Seattle Area Homeowners Coverage: Finding the Right Policy

Seattle’s weather and geography create unique insurance challenges that standard policies often miss. At H&K Insurance Agency, we help homeowners navigate these complexities to find coverage that actually protects their homes.

The right Seattle area homeowners coverage requires understanding local risks like flooding, earthquakes, and windstorms. This guide walks you through the coverage options, comparison strategies, and annual review steps that matter most for Pacific Northwest homes.

What Standard Washington Homeowners Policies Actually Cover

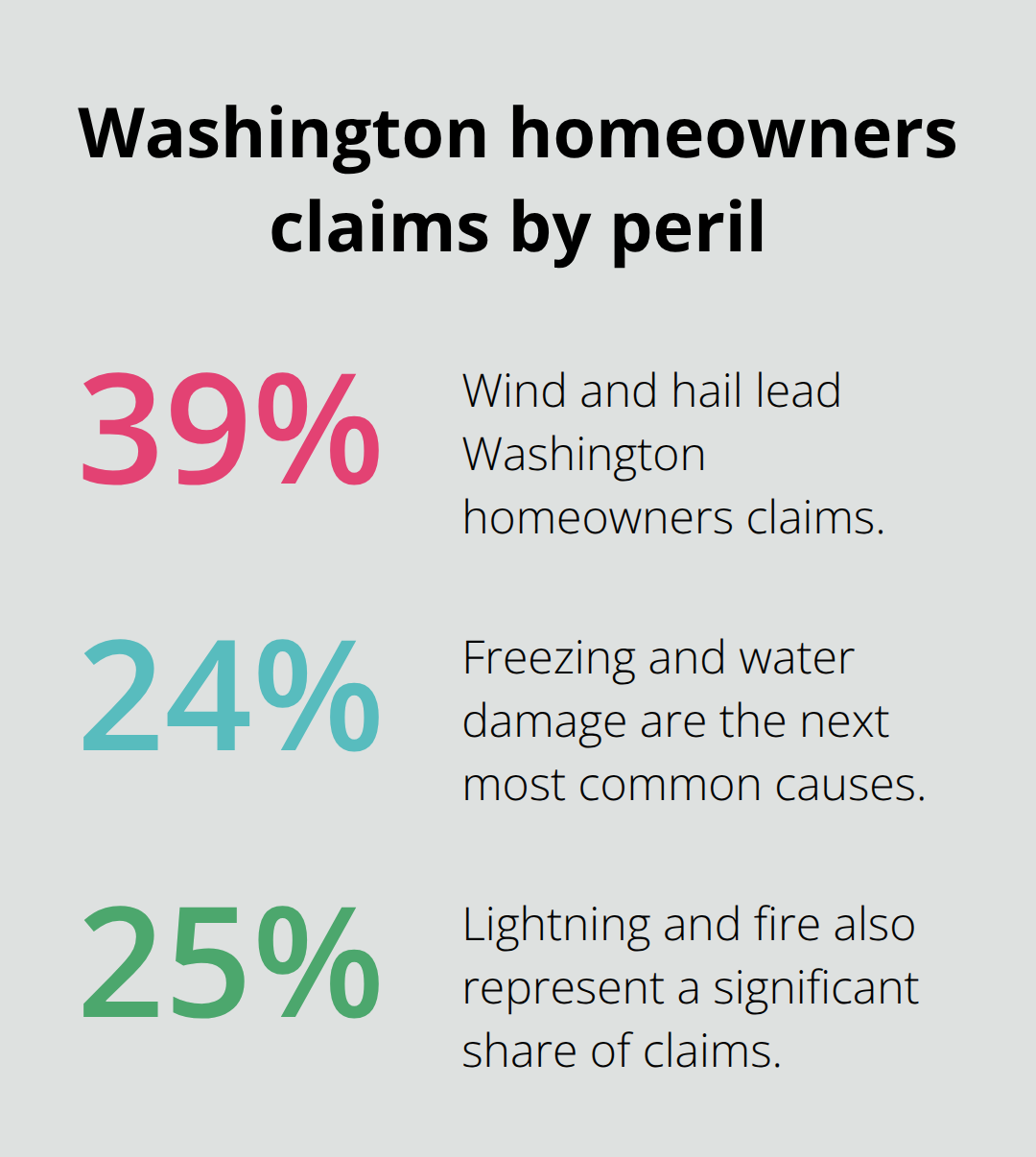

A standard HO-3 homeowners policy in Washington covers dwelling, personal property, liability, and additional living expenses-but the word “standard” masks critical gaps that hit Seattle homeowners hard. The Washington Department of Insurance reports that the average homeowners insurance cost in Washington is about $2,275 per year, though Seattle-area homeowners pay roughly $1,990 annually on average. That price reflects a baseline HO-3 policy with dwelling coverage around $500,000, $300,000 in liability protection, and a $1,000 deductible. However, this baseline excludes earthquakes and floods entirely, two hazards that pose real threats in the Puget Sound region. Wind and hail claims account for 39.4% of all Washington homeowners claims, freezing and water damage make up 23.5%, and lightning and fire comprise 24.8%, according to Insurance Information Institute data.

Your standard policy covers wind, hail, freezing pipes, and fire, but only if those losses result from covered perils-and maintenance issues often void claims. Water backup from storms, sewer damage, and mold remediation typically sit outside standard coverage, capped at around $5,000 to $10,000 if they’re included at all. Dwelling coverage should reflect replacement cost, not market value, and the median rebuilding cost for Washington homes is about $456,643 according to First Street, meaning many homeowners underestimate what they actually need.

The earthquake and flood exclusion gap

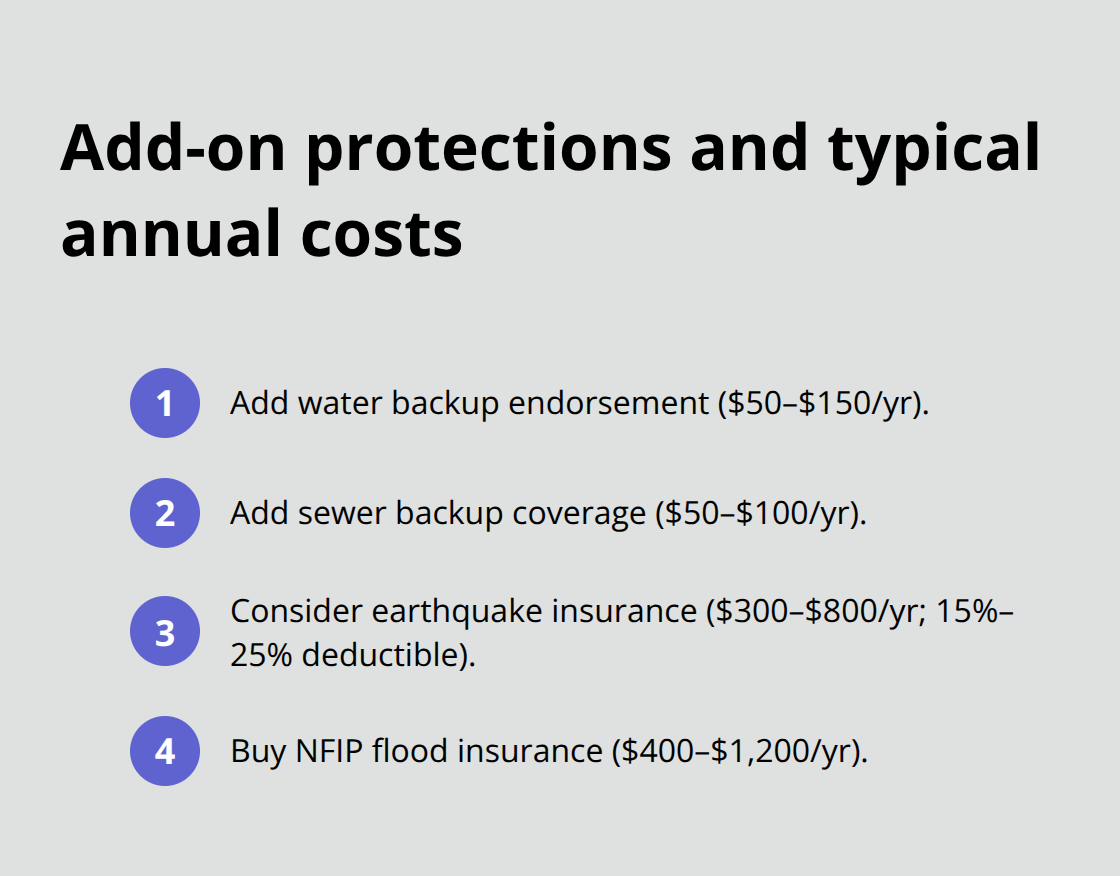

Earthquakes and floods are explicitly excluded from every standard HO-3 policy sold in Washington. The 2024 USGS Uniform California Earthquake Rupture Forecast updates underscore significant seismic risk in the Pacific Northwest, yet most homeowners skip earthquake coverage because they don’t understand the cost. Earthquake premiums run roughly $300 to $800 per year with deductibles between 15% and 25% of your building coverage-meaning a 20% deductible on $400,000 dwelling coverage requires an $80,000 out-of-pocket payment before coverage activates. Flood insurance comes through the National Flood Insurance Program under FEMA and costs typically $400 to $1,200 annually depending on your flood zone and home elevation. A Reddit post from a South Seattle homeowner showed that Country Financial quoted $1,600 per year for a 2,500-square-foot home built in 1955 with no flood or earthquake coverage included, highlighting how quickly costs climb when you add regional protections. Seattle faces substantial flood risk from atmospheric rivers and potential tsunamis, making separate flood insurance genuinely necessary for properties in high-risk zones rather than optional.

Personal property coverage gaps

Personal property coverage on a standard policy tops out at 50% to 70% of your dwelling limit and pays actual cash value unless you upgrade to replacement cost coverage. High-value items like jewelry, art, and collectibles require scheduled personal property riders to avoid massive underinsurance penalties. Most homeowners accept these default limits without questioning whether their belongings would actually be replaced at today’s prices if a loss occurred. Adding replacement cost coverage to personal property costs more upfront but protects you from depreciation penalties that can slash claim payments by 30% to 50%.

Liability limits that leave you exposed

Liability coverage starting at $100,000 is legally insufficient for most homeowners-liability claims regularly exceed six figures, and adding coverage from $100,000 to $300,000 costs almost nothing extra. An umbrella policy adding $1 million of liability protection costs roughly $150 to $300 per year and makes financial sense for anyone with meaningful assets. Additional living expenses coverage should align with your actual monthly costs if your home becomes uninhabitable after a covered loss, yet many homeowners accept default limits that won’t cover temporary housing in Seattle’s expensive rental market. When you compare quotes from multiple carriers, ask each one about their liability limits and what temporary housing coverage actually includes-the differences between carriers can be substantial.

What Seattle Homeowners Actually Need Beyond Standard Coverage

Flood and earthquake gaps that standard policies ignore

Flood and earthquake risks in the Puget Sound region demand coverage that your standard homeowners policy simply will not provide. Flood insurance through the National Flood Insurance Program costs between $400 and $1,200 annually depending on your flood zone and home elevation, but skipping it exposes you to catastrophic losses. Federal flood maps and tools like First Street’s climate hazard models let you check your address to see your actual flood risk rating before deciding whether coverage is necessary. Seattle faces serious flood threats from atmospheric rivers that overwhelm drainage systems and cause interior water damage that standard policies explicitly exclude.

If you live within a FEMA high-risk flood zone, your mortgage lender will require flood insurance anyway, so the choice is whether you control that coverage or let your lender force a more expensive policy on you. Earthquake coverage costs roughly $300 to $800 per year with deductibles typically between 15% and 25% of your building coverage amount. A homeowner with $400,000 in dwelling coverage and a 20% deductible would need to pay $80,000 out of pocket before earthquake insurance activates, making the deductible more important than the premium when evaluating policies. The 2024 USGS Uniform California Earthquake Rupture Forecast updates confirm significant seismic risk across the Pacific Northwest, yet most Seattle homeowners skip this coverage because they underestimate the probability or don’t understand what it actually costs.

Wind, storm, and water damage protection

Wind and storm damage protection is already included in your standard HO-3 policy, but this creates a false sense of security that leads to claim denials. Wind and hail claims account for 39.4% of all Washington homeowners claims according to the Insurance Information Institute, yet many carriers impose strict maintenance requirements that void coverage if your roof or gutters show neglect. Freezing and water damage from burst pipes comprise 23.5% of Washington claims, and these losses happen fast during winter cold snaps when pipes in unheated spaces or poorly insulated walls freeze and rupture. Your policy covers the burst pipe itself, but water backup from overwhelmed storm drains or sump pump failure requires a separate water backup endorsement costing $50 to $150 annually.

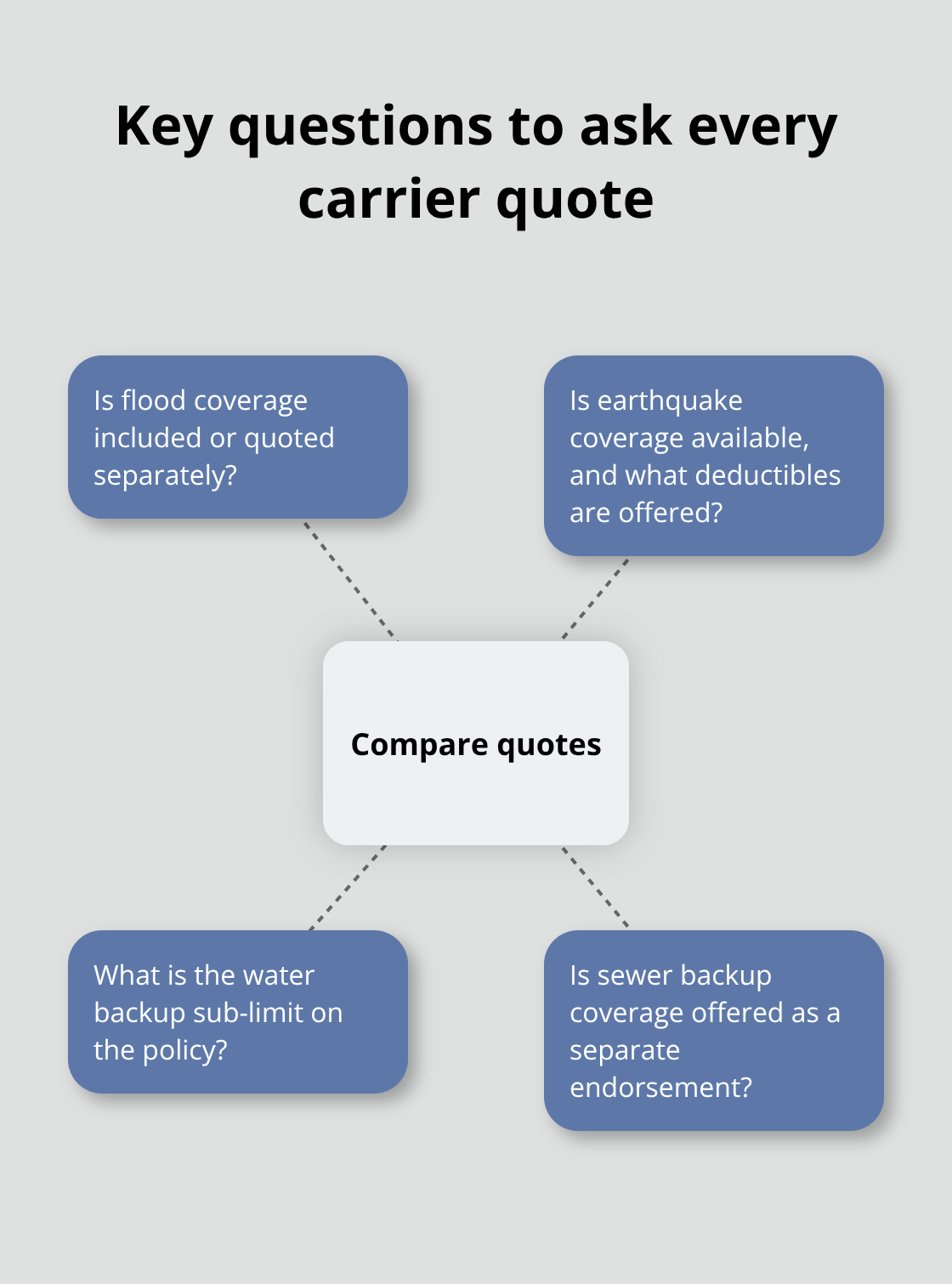

When you request quotes from multiple carriers, ask specifically whether water backup coverage is included and what the sub-limit is, because some insurers cap this coverage at just $5,000 while others offer $25,000 or more. Sewer backup coverage operates separately and costs another $50 to $100 per year, protecting you from the expensive scenario where your sewer line backs up into your home during heavy rain. Seattle’s older neighborhoods often have aging sewer infrastructure that backs up regularly, making this endorsement genuinely necessary rather than optional.

Comparing total protection costs

Request quotes that bundle earthquake and flood insurance with your homeowners policy to see how total costs stack up, since some carriers offer modest discounts when you purchase multiple policies together. As an independent agency serving the Puget Sound region, H&K Insurance Agency represents multiple top local and national carriers, which means you can compare rates and customize packages that include flood, earthquake, and other regional protections without shopping around to different agencies. The real question isn’t whether you can afford these endorsements-it’s whether you can afford not to have them when a loss occurs.

Finding the Right Carrier and Coverage Combination

Compare quotes from multiple carriers at once

Requesting quotes from three to five carriers simultaneously reveals what Seattle area coverage actually costs, since rates vary dramatically based on how each insurer prices flood risk, earthquake exposure, and water damage endorsements. When you call or visit websites, most carriers ask the same questions about your home’s age, square footage, construction type, and prior claims history, so you can complete multiple applications in under an hour and compare apples-to-apples pricing. The critical step most homeowners skip involves asking each carrier the same follow-up questions about what their baseline quote includes and what costs extra. Specifically, ask whether flood coverage is included in the quote, whether earthquake is available, what the water backup sub-limit is, and whether sewer backup coverage is offered separately.

A homeowner in South Seattle received a quote of $1,600 annually from Country Financial for a 2,500-square-foot home built in 1955 with no flood or earthquake coverage included, which illustrates how dramatically prices shift once you add regional protections that actually matter in the Puget Sound area. Once you have three quotes, calculate the total annual cost of homeowners insurance plus earthquake plus flood to see the real price difference between carriers, since some insurers bundle these coverages more competitively than others.

Evaluate carrier strength and complaint history

NerdWallet’s home insurance ratings weigh consumer experience at 40 percent, financial strength at 30 percent, coverage options at 25 percent, and available discounts at just 5 percent, which means you should prioritize carriers with strong complaint histories and financial stability over those offering the lowest premium alone. The Washington Department of Insurance maintains complaint data and financial strength ratings for every licensed insurer, so you can verify that a carrier with rock-bottom pricing hasn’t accumulated excessive complaints or faced regulatory action.

Maximize bundling discounts across your policies

Bundling your homeowners policy with auto insurance, RV coverage, or boat insurance typically yields discounts, making it worth shopping your entire insurance portfolio at once rather than treating home coverage in isolation. When you request quotes, tell each carrier about your other policies so they can apply bundling discounts before you compare final prices, since some carriers offer substantially larger discounts than others for multiple policies.

Work with an independent agent who understands regional risks

An independent agent who represents multiple carriers eliminates the need to contact each insurer separately and ensures that someone who understands Pacific Northwest risks helps you evaluate options. An experienced local agent asks questions most homeowners never consider, such as whether your home sits in a flood zone that requires lender-mandated coverage, whether your roof age affects available discounts or coverage, and whether your dwelling coverage limit aligns with regional rebuilding costs. A qualified insurance agent who specializes in regional coverage represents multiple top local and national carriers, which means you can compare earthquake deductibles, flood coverage limits, and bundling discounts without contacting different agencies.

Final Thoughts

Seattle area homeowners coverage succeeds when you match your policy to actual regional risks rather than accepting default limits that leave gaps. Dwelling coverage set to replacement cost based on your home’s rebuilding expenses, earthquake and flood protection tailored to your specific location, and liability limits high enough to protect your assets form the foundation of adequate protection. Most homeowners underestimate rebuilding costs, skip earthquake coverage because they don’t understand the premium structure, or accept $100,000 liability limits that won’t cover a serious claim.

Review your policy annually after any home improvements, since renovations increase your dwelling coverage needs and may qualify you for discounts on safety upgrades. Check whether your personal property coverage still reflects what you actually own, especially high-value items that require scheduled riders. Update your additional living expenses limit if Seattle’s rental market has shifted, since temporary housing costs climb faster than most homeowners expect.

We at H&K Insurance Agency represent multiple top local and national carriers serving the Puget Sound region, which means we compare rates and customize packages that include flood, earthquake, and other protections without you contacting different agencies. Request quotes that bundle your homeowners policy with auto, boat, or RV coverage to maximize discounts while ensuring your Seattle area homeowners coverage actually protects what matters most.