Rideshare Auto Insurance Kitsap: Protect Your Drive Share Earnings

Rideshare driving in Kitsap County can generate solid income, but your personal auto insurance policy has a major blind spot: it won’t cover you while you’re working for Uber or Lyft.

At H&K Insurance Agency, we’ve seen too many drivers learn this the hard way after an accident leaves them unprotected. The gap between personal and commercial coverage is real, and it can cost you thousands.

This guide walks you through rideshare auto insurance in Kitsap so you understand exactly what protection you need.

Rideshare Coverage Gaps Most Drivers Don’t Know About

What Your Personal Auto Policy Actually Excludes

Your standard personal auto insurance policy stops covering you the moment you turn on the Uber or Lyft app with the intention to accept rides. Insurance companies classify this as commercial activity and explicitly exclude it from personal auto coverage. This isn’t a gray area or something an adjuster might overlook-it’s written directly into your policy documents. If you crash while logged into the app and waiting for a ride request, your insurer will deny your claim. You’ll face the full cost of repairs, medical bills, and liability out of your own pocket.

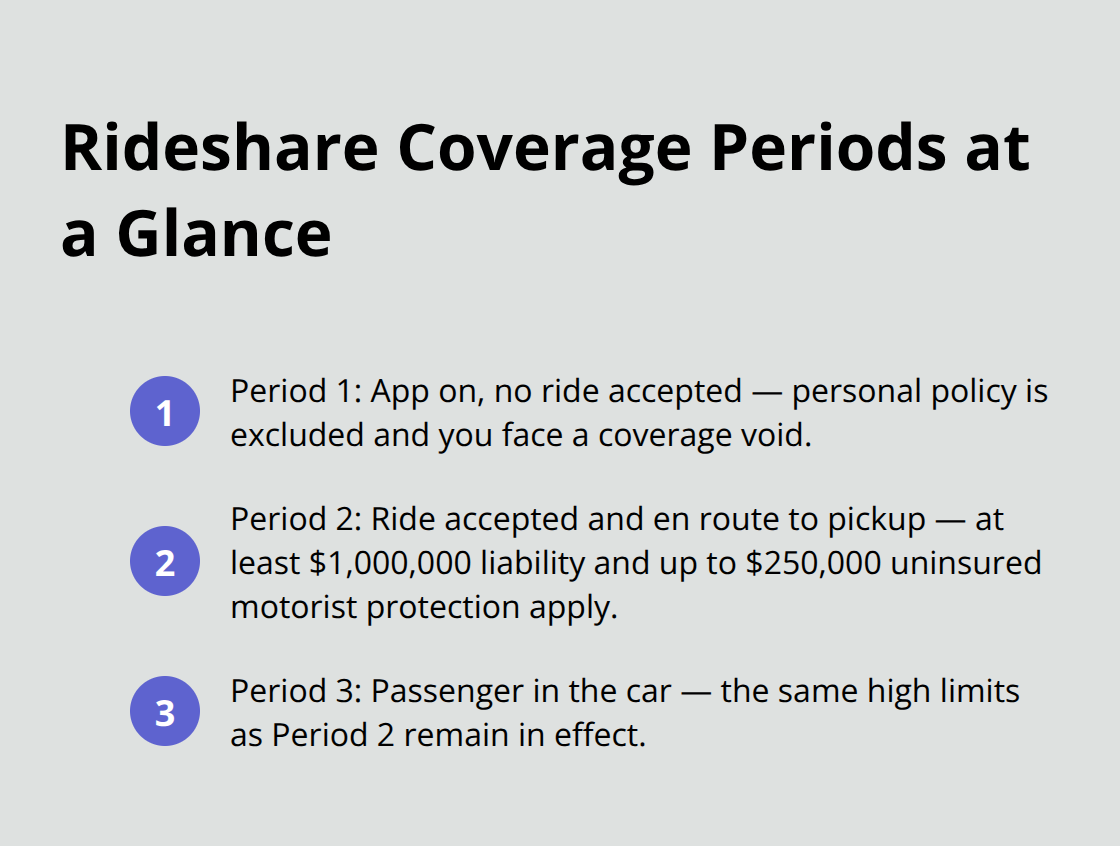

The Three Dangerous Periods Every Driver Faces

Rideshare driving involves three distinct coverage periods, and each one presents different risks. During Period 1, when your app is on but you haven’t accepted a ride yet, you sit in a coverage void. Your personal policy won’t activate until you’re off the clock.

Period 2 begins the moment you accept a ride and start driving toward pickup. Here, liability coverage jumps to at least $1,000,000 per accident, and you gain uninsured motorist protection of up to $250,000 per accident. Period 3, during the actual passenger ride, maintains those same high limits. The real problem surfaces in Period 1-that waiting period between logging in and accepting your first ride. Many drivers assume their personal insurance covers them here because they haven’t technically picked up anyone yet. It doesn’t. A single accident during this gap can wipe out weeks or months of rideshare earnings.

Why Contingent Coverage Falls Short

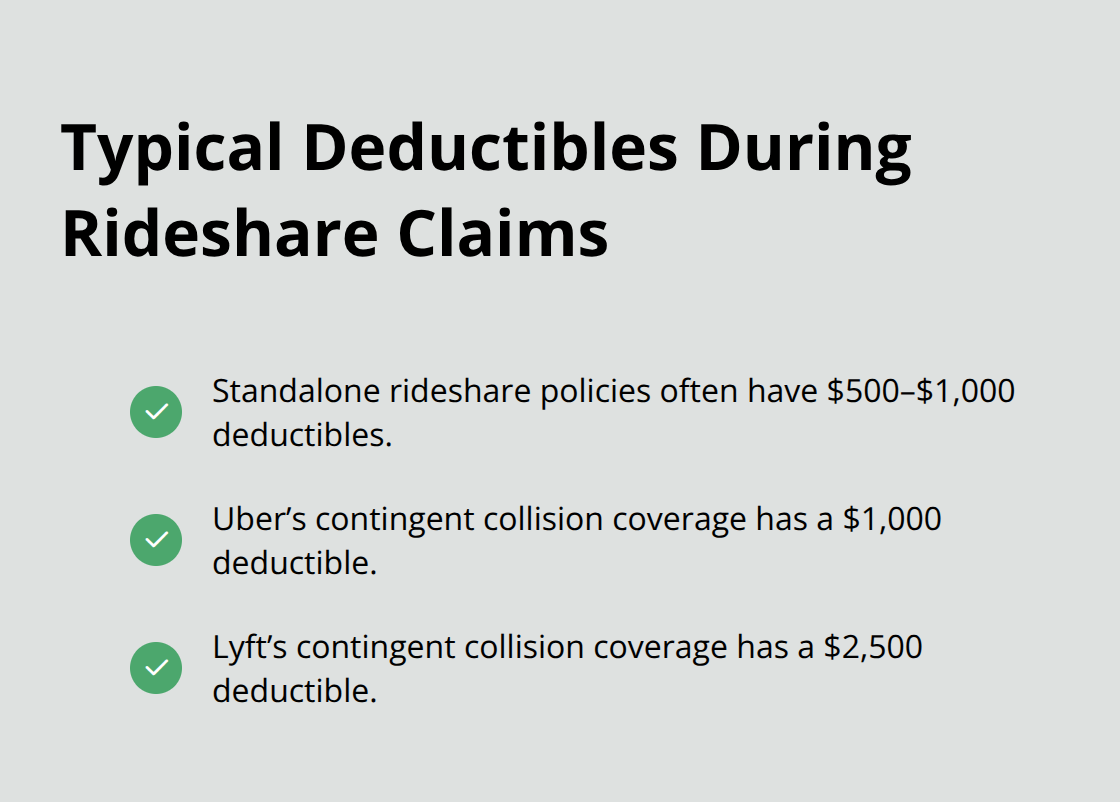

Some drivers believe their personal collision and comprehensive coverage will handle accidents during rideshare work. This assumption proves dangerously wrong. If you’re logged into the app, even in Period 1, your personal policy’s physical damage coverage becomes void. Rideshare-specific policies do include contingent collision and comprehensive coverage, but only if you maintain physical damage coverage on your personal auto policy. More importantly, this contingent coverage carries substantial deductibles before it kicks in. That means in a moderate accident, you pay that deductible first, then deal with the gap between your personal policy’s limits and what the rideshare platform provides. The platforms themselves offer some protection, but it’s secondary and has significant gaps. Uber and Lyft’s coverage only protects passengers and third parties, not your vehicle or your own medical expenses. If another driver hits you and they’re uninsured or underinsured, you need uninsured motorist coverage that actually applies during rideshare work. Without a proper rideshare policy, you’re counting on the other driver’s insurance to cover everything, which often leaves you short.

Understanding What Rideshare Platforms Actually Cover

The rideshare companies provide liability coverage during active trips, but this protection has strict limits. Their policies cover third-party bodily injury and property damage, meaning they protect your passengers and other drivers-not you. If you suffer injuries or your vehicle takes damage, you can’t rely on Uber or Lyft to pay your medical bills or repair costs. This is where the coverage gap becomes critical. You need your own rideshare insurance policy to fill what the platforms won’t cover. The right policy protects your earnings and your assets when accidents happen on the job.

How Rideshare Insurance Works in Washington State

State Requirements for Rideshare Drivers

Washington State doesn’t mandate rideshare insurance specifically, but it does require you to carry minimum liability coverage that actually applies during rideshare work. This is where most drivers get confused. Your personal auto policy’s liability limits don’t transfer to rideshare activity, so you need separate coverage that activates the moment your app turns on. Washington recognizes three distinct periods of rideshare work, and each has different insurance requirements.

During Period 1, when your app is active but you haven’t accepted a ride, you need at least $50,000 in bodily injury coverage per person and $20,000 for property damage. This is state minimum coverage, and it’s frankly inadequate given the risks you face. Once you accept a ride and head toward pickup in Period 2, your liability coverage must jump to at least $1,000,000 per accident. That same $1,000,000 limit applies during the actual trip in Period 3. Washington doesn’t play around with these numbers because rideshare drivers carry passengers for money, which makes them commercial operators in the state’s eyes.

How Coverage Stacks With Your Personal Policy

Your rideshare policy becomes primary during periods when you’re logged in and actively working. Your personal auto insurance sits in the background as secondary coverage only if something falls outside your rideshare policy’s scope, which rarely happens. This stacking structure protects you because the rideshare policy activates first and covers the gaps your personal policy explicitly excludes.

Physical damage coverage gets more complicated. If you carry collision and comprehensive on your personal policy, rideshare coverage includes contingent collision and comprehensive protection, but with hefty deductibles. Uber applies a $1,000 deductible while Lyft charges $2,500 before their contingent coverage kicks in. This means a minor fender bender costs you that full deductible out of pocket before insurance covers anything.

Uninsured Motorist Protection During Rideshare Work

Uninsured motorist coverage in Washington rideshare policies typically reaches $250,000 per accident during Period 2 and Period 3, protecting you when another driver lacks adequate insurance or flees the scene. This coverage protects your medical bills and lost wages, not just your vehicle. If another driver hits you and they’re uninsured or underinsured, you need uninsured motorist coverage that actually applies during rideshare work.

Verify your rideshare policy actually includes uninsured motorist protection at levels matching your liability limits. Many drivers purchase inadequate UM coverage and discover the gap only after a hit-and-run or accident with an uninsured driver. The difference between $250,000 and $1,000,000 in UM coverage can mean thousands of dollars out of your pocket when you need it most.

Selecting Coverage That Matches Your Risk

The right rideshare policy fills what the platforms won’t cover and protects your earnings when accidents happen on the job. Your personal policy treats rideshare activity as an excluded activity, period, so you can’t rely on it to bridge the gap. Understanding these three periods and their corresponding coverage requirements helps you make informed decisions about what protection you actually need. As you evaluate your options, the next step involves comparing the different types of rideshare policies available and determining which deductible levels and coverage limits align with your income and risk tolerance.

Choosing the Right Rideshare Coverage for Your Situation

Standalone Policies vs. Rideshare Endorsements

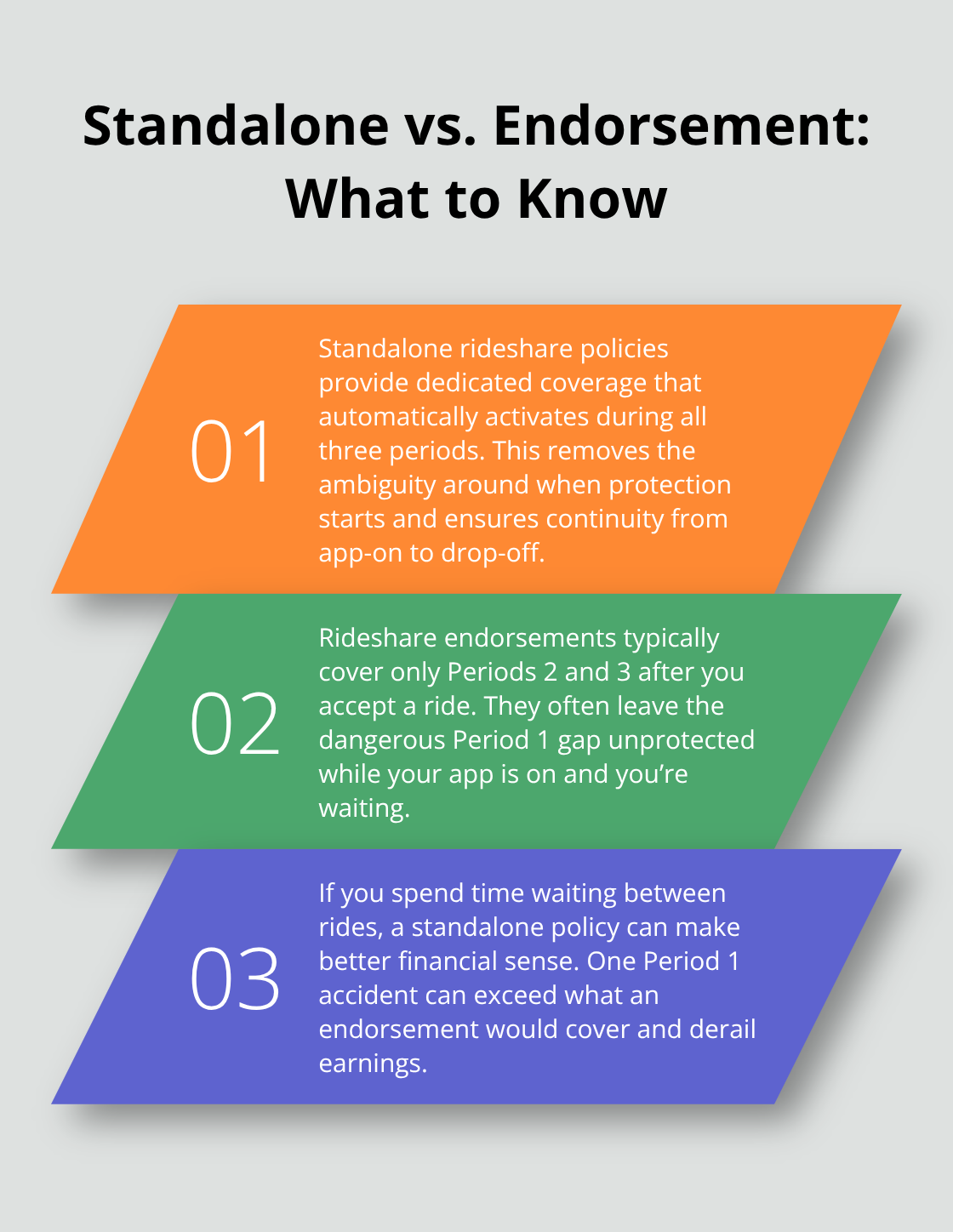

Rideshare drivers in Kitsap County face a stark choice: purchase a standalone rideshare policy or add a rideshare endorsement to your existing personal auto insurance. The standalone approach provides dedicated coverage that activates automatically during all three periods of rideshare work. An endorsement, by contrast, typically covers only Periods 2 and 3 after you accept a ride, leaving that dangerous Period 1 gap unprotected when your app is on but no passenger sits in the car yet. If you spend significant time waiting between rides, the standalone policy makes more financial sense because a single accident during Period 1 can exceed what an endorsement covers.

Most Kitsap drivers who choose endorsements discover too late that their coverage stops the moment they log in and start hunting for that first ride.

Deductible Structures and Their Real Impact

The deductible structure differs significantly between these two approaches. Standalone rideshare policies typically carry lower deductibles ranging from $500 to $1,000, while contingent collision coverage through an endorsement saddles you with Uber’s $1,000 deductible or Lyft’s $2,500 deductible before any physical damage coverage activates. That $2,500 Lyft deductible eats into your weekly earnings fast on minor accidents. If you drive for both platforms, a standalone policy eliminates the confusion of managing two different deductible levels.

When you evaluate your deductible choice, calculate your average weekly rideshare income and select a deductible you could absorb without disrupting your finances. A driver earning $600 weekly should not choose a $2,500 deductible because one accident wipes out over four weeks of income before insurance covers anything. Conversely, a driver earning $1,500 weekly can justify the higher deductible in exchange for lower monthly premiums.

Bundling Strategies to Lower Your Overall Costs

The bundling strategy works powerfully in your favor if you carry other insurance needs. Drivers who bundle rideshare coverage with personal auto, renters, or home policies under one agent often see savings on their total insurance costs. Bundling also simplifies your administration because one agent reviews all your coverage annually and identifies gaps you might miss. H&K Insurance Agency, a locally owned independent agency serving the Puget Sound region, represents multiple top carriers and can compare rates across different bundling combinations to find the right protection at competitive prices.

Coverage Limits That Protect Your Assets

Coverage limits deserve equal attention to deductibles. Washington State’s minimum $1,000,000 liability limit during active trips sounds adequate until you hit someone with significant injuries or property damage. Medical bills for serious injuries regularly exceed $500,000, and you remain personally liable for anything above your coverage limit. Selecting $1,000,000 in uninsured motorist coverage matching your liability limits protects you when hit-and-run drivers or uninsured motorists cause accidents.

Many drivers make the mistake of accepting whatever limits their insurer suggests rather than intentionally selecting coverage that matches their income and asset protection needs. The right coverage protects your earnings and your assets when accidents happen on the job.

Final Thoughts

Rideshare auto insurance in Kitsap protects your earnings and assets when accidents happen during those vulnerable waiting periods. The coverage gaps between your personal policy and rideshare work cost drivers thousands every year, and you now understand why contingent coverage through an endorsement leaves you exposed during Period 1. Your next move requires matching your coverage limits to your actual income and risk tolerance rather than accepting whatever an insurer suggests.

A driver earning $600 weekly shouldn’t carry a $2,500 deductible, just as a driver with significant personal assets shouldn’t settle for minimum liability limits. Bundling rideshare coverage with your personal auto, renters, or home insurance simplifies administration and often reduces your total monthly costs. Working with a local agent who understands Kitsap County’s specific driving patterns makes a measurable difference in your protection.

H&K Insurance Agency serves the Puget Sound region as a locally owned independent agency representing multiple top carriers. They compare rates and customize packages so you get the right rideshare auto insurance Kitsap coverage at competitive prices. Contact them today to discuss your specific situation and secure proper coverage before your next shift.