Condo Insurance Seattle WA: Guard Your Strata With Smart Coverage

Condo insurance in Seattle, WA protects your unit and belongings in ways your HOA’s master policy simply cannot. Most condo owners discover gaps in coverage only after a claim gets denied.

We at H&K Insurance Agency help Seattle residents understand exactly what they need to cover and what their HOA already handles. The right policy keeps your investment safe from the region’s specific risks.

What Your Condo Insurance Actually Covers

Dwelling Coverage Protects Your Interior Upgrades

Your condo insurance policy covers three critical areas that your HOA’s master policy will not. First, dwelling coverage protects the interior structure of your unit, including built-in appliances, cabinets, flooring, and any upgrades you’ve installed. This protection is essential because the master policy covers only the building’s exterior walls and common areas. If you’ve renovated your kitchen or installed hardwood floors, those improvements belong to you and require your individual coverage.

Personal Property Protection Shields Your Belongings

Second, personal property protection reimburses you for furniture, electronics, clothing, and other belongings inside your unit. Protecting your possessions against leaks, burst pipes, and storm damage matters significantly. Most standard policies pay actual cash value rather than replacement cost, meaning your five-year-old television is worth far less than a new one. Adding replacement cost endorsements costs extra but eliminates depreciation deductions after a loss.

Liability Coverage Protects You From Guest Injuries

Third, liability coverage protects you if a guest is injured in your unit or if you accidentally damage someone else’s property. This coverage is essential rather than optional.

Master Policy Type Determines Your Coverage Needs

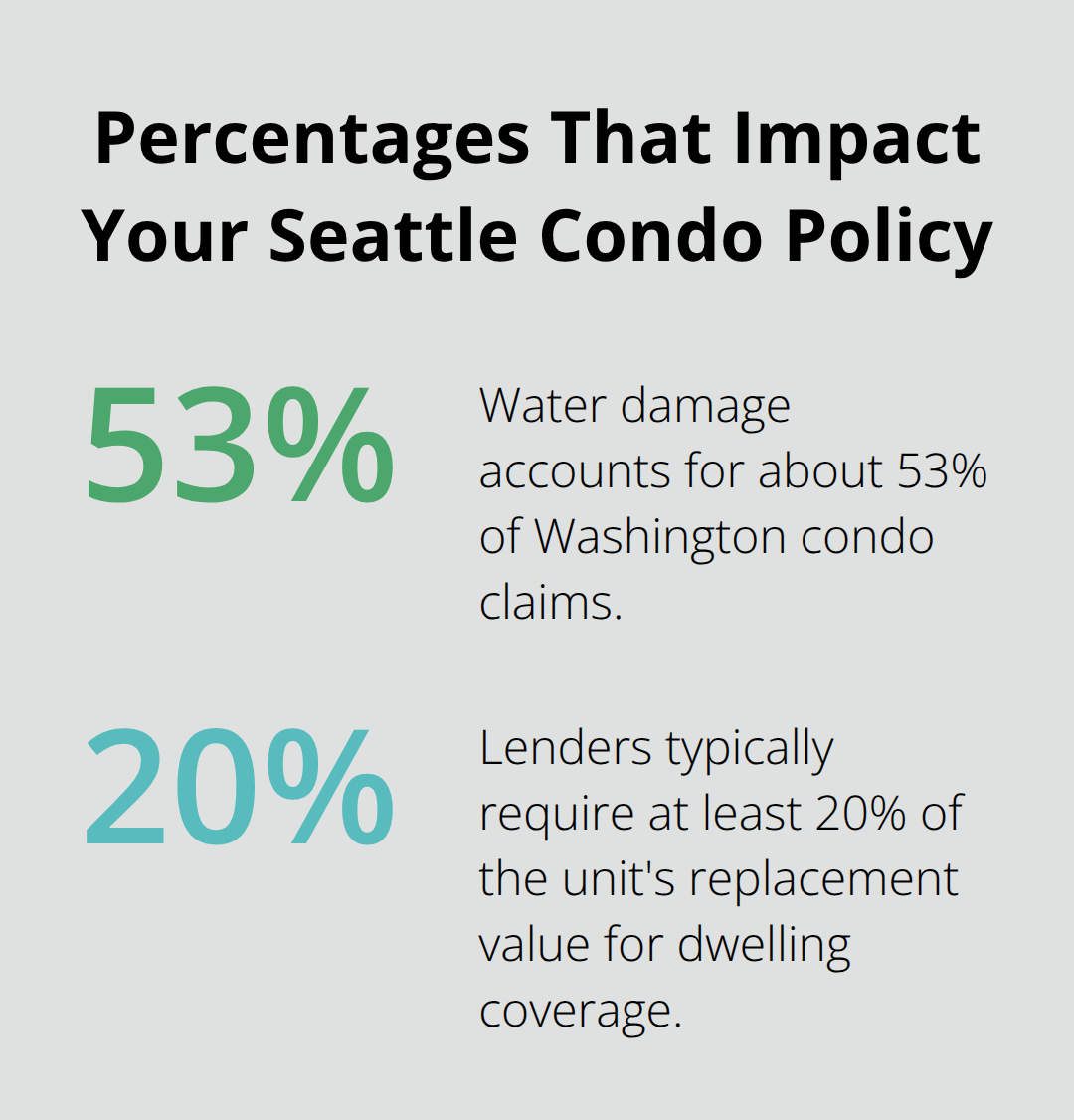

Understanding what sits between your policy and the master policy prevents costly gaps. If your HOA carries an All-Inclusive master policy, it covers common areas and restores your unit to pre-damage condition, meaning your HO-6 dwelling coverage needs less depth. If your HOA carries a Bare Walls policy, you must cover significantly more interior structure yourself, including all fixtures and appliances. Many Seattle condo owners underestimate their dwelling coverage limits because they don’t account for replacement costs of renovations. Your lender typically requires dwelling coverage at least 20% of your unit’s replacement value, but that baseline is often inadequate.

Loss Assessment Coverage Protects Against Special Levies

Loss assessment coverage is optional but worth serious consideration because your HOA can levy special assessments against all owners when the master policy deductible or limits fall short after a major loss. This protection (which many owners overlook) can save you thousands when the association faces unexpected repair bills. The next section walks you through how standard homeowners policies fail to address the unique risks that Seattle condo owners face.

Why Standard Condo Coverage Leaves You Exposed in Seattle

The Master Policy Covers Only the Building, Not Your Unit

Your HOA’s master policy covers the building’s structure and common areas, but it explicitly excludes your interior finishes, personal belongings, and liability within your unit. This separation creates real gaps that leave owners vulnerable. If water damage from a burst pipe destroys your kitchen cabinets and flooring, the master policy won’t pay for those improvements because they’re considered your responsibility as the unit owner. Similarly, if a guest slips on your wet bathroom floor and files a lawsuit, the master policy’s liability coverage doesn’t apply to incidents inside individual units.

Many Seattle condo owners assume their HOA’s insurance handles everything, then face thousands in out-of-pocket costs after a claim. The master policy typically covers only two things: the building’s physical structure and liability for common areas like hallways and lobbies. Anything beyond those boundaries falls on you, which is why an HO-6 policy specifically designed for condo units is non-negotiable.

Earthquake Risk Threatens Your Investment Without Proper Coverage

The Puget Sound region presents earthquake risks that standard condo policies exclude entirely. Washington experiences frequent seismic activity, yet state law does not mandate earthquake coverage for condo associations, leaving owners exposed to potentially catastrophic losses. A moderate earthquake can cause foundation damage, cracked walls, and broken utilities that neither your HO-6 nor the master policy covers without an explicit endorsement.

Your HOA’s master policy likely excludes earthquake damage as well, meaning a major event could leave the entire building unrepaired. Adding earthquake coverage requires a separate endorsement and carries a deductible of 5–20% of insured value, but the protection prevents financial devastation when the ground shifts beneath your Seattle home.

Flood Damage Requires Separate Insurance You Cannot Delay

Flood risk is equally serious in Seattle neighborhoods near Puget Sound, the Green River, and Duwamish River, where spring runoff and heavy rainfall regularly cause water damage claims. Standard condo policies do not cover flood losses, period. If your unit sits in a flood zone or even a flood-adjacent area, you need separate flood insurance through the National Flood Insurance Program, which requires a 30-day waiting period before coverage takes effect.

Many owners purchase flood coverage only after a loss, then discover they cannot. This timing mistake costs thousands. Water damage represents about 53% of condo claims in Washington, making flood protection essential rather than optional for properties in vulnerable areas.

Maintenance Failures and Wear-and-Tear Gaps

Your HOA’s master policy also excludes wear-and-tear maintenance items like failed HVAC systems, roof leaks from age, or plumbing corrosion, so owners cannot rely on insurance for routine building failures. These exclusions mean you must budget separately for preventive maintenance and repairs that fall outside insurance coverage. Understanding what your master policy actually covers (and what it doesn’t) prevents costly surprises when damage strikes your unit.

The gaps between your HO-6 policy and the master policy create exposure that most Seattle condo owners don’t recognize until it’s too late. Choosing the right coverage requires understanding your specific HOA structure and the risks unique to your neighborhood.

How to Choose the Right Condo Insurance Plan

Start With Your HOA’s Certificate of Insurance

Obtain your HOA’s Certificate of Insurance immediately-this document reveals exactly what the master policy covers, its limits, and deductibles. The certificate shows whether your association carries an All-Inclusive, Single Entity, or Bare Walls policy structure, and each type determines how much dwelling coverage you personally need. If your HOA carries a Bare Walls policy, you’re responsible for all interior fixtures and appliances, meaning your dwelling coverage limit must account for full replacement costs of cabinets, flooring, and built-in systems. If your association chose All-Inclusive coverage, your personal dwelling needs drop significantly because the master policy handles most interior restoration.

Contact your HOA president or property manager directly if the Certificate doesn’t clarify which structure applies to your building. Many Seattle owners skip this step and purchase inadequate coverage, then face massive out-of-pocket costs after a claim.

Calculate Your True Replacement Cost

Your lender requires dwelling coverage at minimum 20% of replacement value, but that baseline misses most renovation costs. List every upgrade you’ve made since purchase-kitchen remodels, flooring replacements, bathroom updates-and add 15% for inflation. That number should drive your Coverage A limit selection, not your lender’s minimum requirement. This calculation prevents underinsurance when a loss strikes your unit.

Compare Quotes Across Multiple Carriers

Comparing quotes from multiple carriers matters far more than shopping price alone, especially for condo coverage where policy language varies significantly between insurers. Independent agents can access dozens of carriers and tailor quotes to your specific master policy structure, whereas direct insurers typically offer only one product.

Request quotes that specify exactly what dwelling coverage includes, whether personal property uses replacement cost or actual cash value, and what deductibles apply to water damage claims.

Water damage represents 53% of Washington condo claims, so this coverage deserves special attention. Ask each carrier about water backup coverage, which protects against sump pump failures and drain backups that standard policies exclude. Also request quotes for loss assessment coverage with limits between $5,000 and $10,000, depending on your building size and age.

Add Specialized Coverage for High-Value Items

Specialized coverage for high-value items like jewelry, art, and collectibles should use scheduled coverage rather than relying on your personal property limit, because standard policies typically cap jewelry at $1,500 total. Scheduled coverage lists specific items with agreed values, eliminating depreciation entirely after a loss. For earthquake endorsements, compare deductibles across carriers because they range from 5% to 20% of insured value, creating dramatically different out-of-pocket costs when the ground shifts.

Secure Flood Insurance and Bundling Discounts

Flood insurance through the National Flood Insurance Program carries a standard 30-day waiting period, so initiate that coverage immediately if your neighborhood sits near Puget Sound or any river corridor, rather than waiting until storm season approaches. Request quotes that show bundling discounts when you add condo coverage to auto or other policies, since bundling typically reduces total premiums by 10% to 15% across carriers in the Puget Sound region. H&K Insurance Agency represents multiple top carriers and can compare rates across policies to help you find the right protection at competitive prices.

Final Thoughts

Protecting your Seattle condo requires more than trusting your HOA’s master policy to handle everything. The gaps between what your association insures and what you actually own create real financial exposure that only a properly structured HO-6 policy closes. Your dwelling coverage must account for interior upgrades, personal property needs replacement cost protection rather than depreciation, and liability coverage shields you from guest injuries that the master policy explicitly excludes.

Condo insurance in Seattle WA demands local expertise because Puget Sound risks differ from other regions. Earthquake activity, flood zones near rivers and Puget Sound, and the specific master policy structure your HOA chose all influence which coverages matter most for your unit. A local agent understands these regional factors and matches your coverage to your building’s actual needs rather than selling generic policies that miss critical gaps.

Start by obtaining your HOA’s Certificate of Insurance and calculating your true replacement cost for interior upgrades. Request quotes from multiple carriers that specify exactly what dwelling coverage includes and how water damage is handled. Contact H&K Insurance Agency to compare options and verify your condo insurance aligns with your master policy structure.