Condo Insurance Options: Tailored Coverage for Your Unit

Condo ownership comes with unique insurance needs that differ from traditional homeownership. Your unit requires specific protection that goes beyond what your building’s master policy covers.

We at H&K Insurance Agency help condo owners navigate the various condo insurance options available to them. This guide breaks down exactly what you need to know to protect your investment.

What Your Condo Insurance Actually Protects

Condo insurance splits into three distinct protection zones, and understanding where each applies matters more than most condo owners realize. Your HO-6 policy covers the interior of your unit, your personal belongings, and your liability if someone gets hurt because of you. The condo association’s master policy handles the building exterior, roof, and common areas. This separation creates gaps that trip up unprepared owners, so you need to know exactly what lands on your shoulders.

Interior dwelling coverage starts where the master policy stops

The master policy typically covers bare walls, floors, and ceilings in common areas, but your unit’s interior is your responsibility. This means your walls, built-in cabinets, hardwood flooring, kitchen counters, and bathroom fixtures all need coverage under your HO-6 dwelling protection. Interior dwelling coverage protects the interior structure from the walls inward. If your HOA has all-in coverage instead of bare walls coverage, some of these items might already be protected, but you cannot assume this without reviewing your master policy document directly. The Insurance Information Institute notes that many owners underestimate replacement costs for interior improvements, leading to significant out-of-pocket expenses after a loss. You should obtain an appraisal of your unit’s interior condition and replacement cost, then match your dwelling coverage to that number. Actual quotes from contractors in your area provide the accuracy you need to avoid being underinsured.

Personal property coverage protects your belongings, but limits apply

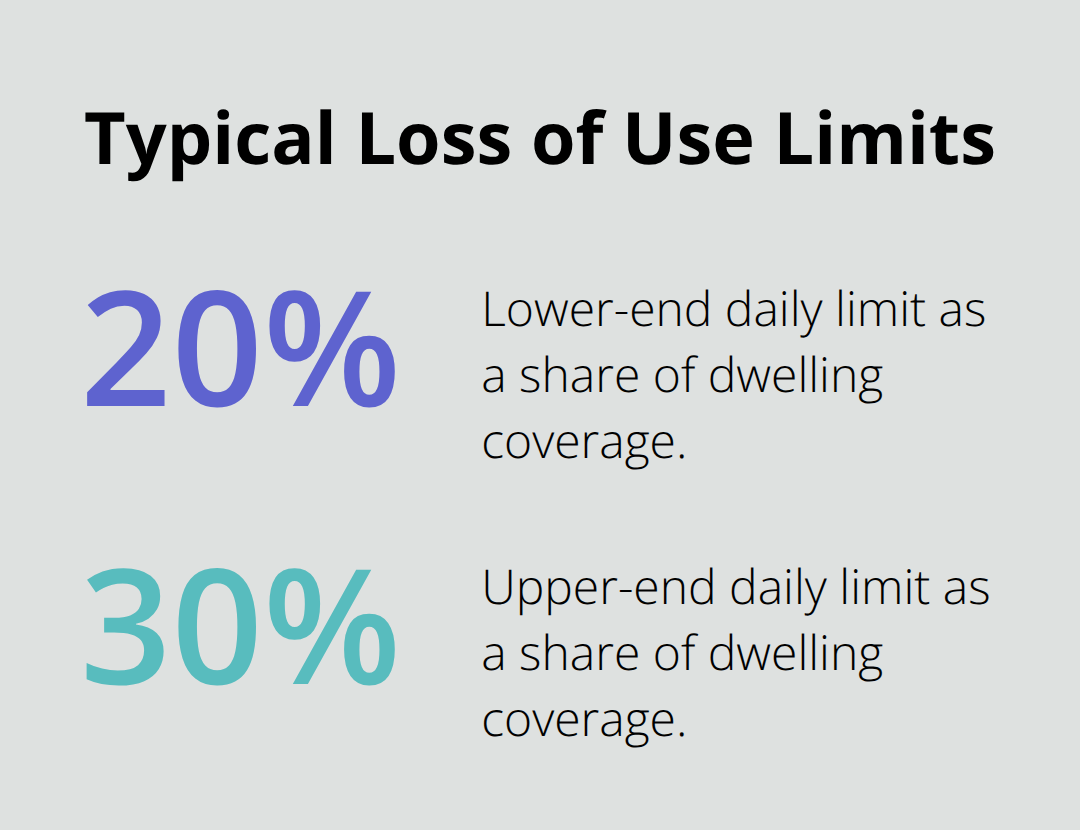

Your furniture, electronics, clothing, and other movable items fall under personal property coverage, which reimburses replacement costs for items damaged or stolen from named perils. Standard HO-6 policies typically reimburse depreciated value unless you add a replacement cost endorsement, which means a five-year-old television receives payment at a fraction of its original price. High-value items like jewelry, art, or firearms often hit policy limits around 50 to 75 percent of the item’s value, so valuable collections need scheduled personal property endorsements with appraisals to guarantee full replacement cost. You should create a detailed home inventory now, photograph items, and store the list outside your home. This simple step eliminates disputes when you file a claim and ensures you request adequate coverage limits upfront. Loss of use coverage also sits here, reimbursing hotel stays, meals, and other temporary living expenses if your unit becomes uninhabitable after a covered event, typically with daily limits around 20 to 30 percent of your dwelling coverage.

Liability coverage protects you from lawsuits and injury claims

If someone slips on your unit’s floor and breaks a leg, or your guest damages a neighbor’s property, your personal liability coverage pays for medical bills, legal defense, and settlements up to your policy limit. Most condo owners start with 100,000 dollars in liability protection, but that limit may not adequately shield someone with significant assets or rental income. Medical payments to others coverage, separate from liability, pays up to around 1,000 dollars per person for injuries on your property without requiring fault, making it valuable for preventing small incidents from becoming disputes. Loss assessment coverage handles your share of HOA special assessments when the master policy exceeds its limits or deductible after damage to common areas, with limits typically ranging from 1,000 to 25,000 dollars. An umbrella policy adds another layer of liability protection beyond your HO-6 limits, often providing 1 million dollars in additional coverage for reasonable annual premiums, making it smart protection if your unit appreciates significantly or you rent it out.

Understanding these three protection zones sets the foundation for selecting the right policy type. The next section walks through the specific policies available to condo owners and how each one fits into your overall protection strategy.

Which Policy Type Protects Your Condo

HO-6 policy covers personal liability, damage to your condo unit and belongings, and additional living expenses if a covered incident forces you to leave your home. An HO-6 policy covers only your unit’s interior and personal belongings, not the building structure itself, which means it fills specific gaps that the condo association’s master policy deliberately leaves uncovered. The master policy, funded through your HOA fees, protects common areas and the building exterior, but it stops at your unit’s walls. This separation of responsibility means you cannot skip HO-6 coverage and expect the master policy to protect you-they work together as complementary layers, not replacements. Most mortgage lenders require HO-6 coverage before closing, and many HOAs enforce minimum coverage levels in their bylaws, so you have limited flexibility here.

Master Policy Types Determine Your Coverage Gaps

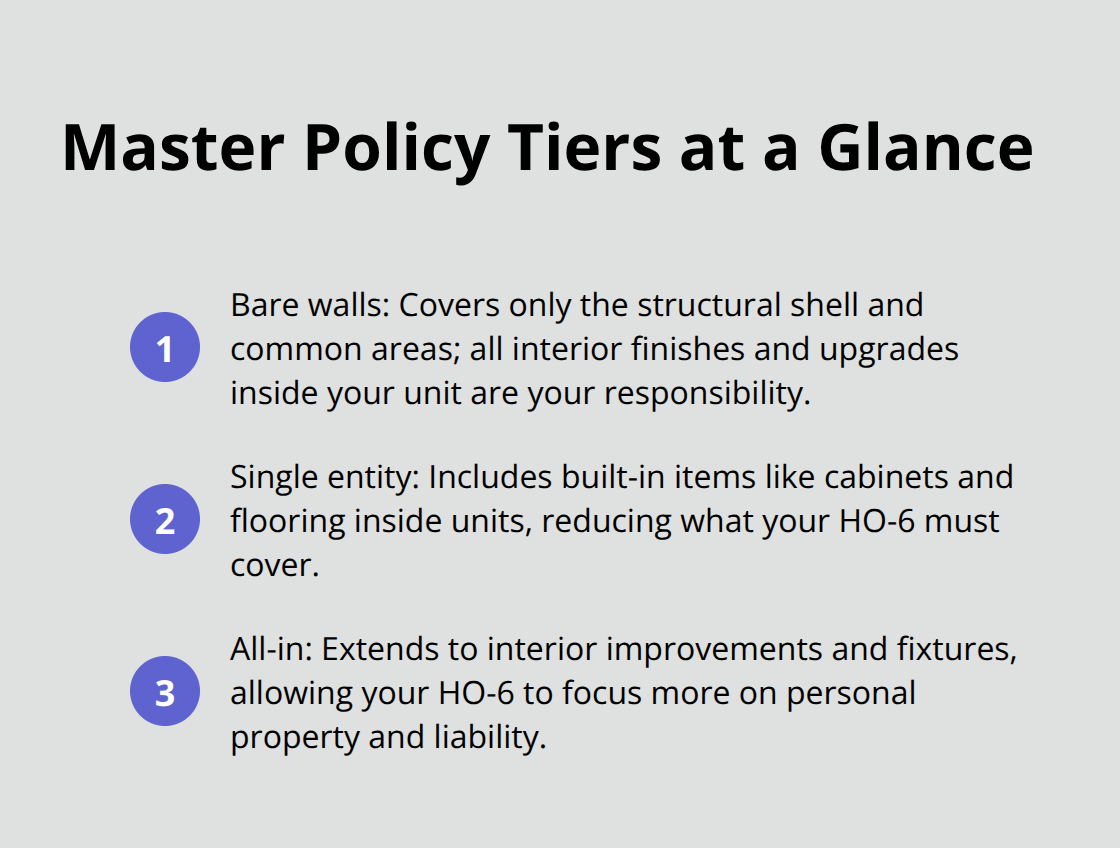

Your condo association’s master policy type directly determines what dwelling coverage your HO-6 needs to provide. Bare walls coverage, the most basic master policy tier, protects only the structural shell and common areas, leaving you responsible for all interior finishes, fixtures, and improvements inside your unit. Single entity coverage adds protection for built-in items like cabinets and flooring within units, reducing what you need to cover individually. All-in coverage represents the most comprehensive master policy option, covering interior improvements and built-in fixtures, which means your HO-6 dwelling coverage can focus primarily on personal property and liability rather than interior structure.

You must obtain a copy of your master policy document and identify exactly which tier your HOA carries-this step is not optional if you want adequate protection.

Endorsements and Riders Customize Your Protection

Additional riders and endorsements transform your base HO-6 into targeted protection that matches your specific situation. Replacement cost endorsements for personal property pay full replacement value instead of depreciated amounts, costing modestly more but protecting newer belongings from steep depreciation losses. Scheduled personal property endorsements with appraisals guarantee full replacement value for high-value items like jewelry, art, or firearms that standard policies typically limit to 50 to 75 percent of actual value. Water backup coverage addresses damage from clogged drains or sump pump failures that standard policies exclude, identity theft protection covers legal fees and recovery costs after fraud, and earthquake coverage becomes essential in high-risk areas since standard condo policies categorically exclude this peril. Waiting until after a loss to discover coverage gaps costs far more than the modest annual rider premiums.

The specific endorsements you add depend on your unit’s condition, your personal property value, and your area’s natural disaster risks. Once you understand which policy type and endorsements fit your situation, the next step involves comparing actual quotes from multiple carriers to find the coverage and price combination that protects your investment without overpaying.

Selecting the Right Coverage for Your Situation

Choosing condo insurance requires three concrete steps that most owners skip, then regret after a claim reveals massive gaps in their protection. You must measure what you actually own and what your unit actually costs to repair, then cross-reference that against your master policy’s scope, and finally compare multiple carriers for real pricing. Skipping any of these steps leaves you guessing, and guessing wrong costs thousands when damage happens.

Get a Professional Appraisal of Your Interior Costs

A professional appraisal of your unit’s interior replacement cost beats generic online calculators by miles. Your walls, flooring, kitchen, bathrooms, and built-in fixtures all cost real money to replace at current market rates, not 2015 prices. Contractor estimates in your area provide the accuracy you need to request appropriate quotes and avoid underinsurance that surfaces after claims arrive.

Document Your Personal Property with Photos and Lists

You should document every item you own by category-furniture, electronics, clothing, jewelry-and photograph high-value pieces. This inventory forms the basis for your personal property limit and catches underinsurance before claims arrive. Store your list outside your home so fire or theft cannot destroy your documentation when you need it most.

Review Your Condo Association’s Master Policy Document

Obtain your condo association’s master policy document and identify whether your HOA carries bare walls, single entity, or all-in coverage, because this determines whether your HO-6 needs to cover interior structure or just your belongings and liability. Many owners never read their master policy, then discover after a loss that they duplicated coverage they already had or missed coverage gaps they thought were included. Standard condo policies exclude flood damage entirely, so if your building sits in a flood zone or even a moderate-risk area, flood insurance through the National Flood Insurance Program or private carriers becomes non-negotiable.

Compare Quotes from Multiple Carriers with Identical Coverage

Request quotes from at least three carriers using identical coverage limits and deductibles so you compare apples to apples. The average condo insurance cost runs around $490 annually according to NerdWallet rate analysis, but your specific premium depends on location, unit value, and chosen deductibles. Higher deductibles reduce premiums significantly, but only if you actually have savings set aside to cover that deductible after a loss-choosing a $1,000 deductible when you have $500 in emergency funds creates a trap.

Ask each carrier about multi-policy bundling discounts with auto insurance, safety equipment discounts for alarm systems or fire detectors, and claim-free discounts that can slash your premium by 10 to 25 percent.

Work with an Independent Agent to Simplify Your Search

An independent agent representing multiple top carriers can compare rates across providers and customize packages that match your unit’s actual needs rather than offering generic policies that leave you exposed. This approach saves you time and helps you identify coverage gaps before losses occur.

Final Thoughts

Condo insurance protects what matters most about your unit-the interior you’ve invested in, the belongings you own, and your financial security if someone gets injured because of you. The condo association’s master policy handles the building shell and common areas, but your HO-6 policy fills the gaps that matter to your daily life. Understanding this split responsibility prevents the costly mistakes that catch unprepared owners after losses occur.

Your next move is straightforward: obtain your master policy document and identify whether your HOA carries bare walls, single entity, or all-in coverage, get a professional appraisal of your unit’s interior replacement cost rather than guessing, and document your personal belongings with photos and lists stored outside your home. Then request quotes from multiple carriers using identical coverage limits so you compare real pricing, not generic estimates. Ask about bundling discounts, safety equipment discounts, and claim-free discounts that can meaningfully reduce your premium.

We at H&K Insurance Agency specialize in helping condo owners navigate these decisions and find the condo insurance options that match their actual needs. As a locally owned, independent agency serving the Puget Sound region, we represent multiple top carriers and customize packages rather than offering generic policies that leave you exposed. Contact us today to get quotes that protect your investment without overpaying, and let our team handle the complexity so you can focus on enjoying your condo.