Kitsap County Car Policy: What It Covers and Why It Matters

Kitsap County drivers face unique insurance challenges that standard policies often miss. Weather, military community dynamics, and local accident patterns create coverage gaps most people don’t anticipate.

We at H&K Insurance Agency help drivers build Kitsap County car policies that actually protect what matters. This guide shows you what coverage you need and how to avoid paying for protection you’ll never use.

What Coverage Kitsap Drivers Actually Need

Washington state requires a minimum of 25/50/10 liability coverage-25,000 dollars per person and 50,000 dollars per accident for bodily injury, plus 10,000 dollars for property damage. In Bremerton, you can obtain this minimum liability-only coverage for around 40 to 55 dollars per month, well below the national average of about 52 dollars per month according to Bankrate. However, this bare minimum leaves you exposed. A single at-fault accident can easily exceed 50,000 dollars in total damages, leaving you personally liable for the difference. Washington is an at-fault state, meaning the responsible driver pays for injuries and property damage, and insufficient coverage can result in wage garnishment or asset seizure. We strongly recommend moving to 100/300/100 limits (100,000 dollars per person, 300,000 dollars per accident, 100,000 dollars property damage) to protect your assets. This higher limit typically costs only 10 to 20 dollars more per month but shields you from catastrophic financial exposure.

Why Uninsured Coverage Matters Here

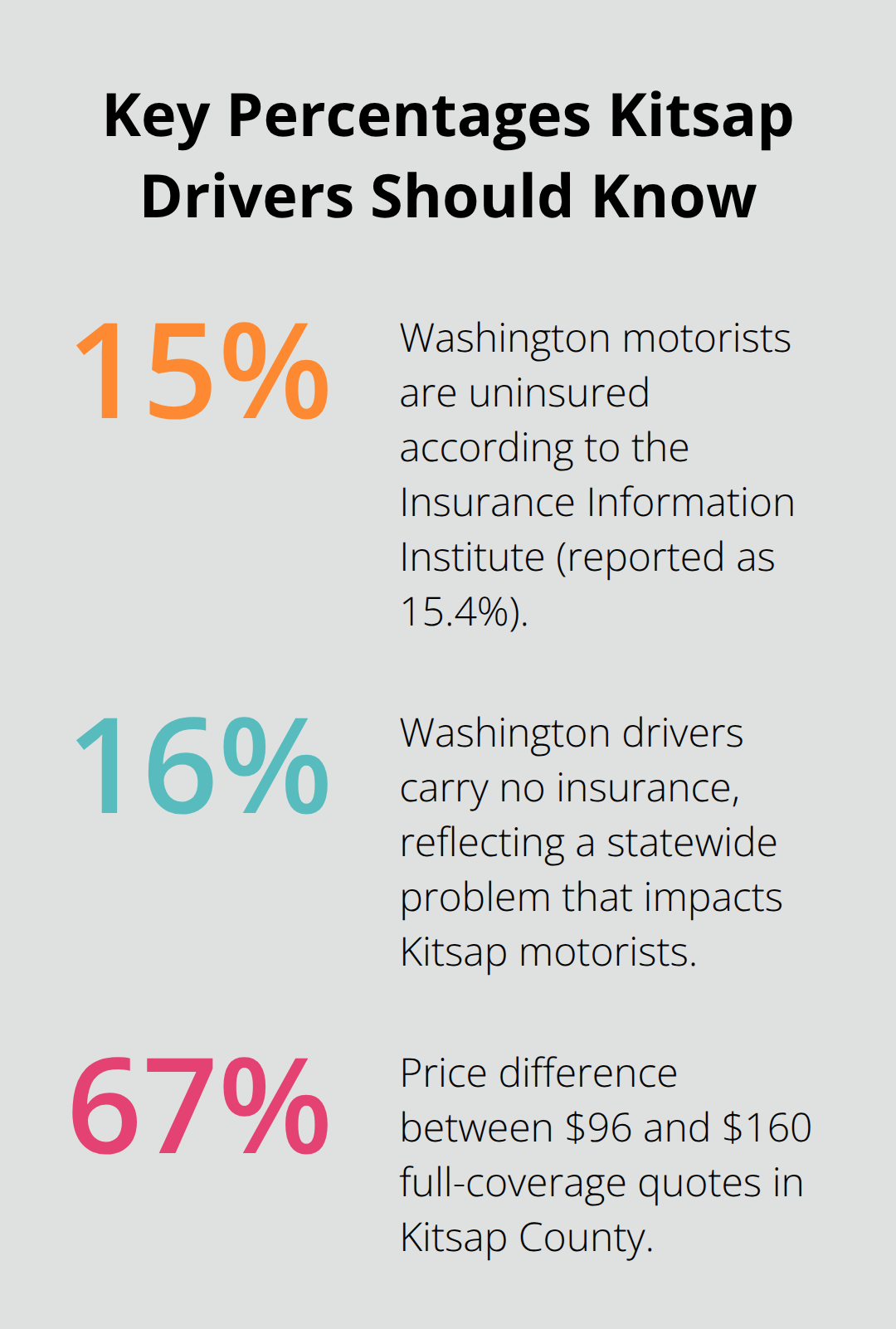

Uninsured and underinsured motorist coverage protects you when another driver causes an accident but carries insufficient or no insurance. 15.4 percent of motorists are uninsured according to the Insurance Information Institute, and Kitsap County reflects this statewide problem. This coverage costs roughly 50 to 100 dollars per year and represents one of the smartest investments you can make.

If an uninsured driver hits you, your own insurance pays for your injuries and vehicle damage instead of leaving you uncompensated. Underinsured motorist coverage fills the gap when the at-fault driver’s limits don’t cover your actual losses. With more than one in seven drivers operating without insurance, UM/UIM coverage represents practical protection against a real local threat.

Full Coverage for Financed Vehicles

Collision and comprehensive coverage protect your vehicle itself, not just liability to others. Collision pays for damage to your car in accidents, while comprehensive covers theft, weather, vandalism, and other non-collision events. Kitsap County experiences significant weather-related damage from winter storms and occasional hail, making comprehensive coverage especially valuable here. If you finance or lease your vehicle, your lender requires full coverage. In Kitsap County, full coverage averages 80 to 160 dollars per month according to Bankrate’s 2026 analysis, substantially less than the national average of about 169 dollars per month. Raising your deductible from 500 dollars to 1,000 dollars can reduce premiums by roughly 15 to 25 percent if you can afford to cover that deductible yourself. GEICO offers full coverage in Kitsap at around 96 dollars per month, while PEMCO runs about 101 dollars per month, giving you specific benchmarks when comparing quotes.

Finding the Right Balance for Your Situation

Your actual coverage needs depend on your assets, driving patterns, and financial situation. Drivers with significant savings or home equity should try higher liability limits and comprehensive coverage to protect what they’ve built. Those with minimal assets can operate with lower limits, though we still recommend UM/UIM coverage given local uninsured driver rates. Your vehicle’s value also matters-older cars may not justify collision coverage, while newer financed vehicles require it. Local independent agents who represent multiple carriers can compare rates across top options and help you identify which coverage gaps matter most for your specific circumstances.

Why Kitsap Coverage Gaps Matter

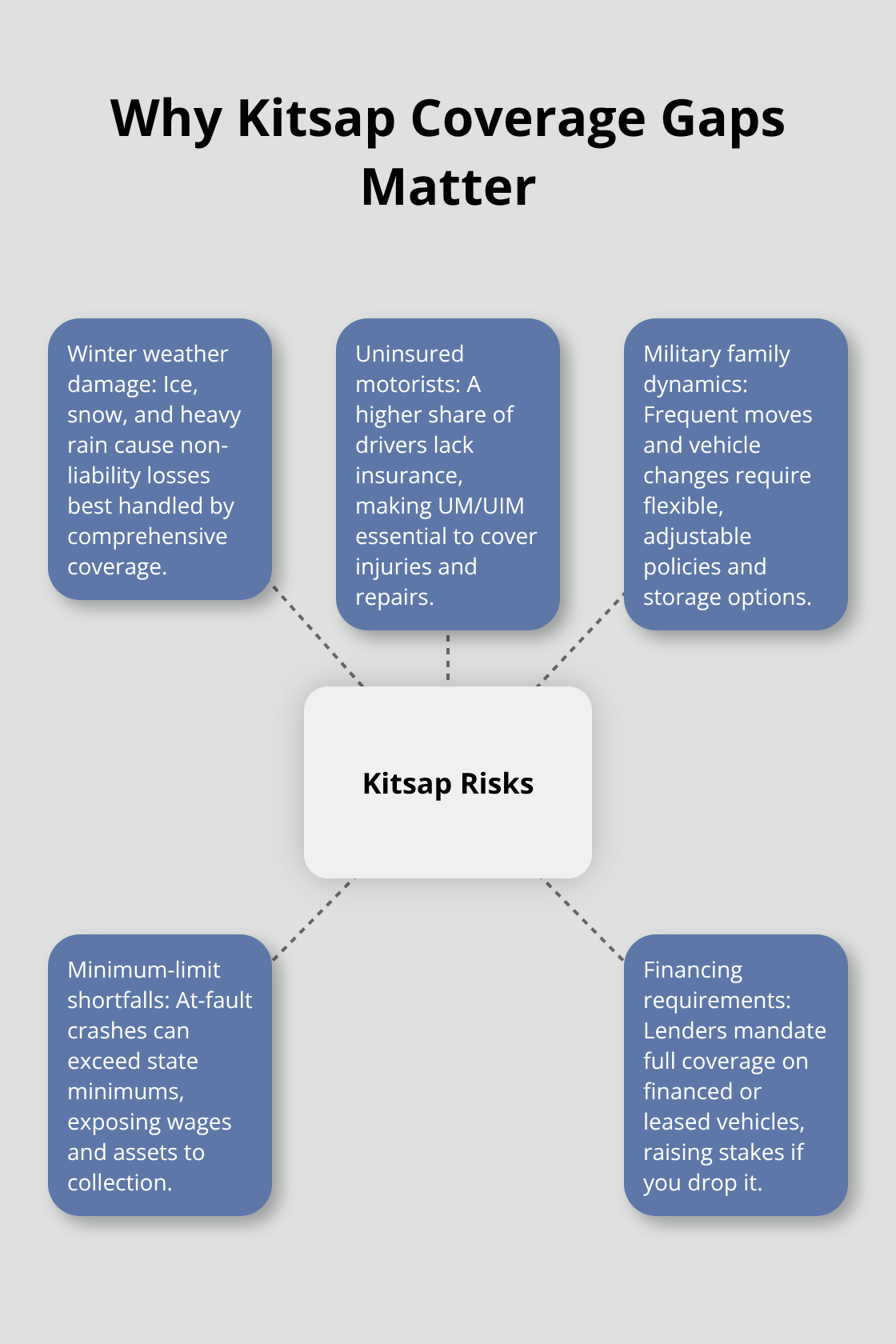

Standard policies protect you against liability, but they leave you exposed to the specific threats Kitsap County drivers face daily. Weather patterns in this region create damage that liability coverage never touches, and the local driver population includes a disproportionate number of uninsured motorists. Military families rotating through Naval Base Kitsap bring different insurance needs than traditional homeowners, yet most off-the-shelf policies don’t account for military-specific risks.

The gap between what you think you’re covered for and what actually protects you in Kitsap is where financial disasters happen. Full coverage at 80 to 160 dollars per month in Kitsap County costs substantially less than the national average of about 169 dollars per month, yet many drivers skip it entirely to save money on minimum coverage. That decision costs them when winter storms hit or an uninsured driver causes an accident.

Winter Weather Threatens Your Vehicle

Winter weather in Kitsap creates comprehensive coverage claims that most drivers underestimate. Ice, snow, and heavy rain damage vehicles through collisions with debris, hydroplaning accidents, and weather-related mechanical failures that comprehensive coverage addresses. Collision coverage pays when you hit something or something hits you during poor driving conditions, which happens regularly on Kitsap roads between November and March. A single winter storm can trigger hundreds or thousands of dollars in damage that liability coverage ignores entirely.

Uninsured Drivers Create Real Risk

Uninsured motorist coverage becomes critical because approximately 16 percent of Washington drivers carry no insurance, and Kitsap reflects this statewide problem. One accident with an uninsured driver can wipe out savings if you only carry minimum liability, since that driver has nothing to pay your damages. This coverage may help pay for damage and injury from a hit-and-run accident or a phantom vehicle and protects you when the other driver cannot.

Military Families Need Flexible Policies

Military families stationed at Naval Base Kitsap face unique challenges: frequent vehicle changes, potential overseas deployment affecting insurance needs, and higher accident rates among younger service members new to the area. These drivers need flexible policies that adjust as their circumstances change, not rigid standard policies designed for permanent residents. H&K Insurance Agency works with military families to build policies that account for deployment timelines, temporary vehicle storage, and coverage gaps that arise when servicemembers relocate. The right coverage costs only slightly more than minimum protection but prevents the financial catastrophe that follows inadequate insurance in Kitsap’s specific environment.

Understanding what coverage gaps exist in your current policy is the first step toward real protection. The next section shows you how to assess your actual needs and compare rates across carriers that serve Kitsap drivers.

How to Build the Right Kitsap Policy Step by Step

Start with a list of what you actually own and what could financially devastate you if damaged or lost. Your home equity, savings account, vehicle value, and retirement accounts represent assets worth protecting. If you own a home in Kitsap County worth $400,000 and carry only minimum liability coverage of $25,000, a single at-fault accident leaves $375,000 exposed to judgment. That means wage garnishment and asset seizure in Washington’s at-fault system. Drivers with significant net worth need 100/300/100 liability limits or higher, plus an umbrella policy covering additional millions. Those renting with minimal savings can operate with lower liability limits, though we still recommend UM/UIM coverage regardless of asset level given Kitsap’s 16 percent uninsured driver rate.

Your vehicle situation matters equally. Financed or leased vehicles require collision and comprehensive coverage by contract, while older paid-off cars may justify dropping collision if the vehicle’s value falls below $5,000. Calculate your actual replacement cost for each vehicle and determine whether a deductible increase makes sense for your budget. Raising your deductible from $500 to $1,000 cuts premiums by 15 to 25 percent, but only if you can actually pay that $1,000 when a claim occurs.

Compare Three Carriers Minimum Every Year

Price differences in Kitsap County are staggering. GEICO quotes around $96 monthly for full coverage while another carrier might charge $160 for identical protection-a 67 percent difference. Calling three insurers or using comparison tools takes an hour and frequently saves $500 to $1,200 annually. Request quotes for the exact same coverage limits across all carriers so you’re comparing apples to apples. Most people shop once when purchasing a car, then never compare again, leaving hundreds on the table yearly.

An independent agency like H&K Insurance Agency represents multiple top carriers in Kitsap, which means they can mirror rates across GEICO, PEMCO, Progressive, State Farm, and others to find your actual lowest cost for real protection rather than pushing one company’s products.

Combine Coverage and Lock In Savings

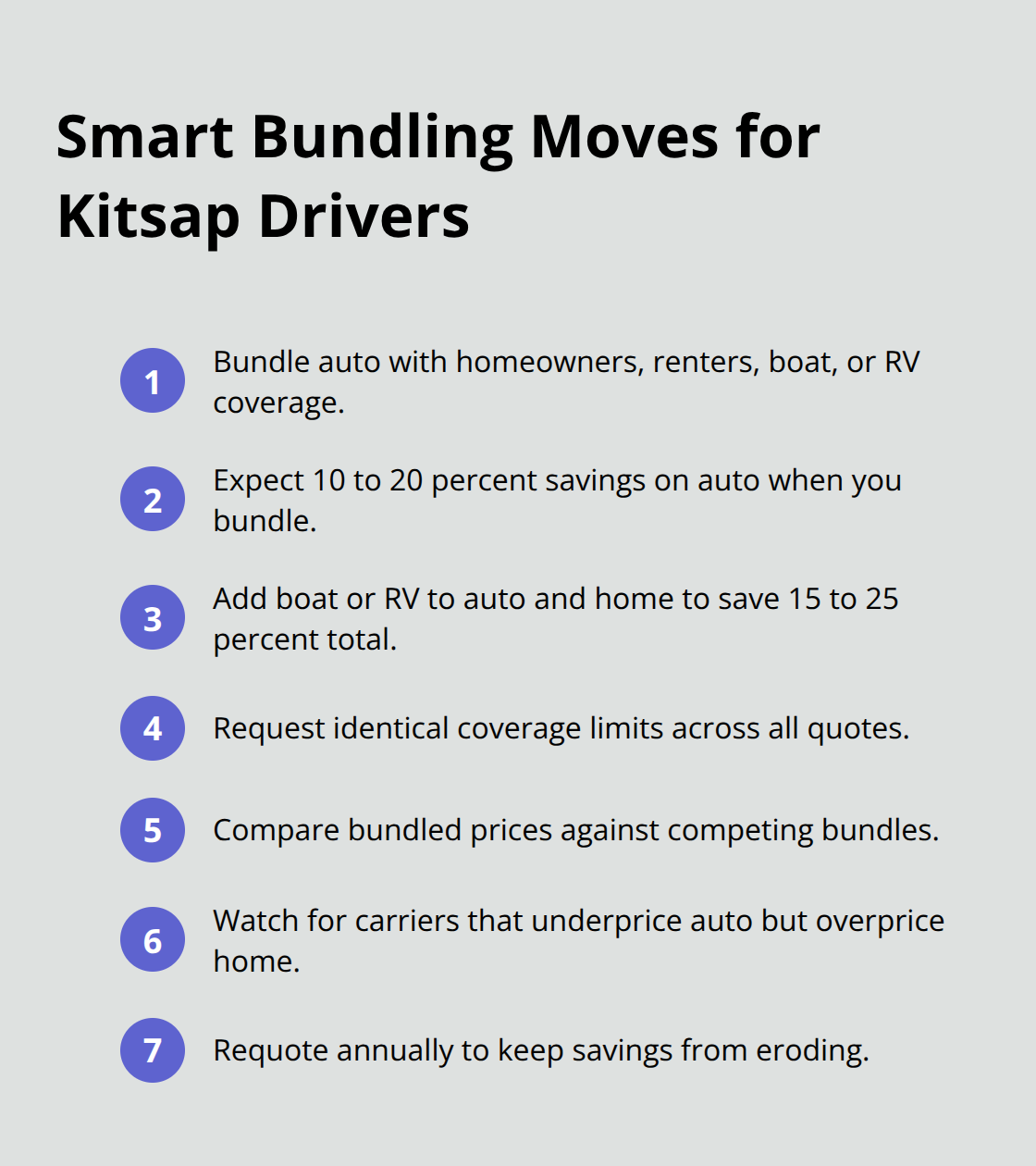

Combining auto insurance with homeowners, renters, boat, or RV coverage saves 10 to 20 percent on premiums. PEMCO and Mutual of Enumclaw offer particularly strong bundle rates in Kitsap County. If you own a boat or RV in addition to a vehicle, combining all three policies typically generates 15 to 25 percent total savings compared to purchasing each separately. Many drivers insure their boat through one company and car through another, missing $200 to $400 in annual savings.

Request bundle quotes as your baseline, then compare that bundled price against competitors’ bundled offers. Some carriers discount auto heavily but charge premium rates for home coverage, so the best bundle differs by household. Shopping bundles takes longer than shopping auto alone, but the savings compound annually and represent real money staying in your pocket instead of going to an insurance company.

Final Thoughts

Kitsap County drivers who carry only minimum liability coverage gamble with their financial future. Winter weather, uninsured drivers, and Washington’s at-fault liability system create real threats that standard policies miss, and inadequate coverage leads to wage garnishment or asset seizure. Building a Kitsap County car policy that protects your assets costs far less than most people expect, especially when you compare rates across multiple carriers and bundle coverage with home or boat insurance.

List your assets, determine what financial loss would hurt you most, and request quotes for coverage that actually protects those things. Ask three insurers for identical coverage limits so you compare real pricing, inquire about bundle discounts if you own a home or RV, and consider raising your deductible from $500 to $1,000 to cut premiums by 15 to 25 percent (if you have cash reserves to cover that deductible when a claim happens). These steps take a few hours but typically save $500 to $1,200 annually while closing the coverage gaps that create financial disasters.

Contact H&K Insurance Agency to build your Kitsap County car policy with the coverage you actually need at a price that makes sense for your budget. We represent multiple top carriers serving Kitsap and customize packages with bundling, higher liability limits, uninsured motorist coverage, and full coverage options tailored to your specific assets and driving patterns. Military families rotating through Naval Base Kitsap work with us to build policies that adjust as their circumstances change.