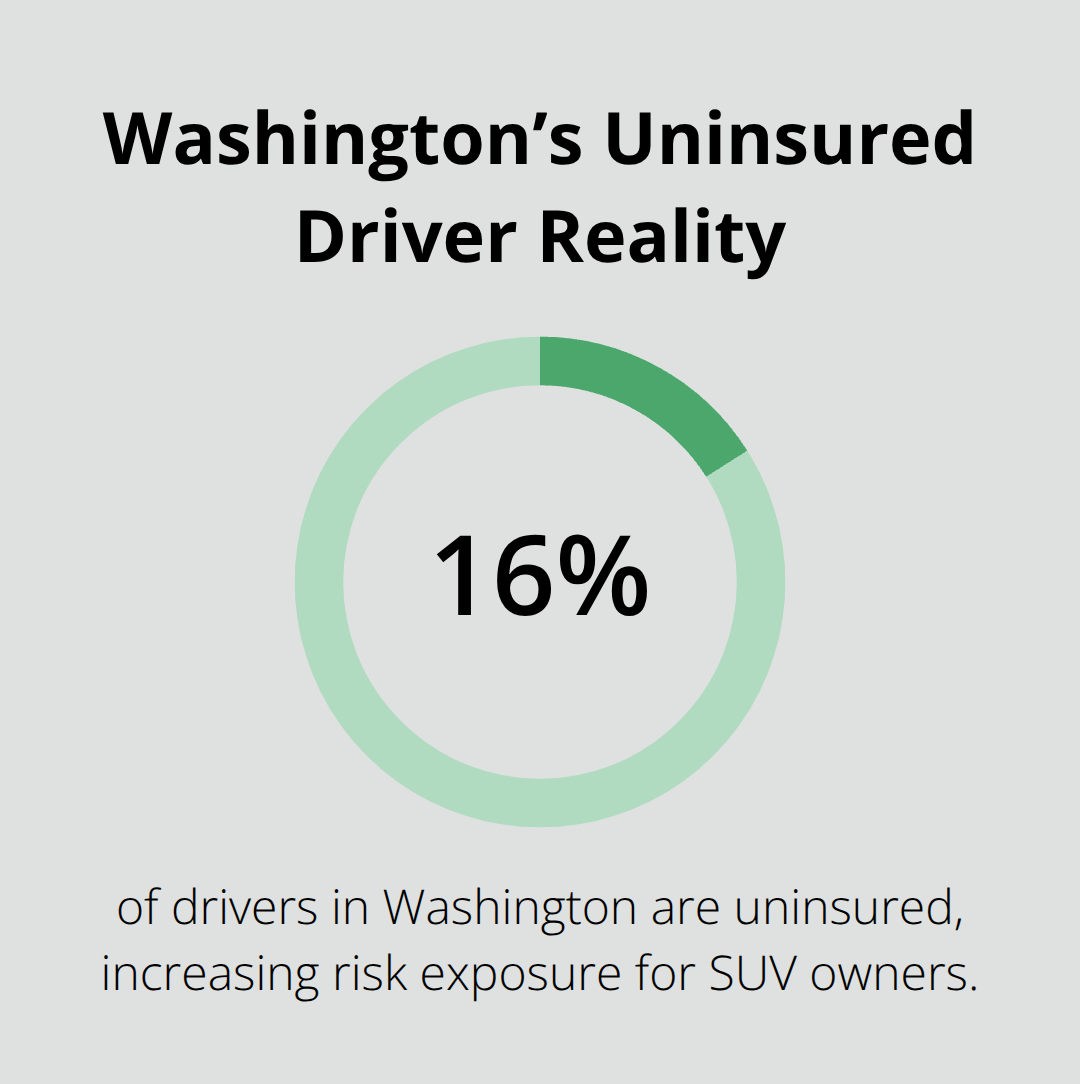

Your homeowner’s policy may not extend to off-road recreation, and your auto policy likely excludes towing expensive recreational equipment or covering damage while your SUV sits parked at a trailhead. Many Kitsap SUV owners use their vehicles for camping, hiking, or beach trips where standard liability and collision fall short. Uninsured and underinsured motorist coverage becomes critical in Washington, where roughly 16% of drivers carry no insurance. That $50–$100 annual cost for uninsured motorist protection feels expensive until an uninsured driver totals your vehicle-then it becomes the difference between a complete loss and financial ruin.

Finding the right rate for your SUV

Comparing quotes across carriers like GEICO, PEMCO, and Progressive reveals how differently insurers rate SUVs. One carrier might charge $105 monthly while another quotes $130 for identical coverage, simply because their underwriting models weight vehicle size and repair costs differently. Getting multiple quotes takes 20 minutes online and can save $300–$600 annually on SUV coverage alone. An independent agent who represents multiple carriers can layer discounts across insurers and compare rates to maximize your savings. The coverage options available to you depend heavily on which carrier you choose, which is why the next section walks through the specific protections that work best for SUVs in Kitsap County.

What Coverage Actually Protects Your SUV

Collision and Comprehensive Coverage Form Your Foundation

Comprehensive and collision coverage form the foundation of SUV protection in Kitsap County, but the specific limits matter far more than most drivers realize. Standard policies often set collision deductibles at $500, which sounds reasonable until your 4Runner needs $8,000 in frame repair and you pay $500 cash while the insurer covers the rest. The real decision is whether that $500 deductible actually reflects your financial situation. Increasing it to $1,000 typically cuts your premium by 15–25% annually, savings that compound across years. For SUV owners with stable finances, that trade-off makes sense.

The collision limit itself should match your vehicle’s actual cash value, not the minimum your lender requires. Many drivers discover their $250,000 SUV sits on a $150,000 collision limit, leaving a $100,000 gap if total loss occurs. Comprehensive coverage handles theft, weather, and animal strikes, which matter in Kitsap’s rainy climate and forested areas where deer collisions happen regularly. Washington-approved defensive driving courses cut premiums by 5–10% for three years, so completing one online course under $30 pays for itself immediately when applied to comprehensive and collision premiums.

Uninsured and Underinsured Motorist Coverage Protects Against the Unprotected

Uninsured and underinsured motorist coverage separates smart SUV owners from those gambling with their finances. Washington has roughly 16% uninsured drivers on the road, meaning one in six vehicles you encounter carries zero protection. If an uninsured driver hits your SUV, your own uninsured motorist coverage may help pay for damage and injuries up to your policy limit, typically costing $50–$100 annually for solid protection.

Underinsured motorist coverage handles the gap when a driver carries only minimum liability. Say they’re insured for 25/50/10 but cause $120,000 in damage to your SUV and injuries. Your underinsured motorist coverage bridges that gap. Skipping either feels like saving money until you’re the one filing a claim against an uninsured driver.

Recreational Use Requires Specific Coverage Endorsements

Off-road and recreational use requires honest conversation with your insurer because standard auto policies explicitly exclude damage while using your SUV for camping trips, trail driving, or towing equipment to remote locations. Some carriers offer endorsements that extend coverage to designated recreational activities, while others require separate policies. PEMCO and Progressive both recognize ferry commuting patterns in Kitsap and offer low-mileage discounts of 5–15% for drivers under 10,000 annual miles, discounts that stack with other savings like bundling auto with home coverage for 10–20% additional reduction.

The coverage options available to you depend heavily on which carrier you choose and how you use your vehicle. The next section walks through the cost-saving strategies that work best for SUVs in Kitsap County.

How to Cut SUV Insurance Costs Without Sacrificing Protection

Bundle Home and Auto for Immediate Savings

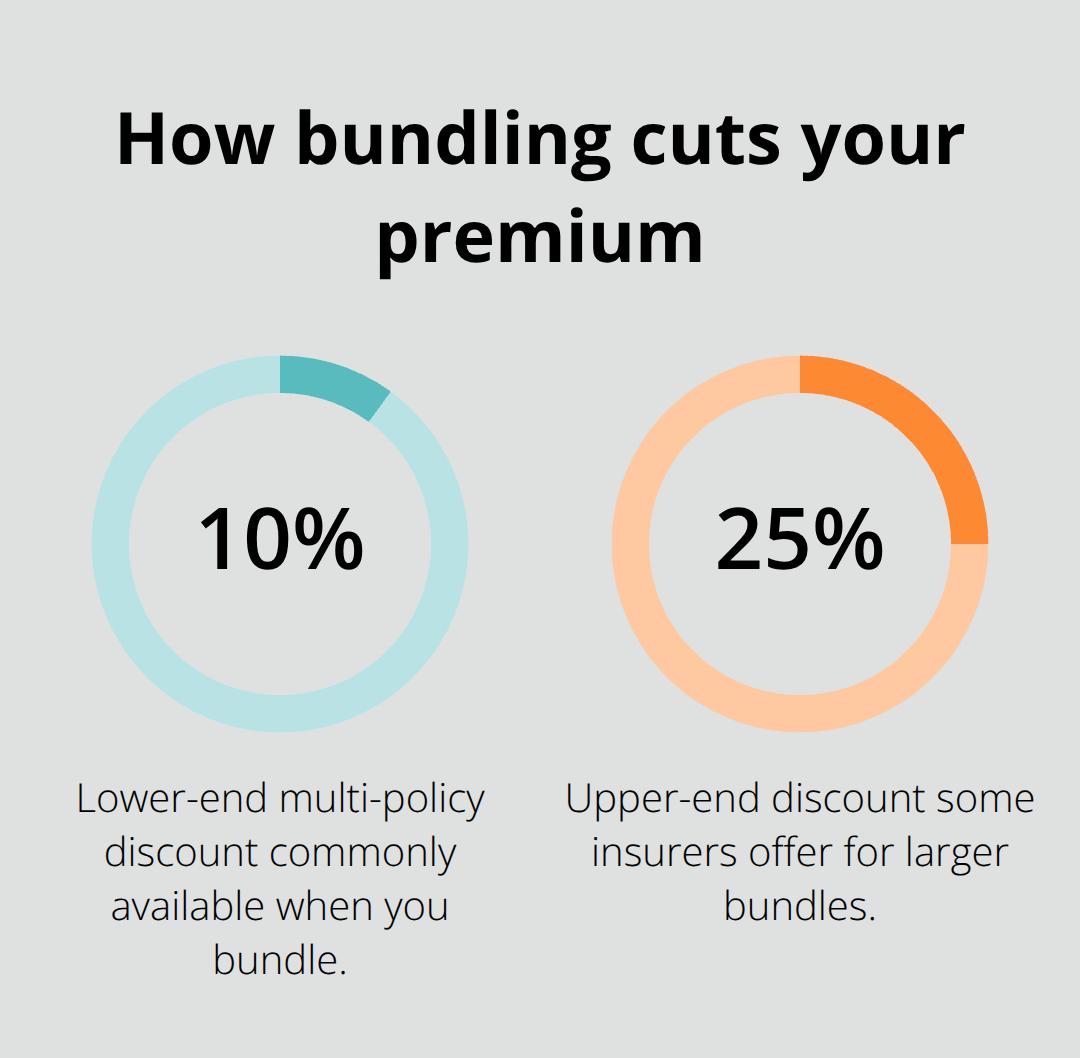

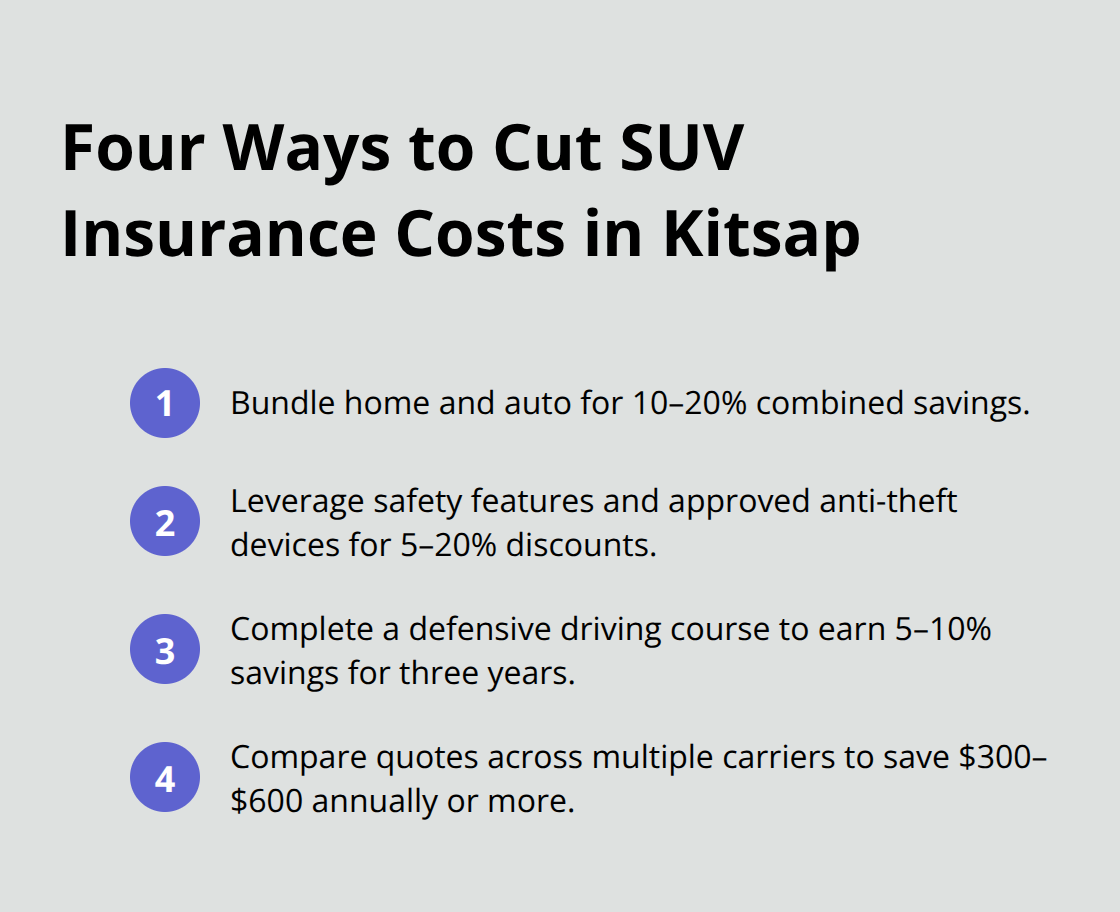

Bundling home and auto insurance cuts your overall premium, and Kitsap County carriers like PEMCO and Mutual of Enumclaw consistently offer stronger bundle rates than national competitors. The math is straightforward: if your home policy costs $1,200 annually and your SUV policy runs $1,200, bundling typically saves $240–$480 per year combined. That’s not theoretical-it’s how most Kitsap families actually reduce their insurance spend. The catch is that bundling only works if you compare actual quotes, not assume one carrier beats another. A driver paying $1,400 annually for separate auto and home policies might find bundled coverage at $1,100 with PEMCO but $1,250 with State Farm. The $150 annual difference compounds across five years into $750 in missed savings.

Leverage Safety Features and Anti-Theft Devices

Safety features on your SUV directly lower your premium because newer vehicles with automatic emergency braking, lane-keeping assist, and blind-spot monitoring receive discounts that can save hundreds of dollars annually. Installing anti-theft devices like GPS tracking or alarm systems cuts collision and comprehensive costs by 5–20%, but only if your carrier recognizes the specific device you purchase-not all systems qualify with all insurers. Before spending $400 on a tracking system, confirm whether your potential carrier accepts it and how much discount it actually provides.

Complete a Defensive Driving Course

Washington-approved defensive driving courses cost under $30 online and cut premiums by 5–10% for three years, making them the highest-return investment available. Completing one course pays for itself in the first month and keeps paying dividends for 36 months. Low-mileage discounts apply if you drive under 10,000 miles annually, which many Kitsap ferry commuters qualify for, yielding 5–15% savings with carriers like PEMCO and Progressive.

Compare Quotes Across Multiple Carriers

Getting multiple quotes takes 20 minutes and reveals the actual savings available to you. One carrier might quote $105 monthly while another quotes $130 for identical SUV coverage-that $300 annual gap exists because different insurers weight safety features, vehicle size, and repair costs differently in their underwriting models. The difference between the cheapest and most expensive quote for the same coverage in Kitsap can exceed $1,000 annually, which is why comparing quotes from at least three carriers matters more than any single discount strategy. An independent agent who represents multiple carriers can layer discounts across insurers and compare rates to maximize your savings without the legwork of contacting each company separately.

Final Thoughts

SUV auto coverage in Kitsap demands more than minimum liability and standard collision limits because your vehicle’s size and repair costs create exposure that generic policies miss. Comprehensive and collision protection with limits tied to your SUV’s actual value, uninsured motorist coverage against Kitsap’s 16% uninsured driver population, and defensive driving discounts form the foundation of smart protection. Bundling home and auto policies cuts your overall premium by 10–20%, while comparing quotes across multiple carriers reveals savings that often exceed $500 annually.

A local Kitsap insurance agent changes how you approach coverage decisions by representing multiple carriers and comparing rates without you spending hours on the phone. They understand how ferry commuting patterns qualify you for low-mileage discounts, which safety features your specific SUV model qualifies for, and whether recreational use endorsements make sense for your lifestyle. They catch coverage gaps that online quotes miss and explain why increasing your deductible or adjusting liability limits actually protects your finances better than generic recommendations.

Contact H&K Insurance Agency to review your current SUV auto coverage in Kitsap, identify which discounts apply to your driving record and vehicle, and build a plan that fits your budget without sacrificing protection. We serve the Puget Sound region as a locally owned, independent agency representing multiple top carriers. We compare rates and customize packages so you get the right protection at competitive prices.