Puget Sound RV Insurance: Tailored Auto Coverage For Your Mobile Life

Your RV is more than just a vehicle-it’s your home on wheels. Standard auto insurance falls short when it comes to protecting what makes your mobile lifestyle unique.

At H&K Insurance Agency, we know that Puget Sound RV insurance needs to cover risks that traditional policies simply don’t address. This guide walks you through the coverage gaps, the right questions to ask, and how to build protection that actually fits your life on the road.

Why Your RV Needs Different Protection Than Your Car

Standard auto insurance won’t protect your RV because it’s fundamentally different from a sedan or truck. Washington state requires motorhomes to carry minimum liability coverage of $25,000 bodily injury per person, $50,000 per accident, and $10,000 property damage-but these minimums barely scratch the surface of what you actually need. A typical motorhome costs $80,000 to $200,000 or more, and your living space inside contains personal belongings worth thousands. Standard auto policies exclude coverage for attached structures like awnings and satellite dishes, personal property stored inside, or the full replacement cost of your RV if it’s totaled. Travel trailers face similar gaps: your auto liability covers the towing vehicle, but not damage to the trailer itself. This means a collision, theft, or weather event could leave you without a home and without compensation. Progressive reported that in 2023, the average Washington motorhome premium was about $824.12 annually, while travel trailers averaged $403.21-but these figures reflect basic coverage. Full-timers living in their RVs year-round face exposure that part-time users don’t encounter.

Motorhomes Demand Higher Liability Limits

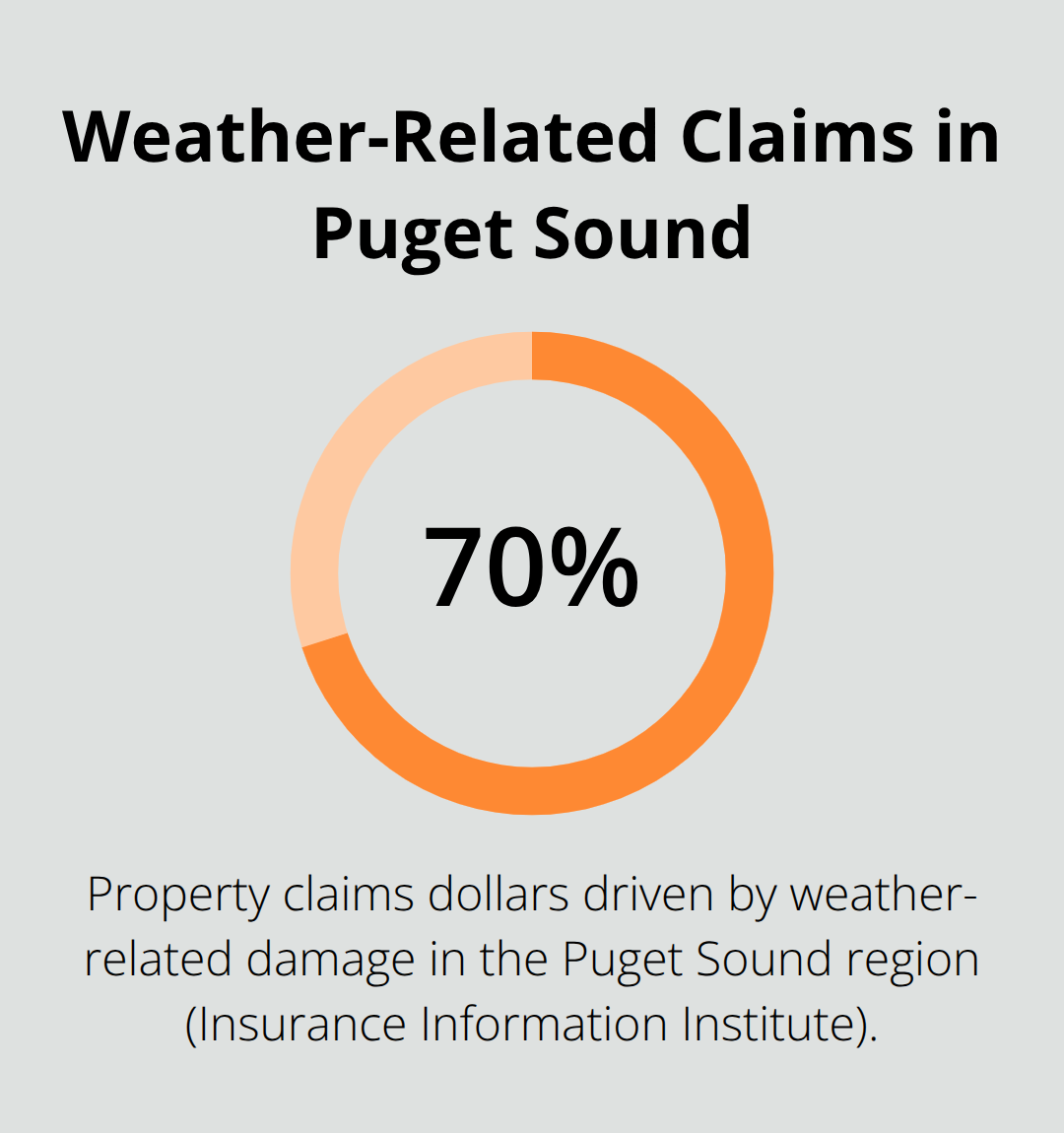

Motorhomes present unique liability risks that standard auto policies can’t address. If someone is injured at your campsite, slips on your awning, or is hurt while you’re parked, your standard auto liability won’t cover it. Liability limits of at least $1 million protect motorhome owners far better than the state minimum, because injury claims involving your living space can escalate quickly. Comprehensive coverage becomes essential in the Puget Sound region, where weather-related damage accounts for approximately 70% of property claims dollars according to the Insurance Information Institute.

Winter winds exceeding 65 mph regularly hit King and Pierce Counties, making comprehensive protection against weather, theft, and vandalism non-negotiable. Full-time RV policies should include emergency expense coverage that reimburses lodging or transportation costs if your motorhome breaks down more than 50 miles from home, with full-timers’ policies typically covering up to $7,500.

Travel Trailers Require Separate Protection

Travel trailers require different thinking entirely. Your auto policy’s liability extends to the trailer while you’re towing, but stops there. Comprehensive and collision coverage for the trailer itself is optional if you own it outright, but financially risky if you don’t have it. Comprehensive covers theft, vandalism, fire, animal collisions, and weather damage-all real threats in Washington’s varied climate. Collision coverage pays for damage from accidents with other vehicles or objects. If your trailer is financed, lenders typically require comprehensive coverage. Personal property coverage becomes critical because camping gear, electronics, and household items stored in your trailer aren’t covered by standard auto insurance. Adjacent structures coverage protects attached items like satellite dishes, awnings, and exterior equipment that standard policies exclude entirely. Loss assessment coverage protects you if your RV park or campground assesses residents for damage to shared property-a real cost in Puget Sound parks where infrastructure damage from storms affects the entire community.

What Happens When You Underestimate Your Coverage

Many RV owners discover coverage gaps only after a loss occurs. You might assume your homeowners policy covers personal belongings in your trailer, but it doesn’t-homeowners policies exclude vehicles and their contents. You might think your auto liability is enough, only to face a lawsuit that exceeds your limits. Weather events in the Puget Sound region expose these gaps quickly. A single winter storm can damage your awning, crack your roof, or cause water intrusion that standard policies won’t cover. The cost of replacing a motorhome roof or repairing structural damage runs into tens of thousands of dollars. Without the right coverage, you absorb these costs yourself. This is where independent agents who understand RV-specific risks make a real difference-they identify gaps before they become expensive problems.

Finding the Right RV Insurance for Your Needs

Match Your Coverage to Your Lifestyle

Your RV type and how you use it determine everything about the coverage you need. A full-time motorhome owner living year-round in their rig faces completely different risks than someone who takes weekend trips in a travel trailer. Start with honest self-assessment: Are you parked in one location for months, or do you move between campgrounds weekly? Do you rent out your RV to generate income, or do you keep it for personal use only? Are you towing a trailer behind a truck, or driving a motorhome where your living space moves with you?

Washington’s 2023 average premiums reflect this variation-motorhomes cost around $824 annually while travel trailers average $403-but these figures mask the real range. A liability-only policy might start around $125 yearly, while comprehensive motorhome coverage with emergency expense and personal property protection easily reaches $1,500 or more. Full-timers should prioritize emergency expense coverage that reimburses hotel and transportation costs if breakdowns strand you far from home, with full-timer policies covering up to $7,500.

This protection matters because Puget Sound’s winter storms regularly produce wind gusts exceeding 65 mph in King and Pierce Counties, creating unexpected repair situations where you’ll need immediate lodging. Comprehensive coverage becomes essential in this region where weather-related damage accounts for roughly 70% of property claims dollars according to the Insurance Information Institute.

Adjust Your Deductibles and Bundle Policies

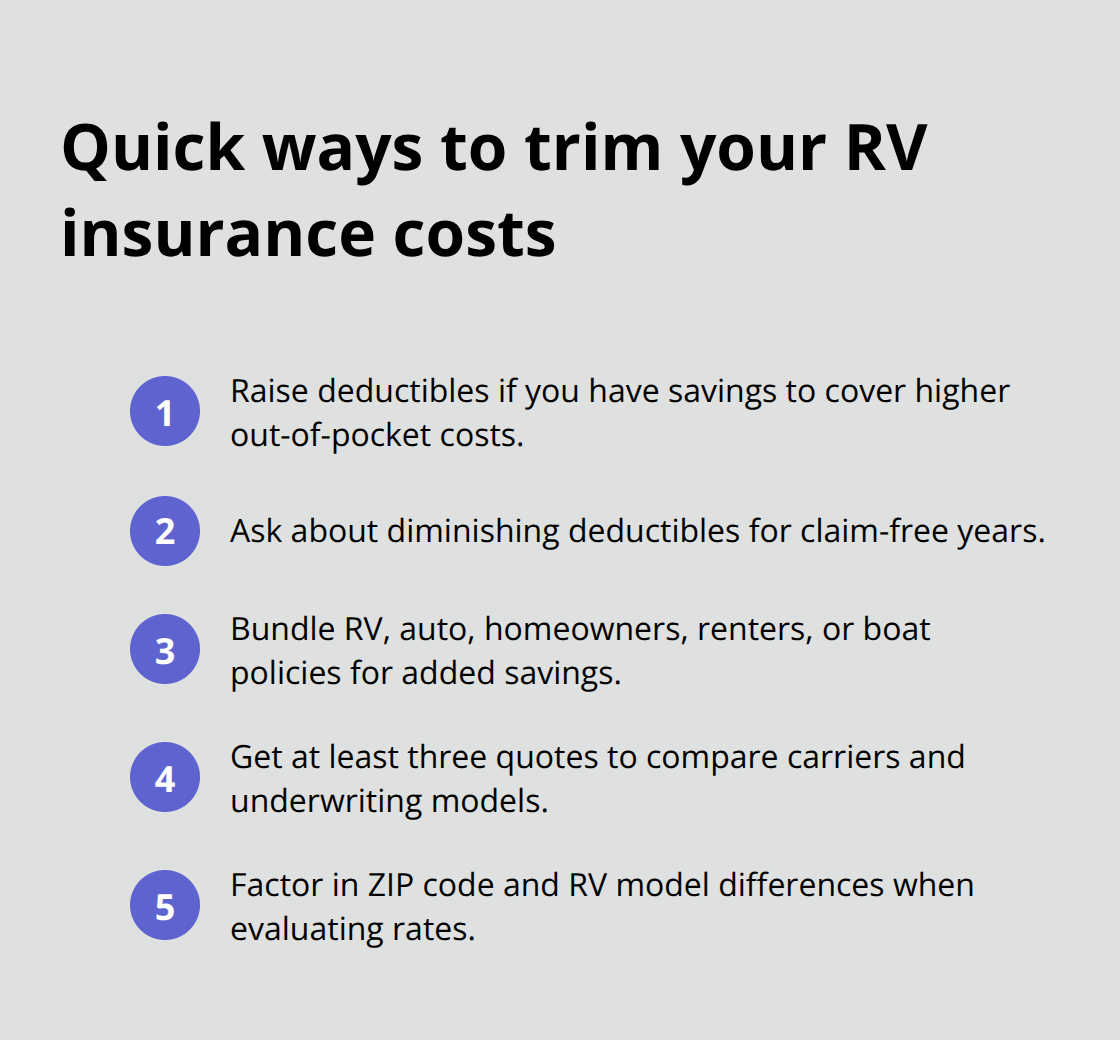

Standard deductibles run $500 to $1,000, but raising your deductible to $1,500 or $2,500 can cut your premium by 15 to 25 percent. This strategy works well if you have emergency savings to cover larger out-of-pocket costs. Some insurers offer diminishing deductibles that reduce your deductible amount for each claim-free year, rewarding safe RV owners over time.

Bundling RV insurance with auto, homeowners, renters, or boat policies typically saves 10 to 15 percent on your total premium. This represents the single most effective way to lower costs without cutting coverage. Shop at least three quotes before deciding, because rates vary dramatically by carrier, RV model, your driving record, and ZIP code within the Puget Sound region. A motorhome worth $150,000 with a clean driving record in one area might cost $900 annually while the same coverage in a different ZIP code runs $1,200 simply due to local loss history.

Add Coverage for Your Belongings and Attachments

Personal property coverage protects your camping gear and electronics inside the RV and typically costs $50 to $100 annually. This modest expense prevents thousands in losses if theft or weather damage occurs. Adjacent structures coverage for awnings and satellite dishes adds another $30 to $50 yearly and proves worth every penny given Puget Sound’s high wind exposure.

These targeted additions address real gaps that standard auto policies leave wide open. Your personal belongings inside the RV aren’t covered by homeowners insurance, and your awning or satellite dish won’t be covered by basic auto liability. The Puget Sound region’s exposure to severe weather makes these protections practical necessities rather than optional upgrades.

Get Quotes From Multiple Carriers

H&K Insurance Agency represents multiple top carriers, allowing you to compare actual quotes across companies rather than guessing which offers the best rate for your specific RV and situation. This independent approach means you access different underwriting criteria and pricing models that can produce significant savings. The right carrier for your motorhome might differ from the right carrier for your travel trailer, and only direct comparison reveals these differences.

Your next step involves identifying which coverage gaps matter most for your specific situation and lifestyle.

Common RV Insurance Gaps and How to Avoid Them

Liability Limits That Actually Protect Full-Time RV Owners

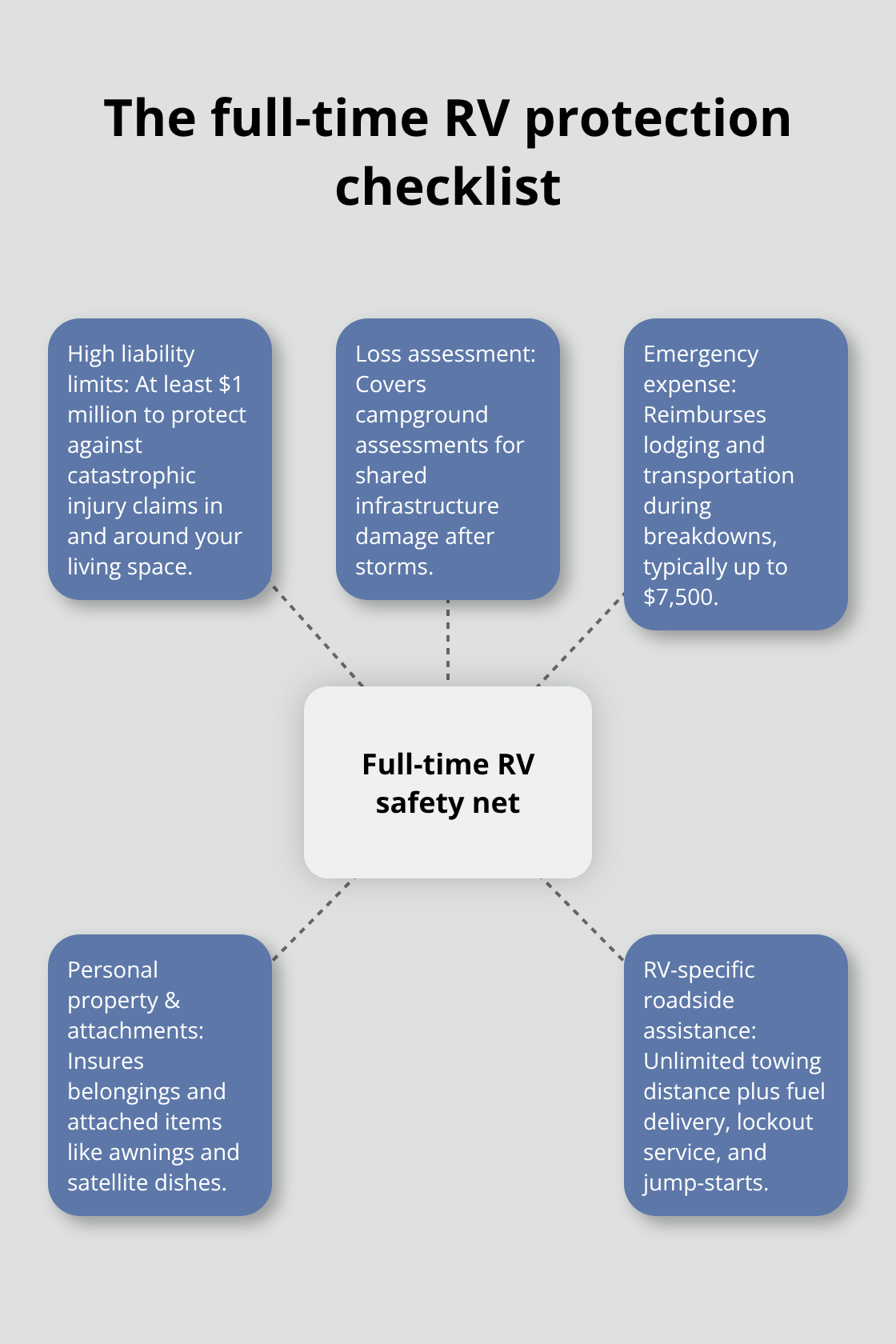

Full-time RV living exposes you to liability scenarios that weekend warriors never face. When you live in your motorhome year-round, someone could slip on your exterior steps, suffer an injury inside your living space, or get hurt at a campground where you park for months. Washington’s state minimum liability requires auto liability coverage for vehicles pulling travel trailers. Medical bills for a serious injury easily exceed $100,000, and if the injured party sues, they pursue assets beyond the state minimum. Full-timers need at least $1 million in liability coverage to protect against catastrophic claims that standard minimums won’t touch. Campground slip-and-fall injuries happen regularly, and Puget Sound’s wet winters create hazardous conditions around RV sites. This isn’t theoretical risk-it’s a practical reality for anyone living full-time in their motorhome.

Loss Assessment and Emergency Expense Coverage

Loss assessment coverage matters equally for full-timers because RV parks and campgrounds frequently assess residents for damage to shared infrastructure after storms. A single winter wind event that damages roads, utility lines, or common structures can trigger assessments of $500 to $2,000 or more per lot. Without loss assessment coverage, you pay these costs directly from your pocket. Emergency expense coverage that reimburses lodging and transportation if your motorhome breaks down becomes essential when you live full-time in your RV. Full-timer policies typically cover up to $7,500 in emergency expenses, which covers hotel stays and vehicle rentals during major repairs. In Puget Sound’s climate, where winter storms regularly produce wind gusts exceeding 65 mph in King and Pierce Counties, breakdowns during severe weather aren’t hypothetical-they’re inevitable for long-term RV residents.

Personal Property and Attached Structures Protection

Your personal belongings inside the RV and attached structures require separate protection that standard auto policies completely ignore. Camping gear, electronics, kitchen equipment, and clothing stored in your motorhome aren’t covered by your auto liability or your homeowners policy. Adjacent structures coverage protects awnings, satellite dishes, exterior storage boxes, and slide-out awnings that face constant exposure to Puget Sound’s harsh weather. This coverage typically costs $30 to $50 annually and prevents thousand-dollar losses from wind damage or weather deterioration.

Roadside Assistance for Remote Breakdowns

Roadside assistance and towing coverage becomes your lifeline when mechanical failures strand you far from home. Standard auto roadside assistance often caps towing at 50 or 75 miles, which leaves you vulnerable if you travel through remote areas of Washington or beyond state lines. RV-specific roadside assistance typically covers unlimited towing distance and includes fuel delivery, lockout service, and jump-starts tailored to motorhome needs.

For full-timers, this coverage prevents situations where a transmission failure 200 miles from home leaves you paying $3,000 to $5,000 in towing costs out of pocket. The combination of liability limits, loss assessment coverage, emergency expenses, personal property protection, and roadside assistance creates the safety net that actual full-time RV living demands.

Final Thoughts

RV insurance in the Puget Sound region demands more than state minimums and generic auto policies. You need liability limits that protect against catastrophic claims, comprehensive coverage for weather damage that accounts for 70% of property losses in this region, and specialized protections for personal belongings and attached structures that standard policies exclude entirely. Full-time RV living requires emergency expense coverage that reimburses lodging during breakdowns, loss assessment protection for campground infrastructure damage, and roadside assistance that covers unlimited towing distances.

We at H&K Insurance Agency understand these distinctions because we work with RV owners throughout the Puget Sound region every day. As an independent agency, we represent multiple top carriers, which means we compare actual quotes across different underwriting criteria rather than steering you toward a single option. This approach reveals which carriers offer the best rates for your specific motorhome or travel trailer, your driving record, and your ZIP code.

Your next step is straightforward: contact H&K Insurance Agency and compare what different carriers offer for your situation. Bring details about your RV type, how you use it, and whether you live full-time or travel seasonally, and we’ll identify which coverage gaps matter most for your lifestyle and build Puget Sound RV insurance protection that actually fits your mobile life.