Condo Homeowners Coverage Bremerton: Protecting Your Shared Investment

Condo ownership in Bremerton comes with unique insurance challenges that many owners overlook. Your HOA’s master policy covers the building structure, but it leaves significant gaps in personal property and liability protection.

At H&K Insurance Agency, we’ve seen too many condo owners discover these gaps only after a loss occurs. The right condo homeowners coverage in Bremerton fills those gaps and protects your financial security.

What Your Condo Insurance Actually Covers

Your HOA’s master policy covers the building’s structure and common areas, but that protection stops at your unit’s walls. An HO-6 condo policy fills the gap by covering your personal belongings, interior improvements, and liability exposure within your unit. In Washington State, condo owners hold responsibility for everything inside their walls, not the HOA. If your kitchen cabinets, flooring, or built-in appliances suffer damage from fire, frozen pipes, vandalism, or glass breakage, your condo insurance pays for repairs or replacement. Personal property coverage typically ranges from $50,000 to $100,000 or more, depending on what you own.

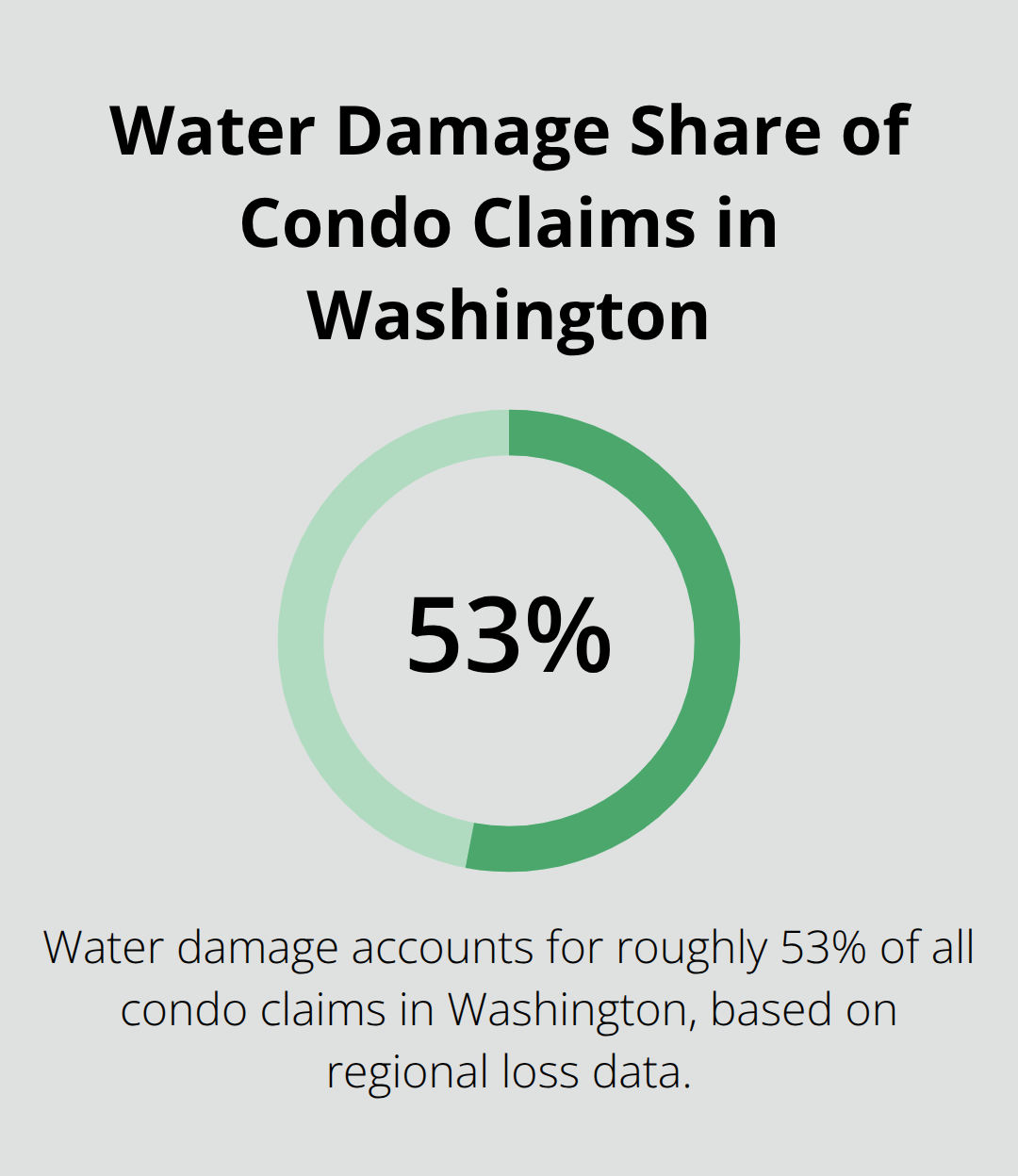

Water Damage Claims Dominate Condo Losses

Water damage represents the dominant condo claim in Washington, accounting for roughly 53% of all claims according to regional loss data. Your HO-6 policy covers water damage from burst pipes and frozen plumbing, but it explicitly excludes sewer or drain backups. Adding a separate water backup endorsement costs only a few dollars monthly yet prevents bills exceeding $10,000.

This single addition protects your investment far beyond its modest cost.

Interior Upgrades Demand Higher Dwelling Limits

Many condo owners accept the default HO-6 dwelling limit, which often starts at just $1,000 to $5,000. That figure proves dangerously low if you’ve invested in kitchen remodels, bathroom upgrades, or replaced flooring. Try raising your dwelling limit to at least $50,000 to match the actual replacement cost of typical interior improvements in Bremerton properties. Your liability coverage should start at $100,000 minimum, but given that Seattle settlements averaged around $68,000 in 2022, you should seriously consider higher limits or an umbrella policy adding $1 million in protection.

Loss Assessment and Special Assessments

Loss assessment coverage protects you against special assessments when the master policy’s deductible is exceeded after a major loss. The standard $1,000 limit proves insufficient, so increase it to $5,000 to $10,000 depending on your building size. This coverage shields you from unexpected bills that can strain your finances after a disaster.

High-Value Items Need Scheduled Endorsements

High-value items like jewelry, art, or collectibles often face underprotection by standard condo coverage because of sub-limits on specific categories. Scheduled endorsements cost relatively little but provide replacement-cost protection without depreciation. Your coverage should adjust after interior upgrades, property value changes, or shifts in what the master policy covers-annual policy reviews help you stay protected. As your condo investment grows and your needs shift, the right coverage adjustments become even more important for your next steps.

Why Your HOA’s Master Policy Leaves You Exposed

The Master Policy Covers Only the Building Structure

Your HOA’s master policy covers the building structure and common areas, but Washington State law places responsibility for everything inside your unit squarely on your shoulders. The master policy typically covers at least 80% of replacement cost for the building’s exterior, roof, and shared spaces under the Washington Condominium Act, yet this leaves your interior completely unprotected. When water intrusion damages your drywall, flooring, or cabinetry, the master policy deductible often runs around $25,000, meaning you’ll pay that entire amount out of pocket before any coverage kicks in. If the loss exceeds the master policy limit, you face a special assessment that can cost thousands.

Your Interior Improvements Remain Your Responsibility

Many condo owners assume the HOA covers everything, then face devastating financial exposure after a fire, flood, or major water event. The gap between what the master policy covers and what actually protects your investment is where condo owners get hurt. Your kitchen cabinets, flooring, and built-in appliances fall under your responsibility, not the HOA’s. A single water event can trigger out-of-pocket costs that proper condo insurance would have prevented entirely.

Personal Liability in Shared Spaces Creates Serious Exposure

Your personal liability in shared spaces creates another significant exposure that standard homeowners insurance doesn’t address properly. If a guest slips on your balcony or suffers an injury inside your unit, your liability coverage must defend you and cover medical bills or legal judgments. The standard $100,000 liability limit falls short given that Seattle settlements averaged around $68,000 in 2022 alone, meaning a single serious injury could exceed your coverage. An umbrella policy adding $1 million in liability protection costs only $100–$200 annually and becomes essential as your assets grow.

Loss assessment coverage Protects Against Special Assessments

Loss assessment coverage protects you against special assessments triggered when the master policy’s deductible is exceeded. Most condo owners carry only the default $1,000 limit, which proves dangerously inadequate. Increase loss assessment coverage to $5,000–$10,000 depending on your building size and prevent unexpected bills that can strain your finances after a major disaster. These assessments hit suddenly and can affect your entire financial picture if you lack proper protection.

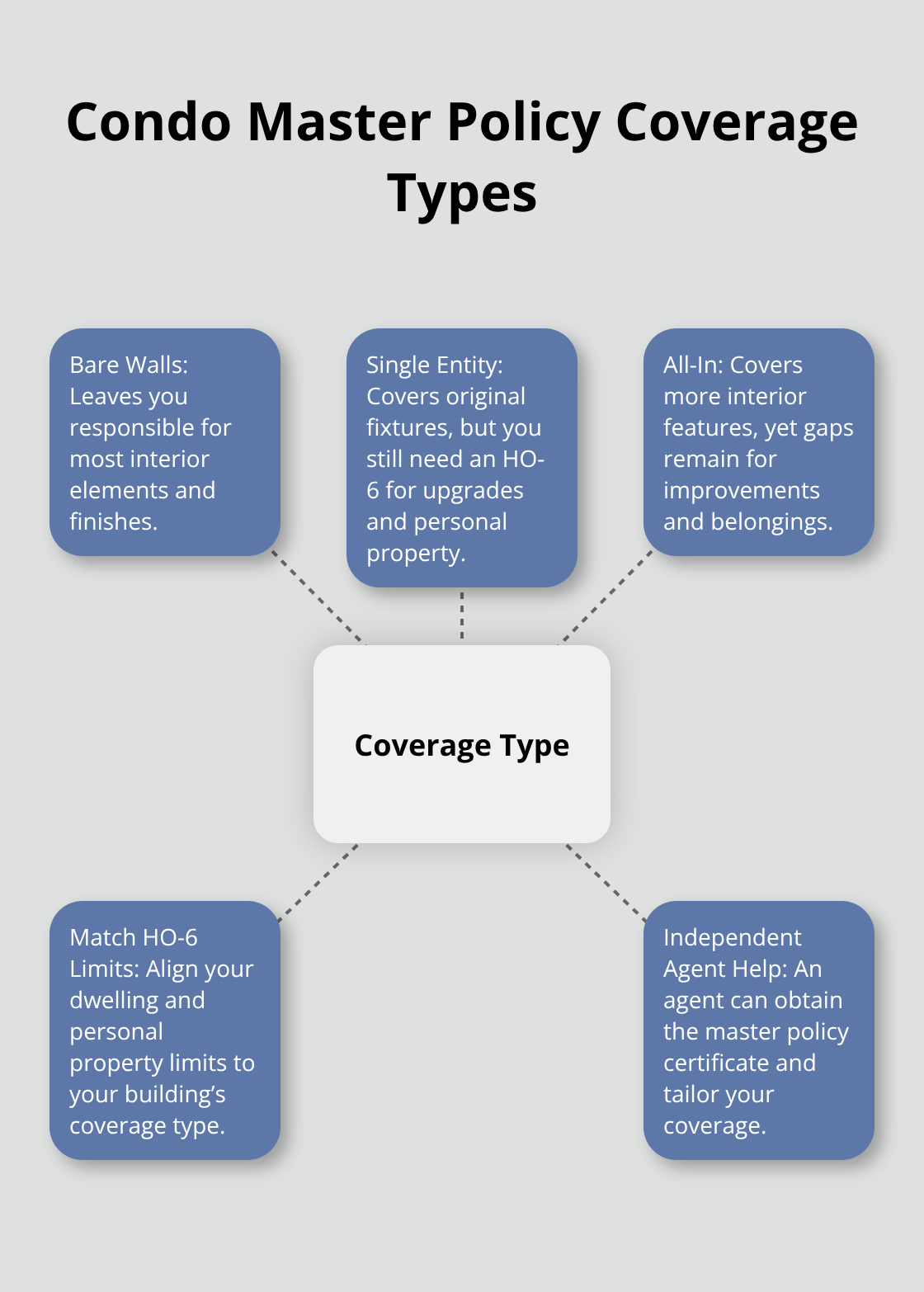

Understanding Your Building’s Coverage Type Matters

The master policy structure varies based on whether your building operates as Bare Walls, Single Entity, or All-In coverage. Bare Walls buildings leave you responsible for virtually all interior elements, while All-In buildings cover more (though gaps still exist). Identifying your building’s coverage type helps you align your HO-6 limits with actual exposure. An independent agent representing multiple carriers can help you obtain the master policy certificate from your HOA and customize coverage that fills the specific gaps your building creates.

How to Build Your Custom Condo Coverage Plan

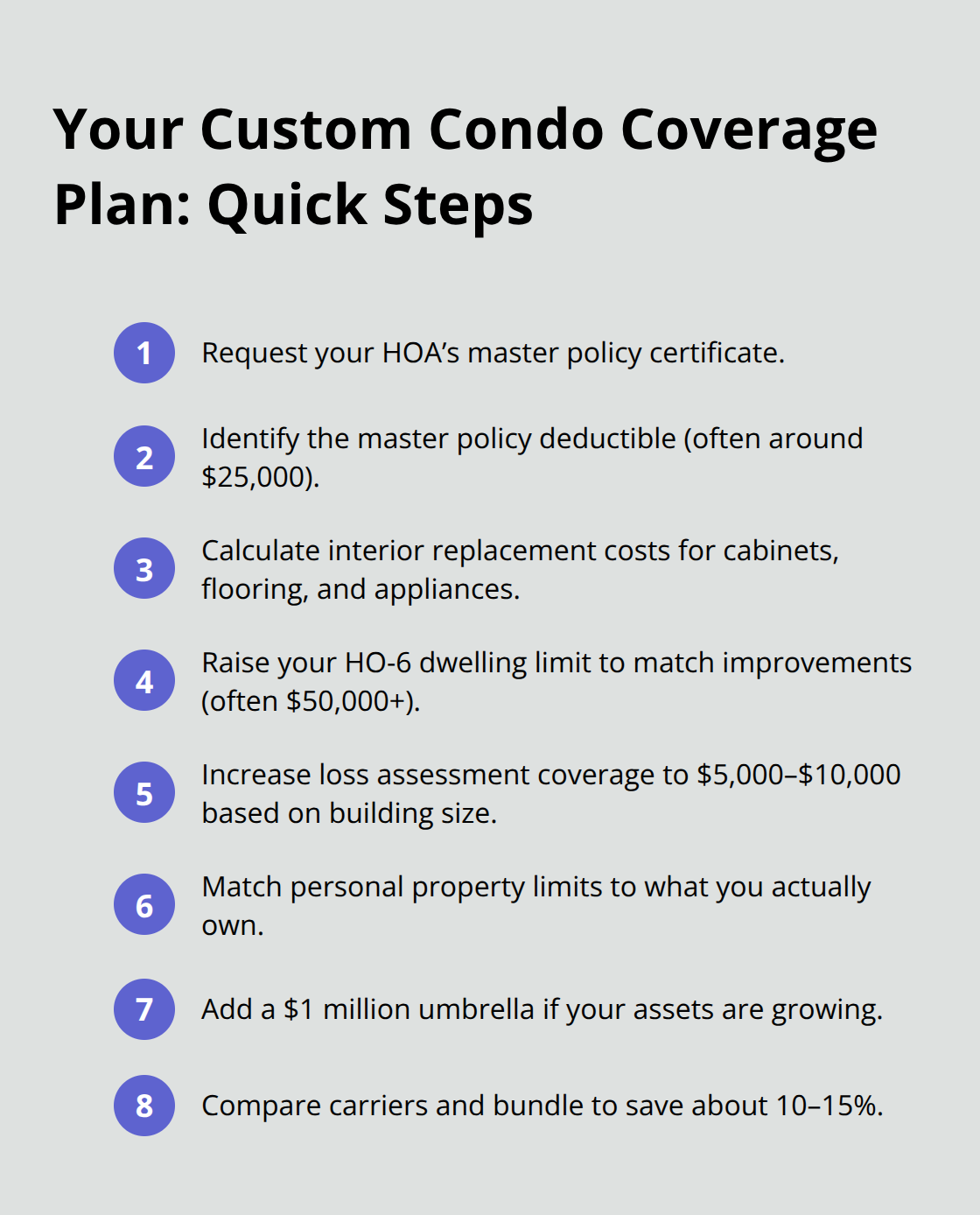

Request Your Master Policy Certificate First

Contact your HOA directly and request the master policy certificate. This document shows exactly what the master policy covers and, critically, what it excludes. You need to know whether your building operates under Bare Walls, Single Entity, or All-In coverage because this determines your actual exposure.

Bare Walls buildings shift nearly all interior responsibility to you, while All-In buildings cover more-though gaps still exist in every structure type.

Once you have the certificate, identify the master policy’s deductible. If it runs around $25,000 (typical for Washington condo buildings), you’ll face that out-of-pocket cost before any coverage applies to water damage or other major losses. This single fact should drive your loss assessment coverage decision immediately.

Calculate Your Interior Replacement Cost and Adjust Dwelling Limits

Walk through your unit and price kitchen cabinets, flooring, appliances, and any upgrades you’ve made. Most owners underestimate this figure significantly. If you’ve invested in remodels, your dwelling limit should jump to $50,000 minimum instead of accepting the default $1,000–$5,000.

Increase loss assessment coverage from the standard $1,000 to at least $5,000, ideally $10,000 if your building has more than 50 units. This protects you against special assessments triggered when the master policy’s deductible is exceeded after a major loss.

Match Personal Property Coverage to Your Actual Belongings

Personal property coverage should match your actual belongings-not a generic estimate. If you own furniture, electronics, clothing, and artwork worth $75,000, don’t settle for a $50,000 limit. Customized policies protect high-value items like jewelry or art without depreciation, costing only $75–$150 annually for substantial peace of mind.

Evaluate Your Liability Exposure Carefully

Your liability coverage deserves serious attention. Seattle settlements averaged around $68,000 in 2022, meaning your standard $100,000 limit leaves minimal cushion for a serious injury claim. An umbrella policy adding $1 million costs only $100–$200 yearly and becomes essential as your assets grow.

Compare Rates and Bundle for Savings

Compare rates across multiple carriers because condo pricing varies dramatically. Seattle condo rates average around $570 annually with typical coverage, but this jumps significantly with higher personal-property or liability limits. Bundling your condo insurance with auto coverage typically saves 10–15% on total premiums.

H&K Insurance Agency represents multiple top-rated carriers throughout the Puget Sound region, allowing us to compare pricing and customize packages that address Bremerton-specific risks like water damage, flood exposure, and earthquake liability. You can request a quote by calling 360-377-7645 or visiting our Bremerton office.

Schedule Annual Policy Reviews to Stay Protected

Schedule an annual policy review rather than waiting until renewal. After interior upgrades, property value changes, or HOA master policy modifications, your coverage needs shift. That kitchen remodel or new appliances justify higher dwelling limits. Your growing investment demands reassessment of liability exposure. These reviews take 20 minutes but prevent the financial devastation that underinsurance creates.

Final Thoughts

Condo homeowners coverage in Bremerton protects far more than your belongings-it safeguards your financial security and your largest personal investment. Without proper HO-6 coverage, you face devastating out-of-pocket costs when water damage, fire, or liability claims strike. The master policy covers the building structure, but everything inside your walls remains your responsibility under Washington State law.

The right coverage strategy starts with understanding your specific exposure. Your building’s master policy deductible, the type of coverage structure your HOA carries, and your interior improvements all determine what limits you actually need. A $1,000 dwelling limit won’t rebuild your kitchen after a fire, and a $100,000 liability limit leaves you exposed when a serious injury claim arrives.

Working with local insurance experts who understand Bremerton’s specific risks makes the difference between adequate protection and dangerous underinsurance. At H&K Insurance Agency, we serve the Puget Sound region with personalized condo homeowners coverage that fills the gaps your master policy leaves behind. Contact us at H&K Insurance Agency or call 360-377-7645 to request a quote and build coverage that actually protects your investment.