Best Homeowners Insurance Seattle: Local Expertise Meets Strong Coverage

Seattle’s weather, earthquakes, and flooding create insurance needs that generic policies simply don’t address. Finding the best homeowners insurance in Seattle means understanding local risks and getting coverage that actually protects your home.

At H&K Insurance Agency, we’ve helped hundreds of Seattle homeowners navigate these challenges. This guide walks you through what coverage matters most and how to find a policy that fits your situation.

Why Seattle Homes Face Different Insurance Challenges

Pacific Northwest Weather and Wildfire Exposure

Seattle’s location in the Pacific Northwest creates specific insurance demands that differ sharply from other regions. Washington state experiences approximately 900 wildfires annually, with most concentrated in eastern Washington, but the risk extends westward into the Seattle area. Convective storms caused over $50 billion in losses nationally in 2025 alone, according to the Insurance Information Institute, and Seattle’s exposure to these weather patterns means your home faces real damage potential from wind, hail, and heavy precipitation. A standard homeowners policy covers fire, wind, and theft, but it explicitly excludes two critical threats in this region: earthquakes and flooding.

The Coverage Gaps That Matter Most

Earthquake damage requires a separate endorsement or standalone policy, and flooding demands either a private flood policy or coverage through the National Flood Insurance Program. These aren’t minor gaps. Many Seattle homeowners discover too late that their standard policy leaves them exposed. Flood exposure varies dramatically across Seattle’s geography. Coastal areas and properties in mapped flood zones need flood insurance, and flood policies require a 30-day waiting period before coverage activates. Earthquake coverage matters equally. The Pacific Northwest sits atop significant seismic activity, yet most homeowners skip earthquake endorsements because they seem optional.

How Seattle’s Risk Profile Affects Your Rates

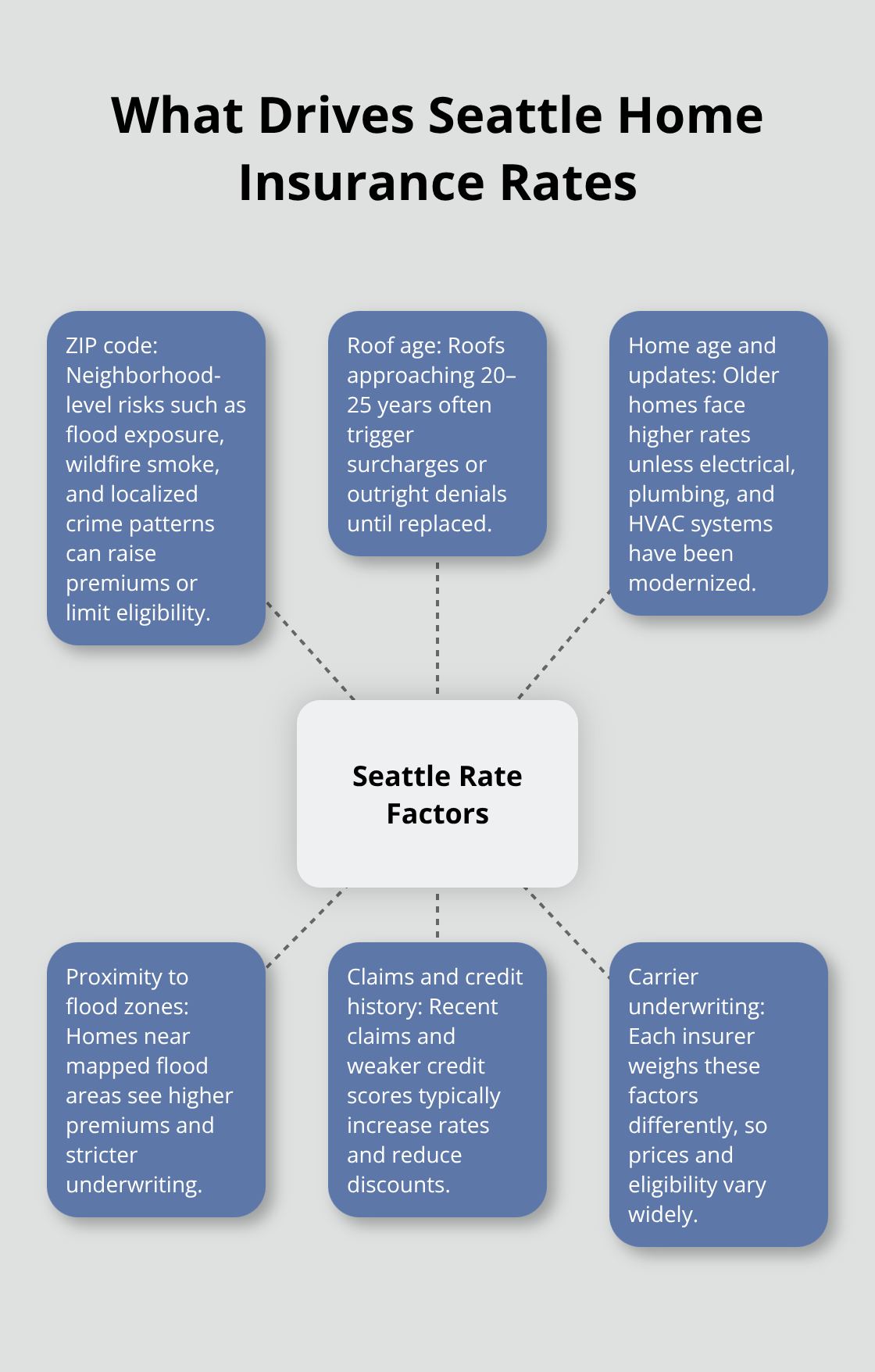

Washington state’s average premium for $300,000 in dwelling coverage sits around $1,539 annually, according to Bankrate, placing it below the national average. However, this moderate baseline doesn’t account for Seattle-specific risk factors. Your ZIP code, roof age, home construction year, and proximity to flood zones all push premiums higher or trigger underwriting denials entirely. Some carriers, including Travelers, Amica, and Nationwide, refuse to insure older homes or properties with aging roofs.

A 1914 home with a 23-year-old roof faces rejection from major carriers, even with recent electrical and plumbing updates. This isn’t theoretical-it’s happening in Seattle neighborhoods right now.

Bundling and Multi-Carrier Shopping

Bundling your home and auto policies can reduce overall costs through multi-policy discounts, but past auto claims complicate this strategy. If you filed a claim on your auto policy recently, bundling becomes less attractive from a rate perspective. Shopping directly with carriers matters more in Seattle than relying solely on aggregator quotes or independent agents with limited carrier relationships. Some insurers operate through captive agents and won’t quote through brokers. Others require bundled auto policies to insure your home. Getting quotes from PEMCO, USAA, Allstate, State Farm, and Farmers reveals how dramatically rates and eligibility vary. PEMCO averages roughly $1,550 annually for a $600,000 dwelling in Washington, while Farmers quotes around $4,216 for the same coverage. That $2,666 annual difference for identical protection shows why comparing multiple carriers matters. An independent agency can access multiple top local and national carriers, helping you compare rates and customize packages that fit your specific situation and budget.

What Coverage Actually Protects Your Seattle Home

The Six Core Components of Standard Protection

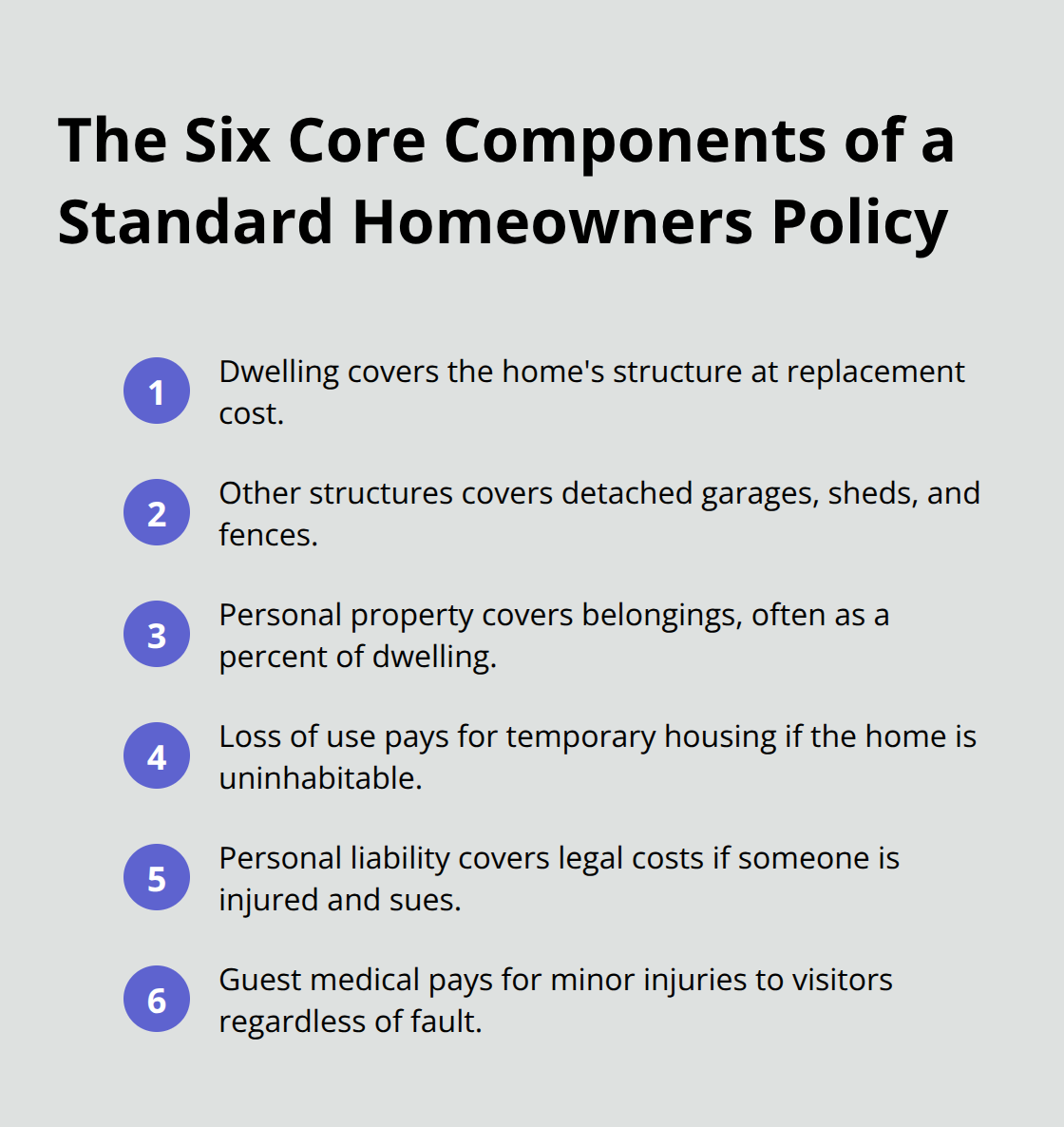

A standard homeowners policy in Washington covers dwelling, other structures, personal property, loss of use, personal liability, and guest medical payments. But standard protection leaves dangerous gaps for Seattle homeowners. You need to understand what sits inside your base policy and what requires separate purchase.

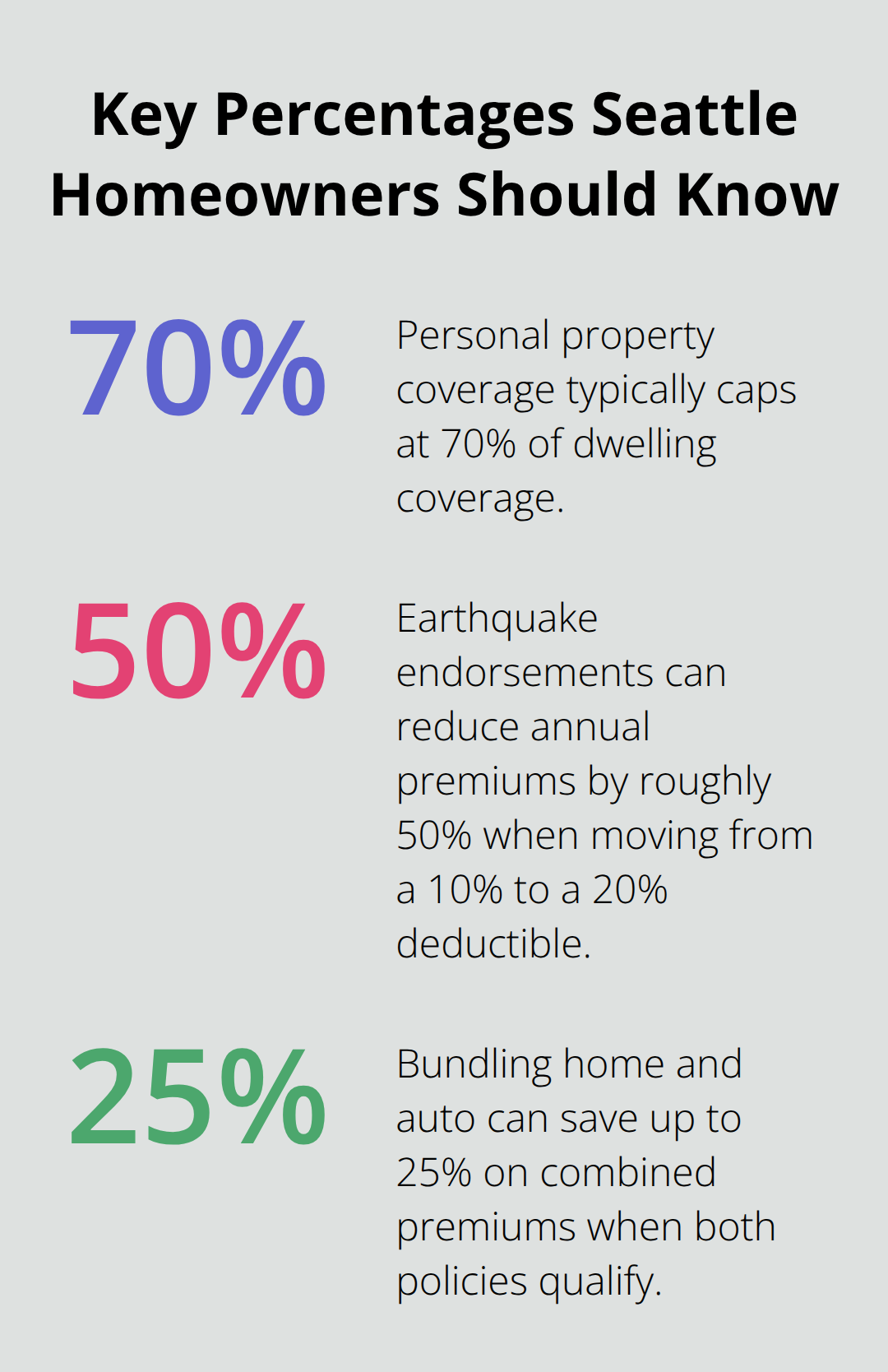

Dwelling coverage pays to rebuild your home’s structure, but it must align with actual replacement cost, not just your mortgage balance. Other structures coverage handles detached garages, sheds, or fences. Personal property coverage typically caps at 70 percent of dwelling coverage and doesn’t always include high-value items like jewelry or electronics without endorsements. Loss of use coverage pays for temporary housing if your home becomes uninhabitable. Personal liability protects you if someone is injured on your property and sues.

Critical Add-Ons for Pacific Northwest Risks

These six components form your foundation, but Seattle’s specific risks demand additions. Wildfire Response Programs, like the one USAA offers, accelerate claims processing during active fires. Inflation guard features, included by State Farm, automatically increase dwelling coverage annually to keep pace with rising construction costs. Earthquake endorsements can reduce your annual premium by roughly half when moving from a 10% to a 20% deductible, according to the Washington State Department of Insurance.

Private flood insurance or NFIP coverage fills the standard policy’s biggest exclusion. Electronic data recovery endorsements cover damage to computers and hard drives. Service line coverage protects underground utility lines on your property. These additions aren’t luxuries in the Pacific Northwest-they’re practical necessities that prevent catastrophic financial exposure.

Bundling, Deductibles, and Premium Trade-Offs

Bundling home and auto policies with the same carrier typically saves 10 to 25 percent on combined premiums, according to industry benchmarks, but this discount only works if both policies qualify at favorable rates. Recent auto claims eliminate most bundling advantages because insurers view you as higher risk across all lines. If you filed a claim within the past three to five years, shopping home and auto separately often yields better overall pricing than forcing a bundle.

Deductibles directly affect both your out-of-pocket costs and your monthly premium. A $500 deductible costs more monthly than a $1,500 deductible, but the lower deductible means less cash due when you file a claim. For Seattle homeowners, a $1,000 deductible represents a practical middle ground. It keeps monthly costs reasonable while limiting surprise expenses. Some carriers offer separate deductibles for specific perils like earthquakes or wind, meaning you might pay a $1,000 deductible for fire but a $5,000 deductible for earthquake damage.

How Seattle’s Risk Factors Shape Your Rates

Premium costs in Seattle vary dramatically by carrier. PEMCO charges approximately $1,550 annually for $600,000 in dwelling coverage, while Allstate averages around $2,012 and State Farm runs about $2,348 for identical protection. Farmers quotes roughly $4,216 for the same scenario. These aren’t minor variations-they represent decisions about which carrier actually serves your situation well.

Credit history influences premiums in most states, though California, Maryland, and Massachusetts restrict this practice. Your ZIP code within Seattle matters more than your general location. A home in a flood-prone area pays substantially more than identical property two miles away. Roof age triggers the largest underwriting decisions. Roofs older than 20 to 25 years face higher premiums or outright denial from major carriers. Home age compounds this problem. Homes built before 1950 often see premium increases or coverage restrictions unless you’ve updated electrical, plumbing, and HVAC systems within the last 15 years.

Finding Your Best Rate Match

Getting quotes from at least three carriers reveals how differently insurers price your specific risk profile and which ones will actually issue you coverage. An independent agency representing multiple top local and national carriers can help you compare rates across different underwriting standards and customize packages that fit your situation and budget.

Finding the Right Carrier for Your Seattle Home

Why National Aggregators Miss Seattle’s Real Options

Shopping for homeowners insurance in Seattle requires a fundamentally different approach than buying online through a national aggregator. The carriers that dominate national markets often don’t compete aggressively in Washington, and some refuse to insure older homes or properties with aging roofs entirely. Travelers, Amica, and Nationwide all declined coverage on a 1914 home with a 23-year-old roof in a recent Seattle scenario, even though that same home qualified for coverage elsewhere. This reality means you cannot rely on a single quote or a limited comparison.

Accessing Quotes Most Homeowners Never See

Getting quotes from PEMCO, USAA, Allstate, State Farm, and Farmers reveals the full range of your options, but only if you contact each carrier directly or work with an agency that represents all of them. Some insurers use captive agents who won’t quote through brokers, while others require bundled auto policies to insure your home at all. Pemco requires bundling, for example, which eliminates it as an option if your auto claim history makes bundling financially unfeasible. An independent agency representing multiple top local and national carriers can access quotes you simply cannot get on your own, saving you hours of phone calls while revealing carriers willing to insure your specific property.

This matters because the rate spread is enormous. PEMCO averages $1,550 annually for $600,000 in dwelling coverage in Washington, while Farmers quotes around $4,216 for identical protection. That $2,666 difference represents real money in your pocket, and it only appears when you compare multiple carriers.

Matching Your Risk Profile to the Right Underwriter

Your ZIP code, roof age, home construction year, and claim history all push individual quotes in different directions, which means customizing coverage requires matching your specific risk profile to a carrier’s underwriting standards rather than chasing the lowest advertised rate. A home built in 1914 with electrical updates in 2005, copper plumbing, and a 23-year-old roof may qualify for coverage from State Farm at $2,348 annually but face denial from Amica entirely. Credit history influences premiums in most states, though California, Maryland, and Massachusetts prohibit this practice.

Deductibles and Their Impact on Your Costs

Deductible selection directly shapes your monthly cost. A $500 deductible costs more monthly than a $1,500 deductible, but the lower deductible limits your out-of-pocket expense when filing a claim. For Seattle homeowners, a $1,000 deductible typically balances affordability with reasonable claim costs. Some carriers offer separate deductibles for specific perils, meaning your earthquake deductible might be $5,000 while your fire deductible sits at $1,000.

Getting Competitive Quotes That Reveal Your True Options

Getting quotes from at least three carriers reveals how differently insurers price your risk and which ones will actually issue you coverage. An independent agency in the Puget Sound region can help you compare rates across different underwriting standards and customize packages that fit your situation and budget, turning the complexity of Seattle’s market into a competitive advantage for your wallet.

Final Thoughts

Seattle’s homeowners insurance market rewards those who take time to understand local risks and compare multiple carriers. The best homeowners insurance Seattle offers isn’t a single policy or company-it’s the coverage that matches your specific home, your risk profile, and your budget. Standard policies leave dangerous gaps for Pacific Northwest homeowners, and earthquakes, floods, and wildfires demand separate coverage or endorsements that generic policies simply don’t include.

Your roof age, home construction year, and ZIP code determine whether major carriers will insure you at all, let alone at competitive rates. Shopping with only one or two carriers means missing options that could save thousands annually while providing better protection. Contact at least three carriers directly or work with an independent agency to gather quotes for your exact address and situation, then compare not just price but coverage options, deductibles, and add-ons like earthquake endorsements and flood insurance.

H&K Insurance Agency serves the Puget Sound region as a locally owned independent agency representing multiple top carriers. We compare rates and customize packages so you get the right protection at competitive prices without spending hours on phone calls yourself.