Kitsap Umbrella Coverage: Why Umbrella Insurance Matters in Kitsap

Your standard homeowners or auto policy likely has liability limits that won’t cover a major accident or lawsuit. One serious incident could expose your personal assets to significant financial risk.

Kitsap umbrella coverage fills those gaps by providing additional liability protection beyond what your existing policies offer. At H&K Insurance Agency, we help Kitsap residents understand how umbrella insurance works and why it matters for protecting the wealth you’ve built.

Why Your Standard Coverage Isn’t Enough in Kitsap

Standard homeowners and auto policies in Washington come with liability limits that sound adequate until a serious accident happens. Most homeowners carry $100,000 to $300,000 in liability protection, which the Washington State Office of the Insurance Commissioner notes is insufficient given Washington’s pure comparative negligence laws. A single lawsuit from a major injury on your property or a car accident you cause can easily exceed these limits. In the Puget Sound region, medical costs and property damage claims regularly surpass $500,000, leaving you personally liable for the difference. This gap becomes real and dangerous to your wealth.

What Umbrella Coverage Actually Covers

Umbrella insurance activates after your underlying homeowners or auto policy limits are exhausted, providing an additional layer of liability protection. If someone suffers a serious injury at your home or you cause a multi-vehicle accident, your umbrella policy covers legal defense costs, medical expenses, and damages beyond your base policy limits. The coverage applies to incidents covered by your underlying policies, meaning it works seamlessly with what you already have. Most umbrella policies start at $1 million in additional coverage, though homeowners with meaningful assets in Kitsap should try $1 million to $2 million. The cost is remarkably low-typically $150 to $300 annually for $1 million in coverage when bundled with existing policies.

Why Kitsap Residents Face Higher Liability Risk

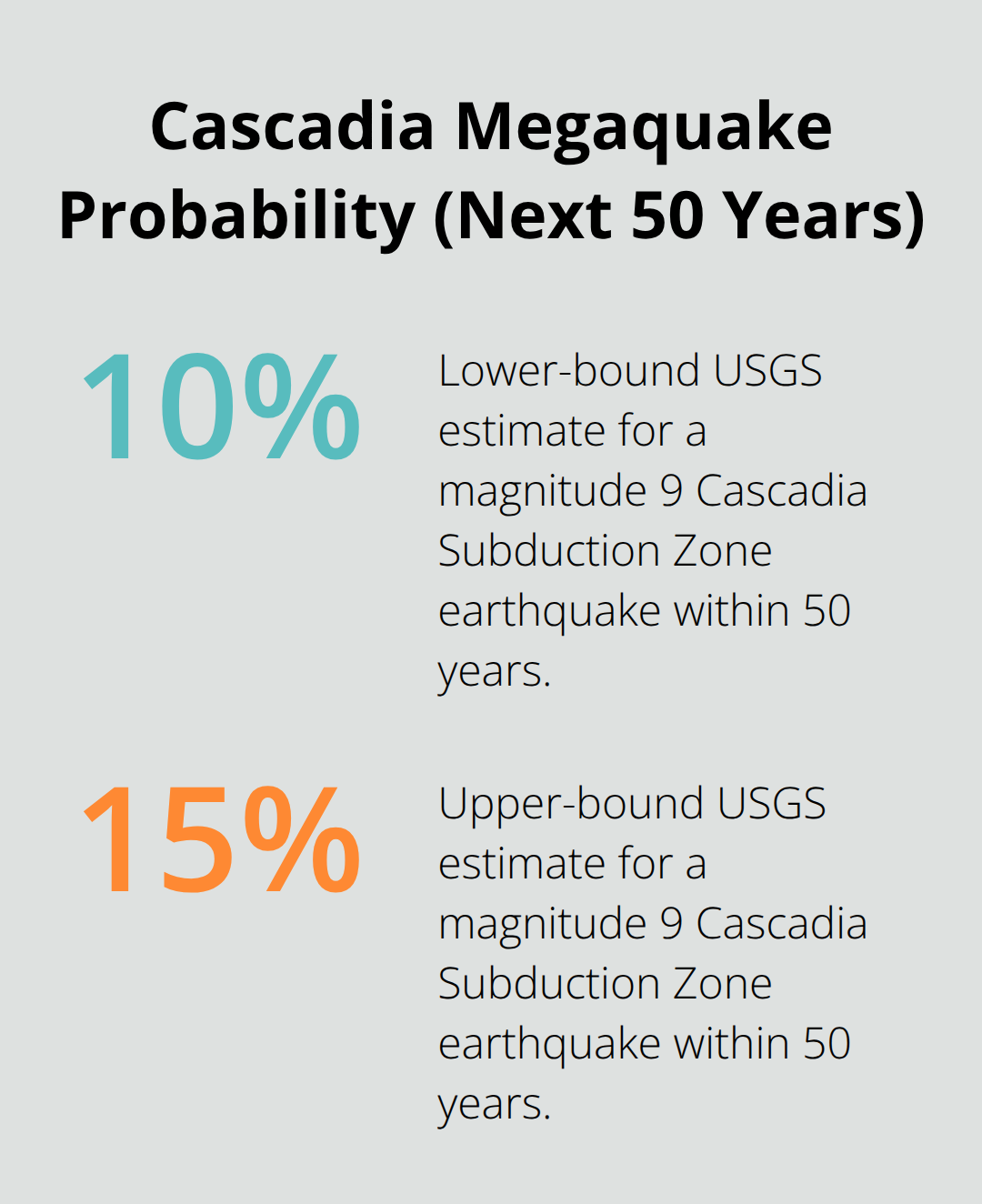

Kitsap’s waterfront properties, active boating culture, and multi-property ownership patterns create specific liability exposures that standard policies don’t adequately address. Boat owners face heightened risk because watercraft liability isn’t covered under homeowners policies, and a boating accident with injuries can result in six-figure claims. Landlords with rental properties face even greater exposure since tenants or their guests can sue for injuries, and the average landlord property damage claim in 2022 exceeded $9,800. Earthquake risk in the Puget Sound adds another layer-the US Geological Survey estimates a 10 to 15 percent probability of a magnitude 9 Cascadia Subduction Zone earthquake within the next 50 years, which can trigger catastrophic property damage and liability exposure. Umbrella coverage protects against these regional hazards in a way your base policies simply cannot.

How Umbrella Policies Work with Your Existing Coverage

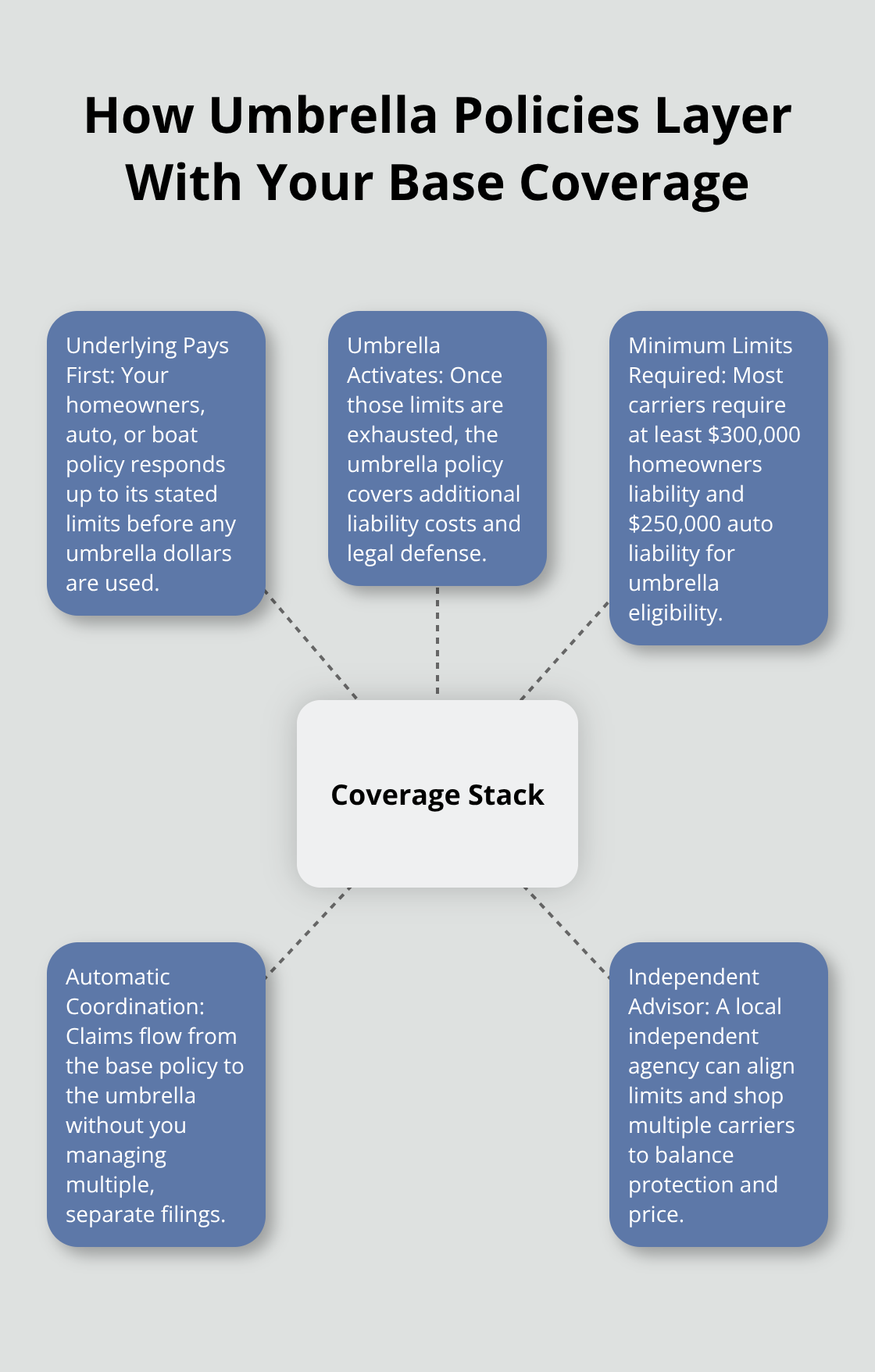

Your umbrella policy sits on top of your homeowners, auto, and boat policies rather than replacing them. When a covered incident occurs, your underlying policy pays first up to its limit, and then your umbrella policy activates to cover additional liability costs. This structure means you need adequate underlying coverage limits for the umbrella to function properly-most insurers require at least $300,000 in homeowners liability and $250,000 in auto liability before they’ll issue an umbrella. The coordination between policies happens automatically, so you don’t need to manage multiple claims separately.

An independent agency representing multiple carriers (like H&K Insurance Agency in Bremerton) can help you structure these layers correctly and compare rates across top local and national carriers to find competitive pricing.

Who Needs Umbrella Insurance in Kitsap

Homeowners with Significant Net Worth

If you own meaningful assets in Kitsap, umbrella insurance isn’t optional-it’s a financial necessity. The Washington State Office of the Insurance Commissioner emphasizes that umbrella coverage protects anyone whose net worth exceeds their underlying liability limits, which applies to most homeowners in the Puget Sound region with properties valued above $400,000. A single lawsuit wipes out years of savings and forces asset liquidation if you lack adequate protection. Homeowners carrying only $100,000 to $300,000 in standard liability coverage face real exposure; one serious injury at your home or a multi-vehicle accident you cause easily exceeds these limits and reaches your personal bank accounts, retirement accounts, and property equity.

The cost of umbrella protection-typically $150 to $300 annually for $1 million in coverage-is negligible compared to the financial devastation a major liability claim inflicts. If you have children, employees, a pool, a trampoline, or host regular gatherings, your liability exposure rises significantly, making umbrella coverage essential rather than optional.

Boat and RV Owners in the Puget Sound Region

Boat and RV owners in the Puget Sound region face heightened liability risk that standard homeowners policies completely exclude. Your homeowner policy may have strict coverage limits or exclude boats and personal watercraft coverage altogether. RV owners face similar gaps since recreational vehicles aren’t covered under standard policies, yet a single accident involving your RV exposes you to substantial liability. These gaps leave you personally responsible for damages, medical costs, and legal defense expenses that can devastate your finances.

Landlords and Rental Property Owners

Landlords with rental properties in Kitsap need umbrella coverage even more urgently than owner-occupants because tenants and their guests sue for injuries on your property, and the average landlord property damage claim in 2022 exceeded $9,800. Multi-property landlords face compounded exposure since a single incident at any rental property triggers claims, and without adequate underlying coverage limits-at least $500,000 per occurrence plus loss-of-rent protection-your umbrella policy may not activate properly. Washington’s pure comparative negligence laws mean you face liability even if you’re partially at fault, so $1 million to $2 million in umbrella coverage represents a practical minimum for landlords managing multiple properties or high-value rentals.

An independent agency representing multiple carriers can structure your underlying coverage and umbrella limits to work together effectively, ensuring proper coordination when claims occur. The right combination of base policies and umbrella protection transforms your liability exposure from a financial threat into a manageable risk. Understanding how much coverage you actually need depends on your specific situation-which brings us to the next critical step: assessing your liability exposure and comparing coverage options that fit your assets and lifestyle.

Selecting Your Umbrella Limit and Building Your Coverage Stack

Assess Your Actual Liability Exposure

Choosing the right umbrella policy starts with a brutally honest assessment of what you own and what a lawsuit could cost. Most Kitsap residents dramatically underestimate their liability exposure. The Washington State Office of the Insurance Commissioner recommends starting with at least $500,000 in underlying homeowners liability if you own a property worth more than $400,000, and raising that to $1 million if you have rental properties, host gatherings regularly, or own a boat. Your umbrella policy then sits on top of these limits. If you own a primary residence worth $600,000 plus a rental property, your net worth exposure is substantial enough to justify $1 million to $2 million in umbrella coverage.

The math is straightforward: a single serious injury claim in the Puget Sound region routinely exceeds $500,000 when medical costs, lost wages, and pain-and-suffering damages combine. Most carriers require minimum underlying limits before issuing umbrella coverage-typically $300,000 in homeowners liability and $250,000 in auto liability-so you cannot simply purchase umbrella protection in isolation.

Calculate the True Cost of Umbrella Protection

Umbrella policies cost remarkably little. For $1 million in coverage, you pay $150 to $300 annually when bundled with existing policies. Raising your underlying homeowners deductible from $1,000 to $2,500 reduces your base policy premium by 8 to 15 percent, which often offsets the cost of adding umbrella protection entirely. This trade-off makes financial sense if you maintain adequate cash reserves to cover the higher deductible.

Shop Multiple Carriers and Compare Rates

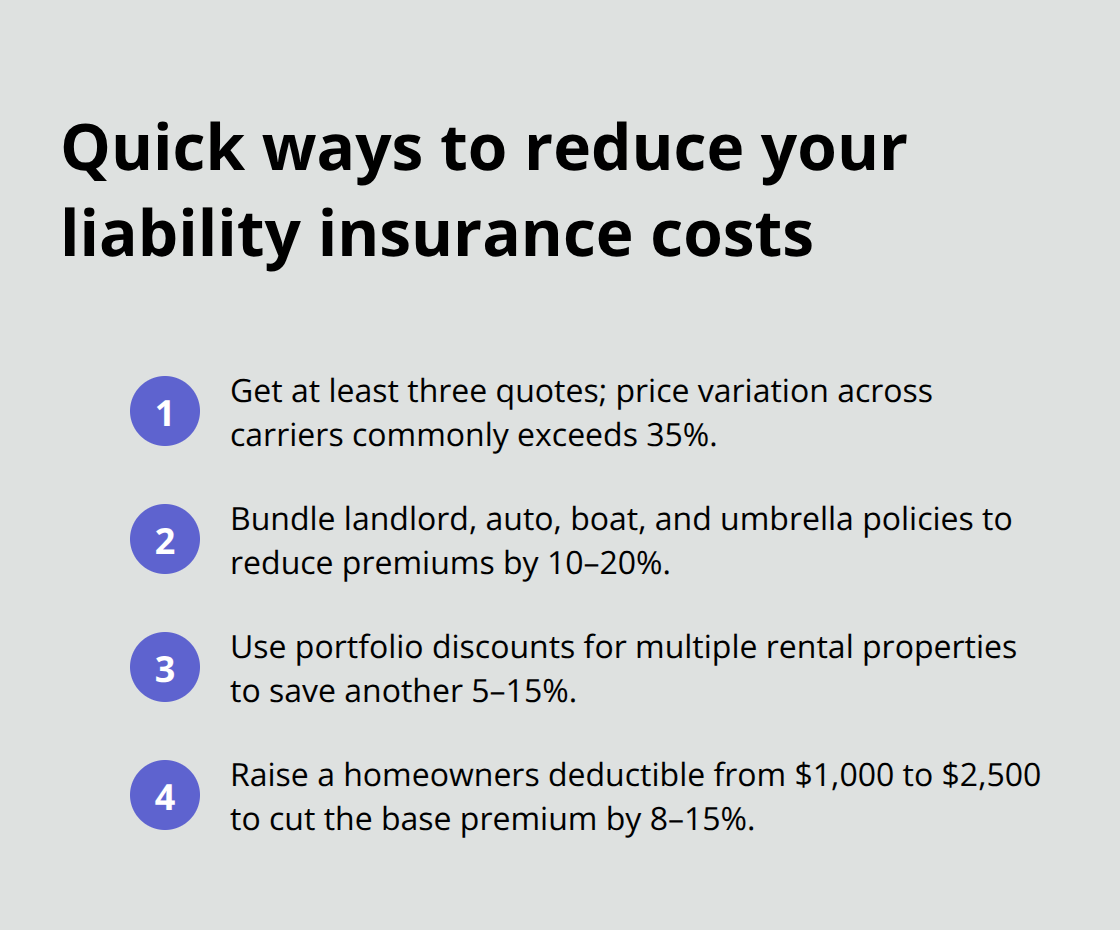

The practical next step is to obtain at least three quotes using identical property details, because price variation across carriers commonly exceeds 35 percent. Bundling landlord coverage with auto, boat, or umbrella policies reduces total premiums by 10 to 20 percent, and portfolio discounts for multiple rental properties cut costs another 5 to 15 percent. An independent agency representing multiple carriers-rather than a single company-gives you the ability to compare options side by side and identify which carrier offers the best rates for your specific risk profile.

Evaluate Carrier Strength and Local Expertise

When evaluating carriers, look for an AM Best rating of A- or higher and check JD Power claim-satisfaction scores to confirm they actually pay claims quickly when accidents happen. Specialized Puget Sound landlords insurers are typically more responsive to regional hazards like earthquakes and floods than national carriers that lack local market knowledge. If you rent to short-term tenants through platforms like Airbnb, premiums jump 20 to 40 percent higher and many standard carriers exclude this activity entirely without specialized riders.

Coordinate Your Coverage Layers

An independent agency representing multiple top local and national carriers can customize packages that bundle your homeowners, auto, boat, and umbrella coverage together at competitive rates while ensuring your underlying limits coordinate properly with your umbrella policy. This coordination matters because your umbrella activates only after your underlying policies exhaust their limits, so misaligned coverage creates gaps that leave you exposed.

Final Thoughts

Umbrella insurance protects the assets you’ve worked hard to build by covering liability costs that standard homeowners and auto policies leave exposed. In Kitsap, where waterfront properties, boating culture, and multi-property ownership create elevated risk, Kitsap umbrella coverage transforms a financial vulnerability into manageable protection. A single serious injury claim or lawsuit can exceed your underlying policy limits by hundreds of thousands of dollars, forcing you to liquidate savings, retirement accounts, and property equity to cover the difference.

The right approach combines adequate underlying limits with umbrella protection structured to work together seamlessly. This means raising your homeowners liability to at least $500,000 if you own meaningful assets, ensuring your auto coverage meets minimum thresholds, and then layering umbrella protection on top. Landlords managing rental properties need even stronger protection because tenants and their guests sue for injuries, and Washington’s comparative negligence laws mean you face liability exposure regardless of fault percentage.

We at H&K Insurance Agency help Kitsap residents and Puget Sound families structure coverage that actually protects their wealth. Visit handkinsurance.com to assess your liability exposure and build the protection your assets deserve.